How’s your business doing? A commonplace question, perhaps, but customers, suppliers, creditors, investors and management all have a vested interest in the answer. Even so, it’s not easy to capture a company’s precise state of current financial health, much less understand how to improve it. Part of this is because financial performance is largely subjective. Although financial reports and key performance indicators (KPIs) are themselves objective measurements, there’s no single report or metric that sums up a company’s financial strength at any given moment. Moreover, there are countless different levers a business can push to boost the status of its financial performance.

How to Improve Financial Performance of a Company

A common mantra when considering how to improve business financial performance is: “You can’t manage what you don’t measure.” Yet no single ratio or metric is adequate for measuring financial performance on its own. Common indicators used to assess financial health include the business’s profitability, liquidity, cash flow, debt-to-equity ratio and return on assets — not to mention the data provided by financial statements, balance sheets and various KPIs.

But none of these indicators should be viewed in isolation. Only when used in aggregate — and compared with both historical data and industry benchmarks — can a business start to reach a comprehensive understanding of its financial performance.

And just as there are many ways to track financial performance, there are many ways to improve it. The first step is to identify points of friction: Is the company bleeding cash? Have you taken on too much debt? Are customers dwindling? Do financial management strategies need maintenance? Recognizing problems will reveal the next step, whether it’s cutting supply costs, improving accounts receivable collections, boosting revenue with a new marketing campaign or even working with a financial professional.

Before taking any action, get a measurement of current financial performance. This baseline is key to assessing whether future efforts to improve financial performance are paying off. Then, collect data during and after any actions are taken. Generally, the goal is to make at least one ratio, financial statement or KPI show positive movement over time — more revenue, a greater profit margin or a lower debt-to-cash ratio, for instance. But remember that financial performance can’t be assessed in a vacuum, and some metrics can decline even as others improve. For example, revenue can increase even as cash reserves decline, perhaps because expenses are increasing with growth. That’s why financial performance indicators must be assessed in aggregate.

Key Takeaways

- There are numerous ways a company can improve its financial performance.

- Cutting costs, managing debt, boosting revenue, obtaining external funding or consulting with financial professionals are all actions that can benefit financial health.

- Measure financial performance before taking action to improve. Continue to track financial ratios, metrics and KPIs to ensure that your efforts are paying off.

- The right accounting software can minimize time spent running manual calculations by automatically tracking KPIs and other key financial metrics.

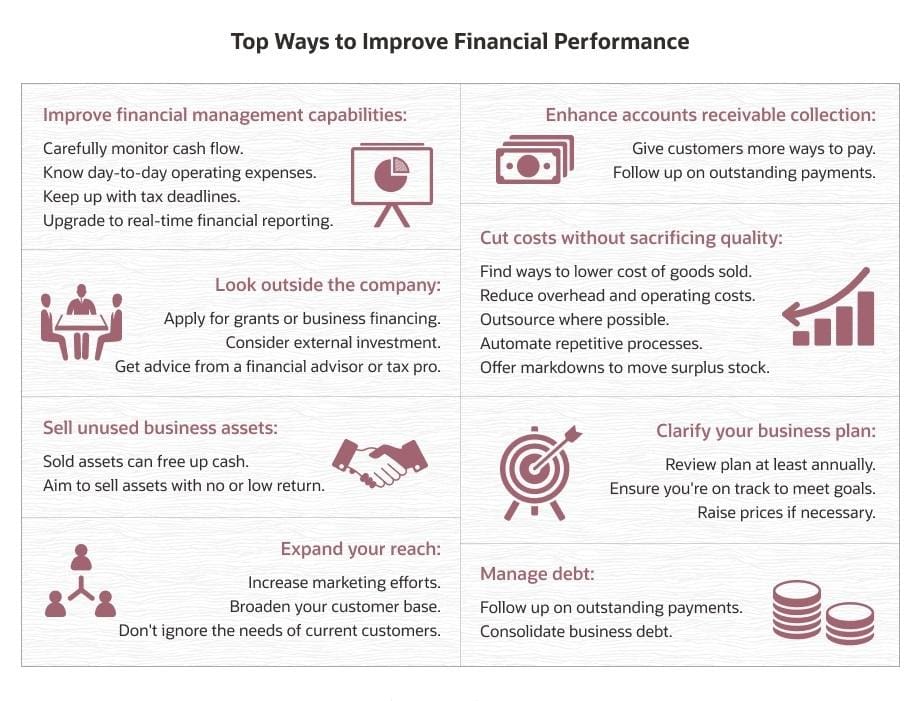

20 Ways to Improve a Company’s Financial Performance

Here are 20 possible ways to improve your business’s financial strength and stability — plus trackable metrics, where relevant. Remember: KPIs and other metrics should be considered alongside financial reports and statements to get the most comprehensive understanding of the business’s financial health. Be sure to take before and after snapshots of relevant metrics to gauge success.

1. Clarify your business plan.

A business plan forms the basis of any company. It describes the company, establishes its goals and lays out the intended means for reaching those goals. A strong business plan can guide a company toward success, help it secure funding and even attract employees — particularly, management or executive staff. Though writing a business plan is generally one of the first steps to starting a company, it’s not a document you can set and forget. Instead, aim to review the business plan at least yearly. Clarify overall business goals, what big-picture success looks like (using quantitative measures whenever possible), how each functional team will contribute to those goals and what metrics will be used to hold each team accountable.

For example, if competitors have begun to reduce prices to get more business, it might be time to revise your business plan’s marketing strategies in order to mitigate revenue loss. Marketing teams could then be responsible for boosting efforts to attract customers. But for those efforts to be successful, they’ll also need to make sure the project’s ROI doesn’t cut away at profits, even if it increases revenue; meanwhile, it doesn’t hurt to have the sales team track customer retention to make sure brand loyalty isn’t fading.

Integrated business planning, or IBP, can be a useful way to adopt this type of detailed and unified approach to improving financial performance. It’s a way to clarify your business plan and align goals with the company’s finance, product development, marketing, supply chain and other key operational teams. Successfully adopting IBP requires substantial cultural change, in that the organization must shift toward tight collaboration and trust among traditionally siloed teams. But if implemented correctly, benefits are vast: Close collaboration leads to improved decision-making, improved responsiveness, greater forecasting accuracy and, above all, increased revenue.

2. Know your day-to-day costs.

When it comes to running a business, it’s key to know how much money is spent on day-to-day operations, aka operating expenses. Also referred to as OPEX, operating expenses include fixed costs, such as rent, staff salaries and property taxes, and variable costs, such as utilities and sales commissions. OPEX excludes the direct costs attributed to processes involved in manufacturing a product or delivering services, known as cost of goods sold (COGS). COGS encompasses the cost of purchasing raw materials, as well as manufacturing activities, including labor.

OPEX typically makes up most of a business’s overall expenses, but it’s important to keep it as low as possible without negatively impacting either the quality of goods or services or customer or employee experiences. That’s because if operating expenditures increase without a corresponding increase in revenue, profitability decreases.

Knowing exactly where money is going will help reveal places to cut costs or prioritize spending. For example, knowing that a large proportion of daily operating expenses goes to energy bills reveals an opportunity to maximize energy efficiency.

Although daily OPEX can be tracked and calculated manually or through spreadsheets, accounting software makes it much easier to capture operating expenses and track related metrics, such as gross burn rate and average daily expenditures.

Gross burn rate measures how quickly available cash is spent on operating expenses. The higher the burn rate, the faster the company will run out of cash — unless it boosts revenue or receives additional financing or funding.

Gross burn rate = Company cash / Monthly operating expenses

Average daily expenditures measures the average amount of money spent on a daily basis. Here’s one way to calculate daily costs:

Average daily expenditures = (Annual COGS + Annual operating expenses) / 365 days

3. Improve accounts receivable collection.

It’s one thing to have great sales on paper. It’s another to actually have cash in hand. Even if payment instructions are crystal clear, it’s almost inevitable that some customers will not comply. Missed or late payments can take a toll, gumming up cash flow and ultimately making it harder to secure financing. Two KPIs that can help a company track its accounts receivable processes are days sales outstanding (DSO) and accounts receivable turnover. Both are good benchmarks to track for any company looking to improve financial performance.

DSO tracks the average number of days it takes to receive payment for sales purchased on credit. High or rising DSO signals a need to check in with customers or improve accounts receivable collections.

DSO = (Average accounts receivable for a period / Credit sales made for period) x number of days in period

Accounts receivable turnover is a ratio that reveals how efficiently your company collects debts. The lower the ratio, the longer it takes customers to pay. This could mean payment terms are too flexible.

Accounts receivable turnover = Net credit sales / Average accounts receivable

If KPIs, like DSO and accounts receivable turnover, aren’t ideal, the following tips could help your business recover outstanding debt — and simultaneously prevent future shortfalls:

- Make it easier to pay. The more ways a customer can pay, the more likely they are to pay sooner. Offer multiple payment options, such as check, e-check, credit card and debit card.

- Clearly communicate payment terms. Give customers terms and conditions up front, including how much time they have to pay (net 30 or net 45, for example). Be clear about penalties or fees that will be applied to late payments.

- Invoice quickly and accurately. Invoice immediately after a sale, state terms clearly on invoices and follow up if they’re not paid on time. Send repeat messages at strategic intervals that politely remind customers that their payment is past due. Make sure invoices don’t contain errors that could delay payment, such as incorrect amounts or missing purchase order information.

- Offer early-pay discounts. Early-pay discounts can be a win-win for companies and their customers. The company gets paid sooner, which boosts cash flow, and the customer gets a discount. Plus, any dollar amount given up in discounts will generally be smaller than the costs of uncollected invoices.

- Use automation. Accounts receivable software can automate manual processes, making it easier to send accurate invoices faster. Payment reminders can also be sent automatically.

4. Seek professional advice (financial adviser).

Business owners tend to wear many hats. They often must make personnel decisions, decide upon capital allocations, strategize how to grow sales, identify where to cut costs and constantly respond to emergencies. For this reason, it can be especially beneficial to consult a financial adviser when trying to improve financial performance. These professionals have the tools, resources and knowledge to help companies budget, manage investments, create long-term financial goals and even manage taxes.

A great way to find a financial adviser is through personal referrals. Ask other business owners whom they use and whether they are satisfied with the results. Another option is to approach the local chamber of commerce or one of following organizations — some of which will provide peer assistance pro bono:

- Service Corps of Retired Executives (SCORE)

- Financial Planning Association (FPA)

- Foundation for Financial Planning (FFP)

- The National Association of Personal Financial Advisers (NAPFA)

- The Association for Financial Counseling & Planning Education (AFCPE)

When searching for an adviser, note that they should be:

- A fiduciary who is required by law to always put their clients’ best interests before their own.

- Compensated with fees, not commissions.

- Prepared to tell you how much time, as well as money, they can save or help generate.

- Adept at adopting advancing technology as it becomes available.

- An expert in the specific area of finance your business needs help with.

- Able to provide references from other clients.

5. Reduce expenses.

One straightforward way to improve financial performance is to cut costs. If costs decline while incoming revenue remains the same, profitability increases.

First, identify potential places of waste or inefficiency. Four main areas to look at include people, energy, transportation and travel. But it’s worth scouring every part of the business. Scrutinize the costs of office supplies, advertising, rent, utilities, insurance, loan terms and credit card fees. Don’t forget to look at business processes, too: If your staff spends more time troubleshooting faulty equipment than producing products, for example, valuable time is being wasted.

Next, begin cutting costs where possible, in controlled environments. There may be several areas worth addressing, but try not to target everything at once. Businesses, in many ways, are delicate machines. If you tinker with one area — say, by cutting advertising costs — be sure to keep an eye on other areas, like new customer acquisitions. Additionally, don’t overlook automation technology’s ability to help boost financial performance. Especially in the cloud era, businesses can get up and running with apps that cause worker productivity to soar by eliminating repetitive, manual tasks and consolidating currently disparate systems to avoid the time — and mistakes — often generated by manual data entry and analysis.

Be sure to track metrics before and after taking any action. Profitability ratios, such as net profit margin, can clue you into how expenses are affecting the financial health of the company. If net profit margin starts falling, it might be a sign to try to reduce COGS, for example — maybe by finding a more affordable supplier, buying in bulk or even automating parts of the job. As always, net profit margin shouldn’t be assessed in isolation. Instead, look at it alongside other relevant metrics, such as return on investment or cash flow.

6. Sell business assets.

Assets are resources a business owns or leases that can be used to create value in the future. For example, if mobile apps are a business’s primary source of revenue, the phones, laptops, tablets or other types of computers used for programming would be key business assets. Tangible assets, such as inventory and machinery, have a physical presence — their value is easily measurable. Intangible assets, such as patents, trademarks and copyrights, lack a physical component and can be harder to measure.

Many businesses possess tangible assets that they aren’t using or aren’t using to the fullest extent. Selling these assets can be a good way to generate cash and free up funds for tactical or strategic investments that will help the core business.

Assets are recorded on the company balance sheet. Clear and accurate records of assets across their entire life cycles can make it easier to know at a glance the financial position and net worth of each asset and to analyze which assets are performing and which are generating less value. Once that data is provided by the balance sheet, several KPIs can be used to determine how well assets are performing. Here are a few:

Working capital measures whether a business has sufficient current assets to meet short-term financial obligations. Though a higher number is generally better, working capital that’s too high may indicate that assets aren’t being leveraged as well as they could be or that surplus cash isn’t being invested wisely.

Working capital = Current assets – Current liabilities

Fixed assets turnover measures efficiency, or how well assets are used to generate sales. A higher ratio is good and indicates effective utilization of fixed assets. A lower ratio says the reverse.

Fixed assets turnover = Net sales / Average fixed assets

Return on assets measures the efficacy of a company’s management to generate profits from its assets. The higher the return, the better.

Return on assets = Net income / Total assets for period

If the business has assets that aren’t generating sufficient value — maybe the production facility is storing unused equipment — it might be time to research the value of the assets in question to see if they’re worth selling: What is the current market value of the asset? How much would it realistically bring in if sold today? An asset’s value can fluctuate significantly over time, so make sure the analysis considers current demand, prices and any upcoming trends that could affect its value. Consider the costs of selling, such as tax implications and advertising expenses, as these will chip into the return.

Once assets are sold, compare KPIs from before the sale and after the sale to see how much selling those assets improved financial performance.

7. Increase prices.

Any company that’s in business for any length of time will eventually need to raise prices — whether due to rising costs, inflation, a brand overhaul or value added to goods or services. Whatever the catalyst, raising prices is a delicate matter with long-term implications. A business needs to purposefully decide whether to raise prices, how to do it, how much more to charge and how to communicate that increase to customers without alienating them.

One way to get a sense of whether prices should increase is by tracking gross margin, or the percentage of revenue a business keeps after deducting the cost of goods sold. The higher the percentage, the more profitable each sale. If the company’s gross margin is lower than desired, and cost of goods sold is already as low as possible, it might be time to raise prices.

Gross margin = [(Total revenue – COGS) / Total revenue] / 100

Customer acquisition cost (CAC) is another KPI that can influence a company’s pricing strategy. If the cost of acquiring new customers is higher than desired, the business might need to either find ways to lower CAC or set a higher price point to cover the cost of that acquisition. Doing so can help ensure that the business remains profitable in the long term.

Customer acquisition cost = Total sales and marketing cost / Number of new customers

If it’s time to raise prices, it’s a good idea to first check out what competitors are charging. Analyze the value being provided from the low end to the high end of the spectrum of the offerings in the market. Decide where your brand best fits in and how it stands out against competitors. How can you capitalize on that differentiation as a reason to raise prices?

Avoid raising prices until after the change has been announced and justified. No customer welcomes sticker shock; it’s generally better to communicate with utter transparency. Perhaps view this as an opportunity to emotionally reconnect with customers. After all, emotion drives purchase behavior even more than price, research shows. Not sure how to announce your price increase? Give it prominent placement on your website, post it on social media or consider sending a personalized email.

8. Offer markdowns to move surplus stock.

Even if you track all the right KPIs, demand planning can be as much art as it is science. Unforeseen events could shift the market or economy, leading to overstock at the end of a selling season. Don’t consider this a failure. Most retailers and manufacturers would rather have a small inventory left over than run short, as the latter would potentially mean lost sales. To effectively manage surplus stock, consider implementing strategies such as determining appropriate discount levels and leveraging various sales channels. Additionally, timing plays a crucial role in offering markdowns, and market research, customer behavior analysis, and market trend monitoring can help identify the optimal time to maximize demand

That’s why markdowns are inevitable. A markdown is a permanent price decrease for a product at the end of its life cycle. It’s used to boost demand and ideally sell off all remaining stock. Markdowns can occur at any stage of the manufacturing process, from raw materials to finished goods. In many cases, you won’t be able to recover all your costs. But at least you can limit carrying costs and stop the inevitable decline in value of aging inventory — all of which can negatively affect a business’s financial performance. Here’s a simple way to calculate inventory carrying costs:

Inventory carrying costs = (Cost of storage / Total annual inventory value) x 100

ABC inventory analysis can also be a useful way to determine which products will benefit most from markdowns. It helps determine the value of inventory items, based on their importance to the business. ABC groups items according to demand, cost and risk data. This helps business leaders understand which products or services are most critical to the financial success of their organization. The most important stock keeping units (SKUs), based on either sales volume or profitability, are “Class A” items. Class A items are typically the 20% of goods that deliver 80% of the value. The next most important goods are “Class B,” which are less valuable. The least important are “Class C,” which make up the greatest percentage of inventory and deliver the least value.

Conduct ABC inventory analysis by finding the annual usage value per product. To do so, multiply the annual sales of a certain item by its cost. The results reveal which goods are most valuable and which yield the lowest profit, so you know where to focus human and capital resources — and where to offer markdowns.

Annual usage value per product = (Annual number of items sold) x (Cost per item)

When you have an idea of what products to markdown, make sure any resulting price drops:

- Are part of a holistic pricing strategy for each product across its entire life cycle.

- Will help clear out end-of-life inventory while maximizing gross margin.

- Take into account nuanced factors that can affect product demand, such as seasonal trends, economic traditions, sociocultural trends and competition.

It may also help to start with a small markdown and gradually increase the discount if the product still doesn’t sell.

9. Offer multiple payment options.

Cash might be king, but many consumers and businesses prefer card payments or direct deposits. Ultimately, the types of payment you accept may depend on your specific customer base and your business requirements. A smaller local business may be able to get away with accepting only cash or check, whereas a major ecommerce retailer will likely need to accept credit cards, debit cards and maybe even a partnership with a buy now, pay later provider. In any case, it’s important to ensure an easy, seamless checkout or invoicing experience for customers.

B2B companies might want to track a KPI, like day sales outstanding, to get a sense of whether customers could be paying sooner (see “3. Improve accounts receivable collection,” above). For B2C companies, tracking the cart abandonment rate might reveal that customers are failing to complete a purchase when it’s time to enter payment information, signaling a need for more payment options. Remember: Carts can also be abandoned for different reasons, such as high taxes or fees or slow shipping times, so it’s important to track exactly when shoppers are clicking away.

Cart abandonment rate = 1 – (Completed purchases / Number of carts abandoned before checkout) x 100

In general, the more flexible a business can be about accepting different kinds of payments, the more likely a B2B customer will be able to make on-time payments and the less likely a B2C customer will be to abandon their cart. The faster more sales can be made, the greater the cash flow benefits — and the greater the chances of improving financial performance.

Many technology platforms help businesses accept a variety of payment methods, from e-checks to credit cards. In addition to considering what’s practical for your business, keep the following in mind when deciding which payment options to offer:

- Price: What is the pricing structure, especially the per-transaction fee? This is a key consideration since fees can erode profit margins, but not accepting credit cards can dramatically limit clientele.

- Features: What other capabilities does the vendor offer, other than facilitating payments? Do they offer chargeback protection or analytics services, for instance?

- Flexibility: Can customers choose how to pay? Are credit cards, debit cards, digital wallets and bank transfers all accepted?

- Connectivity: Does the solution integrate with your other financial management software?

- Security: What kind of security does the platform have? Is there any fraud protection?

10. Consolidate your business debt.

Debt consolidation rolls up outstanding loans, credit card balances and other debts into a single loan with a single monthly payment. In addition to simplifying monthly payments, debt consolidation could also provide lower interest rates, reduced payments, shorter repayment periods or all three. Any of these benefits could help a company manage its finances — especially if the company’s cash flow-to-debt ratio is low.

Cash flow-to-debt ratio measures how much debt a company could repay with its operating cash flow, or total revenue minus operating expenses.

Cash flow-to-debt ratio = Operating cash flow / Debt

If a company’s cash flow-to-debt ratio is 0.5, for example, this means the company is earning $0.50 for every dollar of debt it can repay. In other words, the company owes more in debt than it’s taking in. Though factors like revenue and operating expenses also influence cash flow-to-debt ratio, if a business can lower monthly debt payments or interest rates through consolidation, it may improve its ratio — benefiting financial performance. Other financial KPIs, such as current ratio, working capital and the quick ratio, can also help a company gain an understanding of its ability to cover debt.

Debt consolidation loans are available from several different sources, including banks, credit unions, the Small Business Administration (SBA) and alternative peer-to-peer lending companies.

11. Increase marketing efforts.

Marketing helps increase brand awareness, which, in turn, attracts customers and drives sales. Without effective marketing, businesses would struggle to compete. Businesses looking to improve financial performance might consider boosting or rethinking their marketing efforts — particularly if site traffic seems to be waning or if KPIs like return on marketing investment (ROMI) are lower than desired.

Site traffic measures how many visitors your website gets over a period of time. More visits usually lead to more sales. Companies can get fairly granular in how they measure site traffic. For example, tracking traffic by source (how visitors found your website) can help ensure that you’re making the right marketing investments. Say a business is failing to get organic clicks months after starting a new search engine optimization (SEO) marketing strategy. Something probably needs to change. Maybe the site is optimized for desktop, but their target audience primarily searches on mobile. Transitioning to a mobile-friendly layout is key, as Google primarily uses the mobile version of a site when indexing and ranking. That simple change could be enough to boost marketing performance, get more clicks, more sales and, ultimately, more revenue.

ROMI compares the cost of marketing to how much revenue and profit it generates. Since it can take weeks or months to convert a lead into a customer — especially in the B2B space — it’s best to track ROMI over time. Tracking this KPI can help demonstrate marketing’s contribution to the bottom line, justify marketing spend and determine how future budgets should be allocated.

Return on marketing investment = (Net return on marketing investment / Cost) x 100

If ROMI is low, make sure you clarify your target audience: What are their needs? Do you understand their demographics — location, age, gender and interests? The more you know, the easier it will be to create marketing messages that resonate. It can help to conduct market research, with surveys or focus groups, or by analyzing the competitive landscape of your particular market. Then, identify the features and benefits unique to your company. This is your value proposition. Find creative ways to accentuate those differences and initiate contact with customers via email, webinars, podcasts, social media content or even television, radio and digital advertising.

Whatever route the business goes, track related marketing KPIs. For example, marketing qualified leads (MQLs) can be used to assess how many leads are coming in from a new marketing effort, be it an email, social media or SEO campaign. Coupled with conversion rate — or how many of those visits lead to sales — a business can get a pretty good sense of how increased marketing efforts are affecting overall financial performance.

12. Apply for grants.

In business, a grant refers to a sum of money that is given by a government agency, nonprofit organization or even a commercial entity to a business or individual, usually for a specific purpose. Grants are often used to support research and development, to start up new businesses or for specific initiatives, such as those related to sustainability, population equality and community development.

The cash infusion grants provide can be just what a business needs to help boost financial performance, whether by improving cash flow or making it more affordable to invest in the equipment — or people — necessary to build the business. And, unlike loans, grant money does not have to be repaid.

But the grant scene is competitive and to successfully get awarded one takes attention and time. Businesses typically won’t qualify for most of the grants they apply for, but understanding how specific grant-issuing organizations evaluate applicants can help increase the chances of success. In addition:

- Look for grants within your industry.

- Read the eligibility requirements carefully.

- Make sure your business aligns with the grant organization’s mission.

- Know what you’ll be spending the grant money on.

- Focus your pitch accordingly.

Though grants are essentially “free money,” the recipient may be required to meet certain conditions or report on the use of the funds; grant issuers usually have a mission and like to know their money is being put to good use. If you are approved for a grant, keep good records and make sure funds are being used effectively. And though it might be tempting to spend grant money freely, it does help to track the return on any investments funded by grants — as well as the cost effectiveness of any grant-funded projects — to ensure that financial performance is truly improving.

13. Meet tax deadlines.

Businesses, like individuals, must file a tax return. Business structure, location and net income, among other factors, determine which forms need to be filed, which taxes must be paid and how much.

Failing to pay taxes on time can incur steep costs and inhibit financial performance. For instance, if a business doesn’t file on time, it may have to pay up to 5% of the unpaid taxes for each month or part of a month that the return is late (but the penalty won’t exceed 25% of the business’s unpaid taxes). The IRS will also charge interest on underpaid taxes and penalties. Meeting tax filing and payment deadlines can, therefore, prevent unnecessary charges.

Additionally, meeting tax deadlines demonstrates compliance with laws and regulations, which can help a business maintain a good reputation and build trust with customers and partners.

Here’s a list of common business taxes to be aware of:

- Income tax: Except for partnerships, all businesses need to file an annual federal income tax return. (Partnerships file an information return and each partner reports taxes on their individual return.) The federal income tax is a pay-as-you-go tax, meaning taxes must be paid as income is earned during the year. Employees usually have income tax withheld from paychecks; if not, it’s likely estimated tax payments must be made. Most states also impose a business income tax.

- Estimated tax: Businesses generally must pay taxes on income by regularly making estimated tax payments throughout the year, usually quarterly. Any income that is not subject to withholding, such as income from self-employment, interest and dividends, must be paid this way.

- Self-employment tax: Self-employed business owners must pay self-employment taxes to cover Social Security and Medicare taxes. These taxes must be paid in addition to income taxes and are paid quarterly, as estimated taxes.

- Employment taxes: Businesses that have employees must withhold and deposit federal and state income taxes from employee wages. Employment taxes include Social Security and Medicare taxes, federal income withholding taxes and the federal unemployment tax (FUTA). Due dates can differ; check with the IRS or a tax professional.

- Excise tax: These taxes must be paid if the business manufactures or sells certain products, is paid for certain services or uses certain types of equipment, facilities or other products. Excise taxes are typically imposed on the sale of things considered to be nonessential or harmful, such as fuel, tobacco, firearms and airline tickets. Excise taxes are paid quarterly.

The IRS provides an online Tax Calendar to identify important tax deadlines and remind businesses when to pay. It can be customized to match your business structure, fiscal year and other parameters. Note that tax deadlines may change if a business files tax returns for a fiscal year, instead of a calendar year.

14. Control overhead costs.

Every business has overhead costs. Overhead costs are not directly tied to the production or sale of a specific product or service but are necessary to keep the doors open and lights on. Carefully controlling overhead is one way to improve financial performance; assuming all else is equal, the higher a company’s overhead, the lower its net profit margin.

Fixed costs are the same for every monthly, quarterly or annual payment. They include rent or mortgage payments, insurance, property taxes and administrative salaries. Variable overhead costs, like utility bills, office supplies and equipment, change from payment to payment, and may not be paid on a fixed schedule. There are many ways to cut back on both fixed and variable overhead costs. But first, it’s a good idea to calculate the business’s overhead rate. Here’s a simple formula:

Overhead rate = Overhead costs / Sales

If a company has $50,000 in sales for June and overhead costs of $8,000, the overhead rate is 16%. For every dollar brought in, the company spends $0.16 in overhead. A good overhead rate depends on the business and industry, but it’s generally a good idea to keep overhead as low as possible. Too high a rate indicates the business is likely spending too much on operations, which can limit the bottom line and eventually make it hard to stay solvent.

Common ways to control overhead include:

- Cutting utility costs by reducing energy consumption, such as by improving insulation or using energy-efficient lighting.

- Outsourcing administrative or specialized tasks, such as payroll.

- Negotiating better payment terms or deals with suppliers.

- Lowering rent and payments by cutting back on office space, warehouse space, retail space. This can also shave utility costs.

- Reducing labor costs by automating manual processes.

15. Monitor cash flow.

Cash flow refers to the volume of cash that is coming into and going out of a company. It’s a measure of a company’s liquidity and its ability to meet its financial obligations. Positive cash flow means that a company has more cash incoming than outgoing, while negative cash flow means the opposite. Businesses need to maintain positive cash flow to cover operating costs — raw materials, equipment, rent, payroll, supplies — and invest in future growth.

Monitoring cash flow is an essential aspect of improving business performance. Unfortunately, it’s possible to be profitable on paper and have negative cash flow, if you have a large volume of accounts receivable or unpaid invoices for products sold or services performed. If that happens, the business may struggle to pay its workers or cover operational expenses — and have nothing left to invest in any growth opportunities that arise.

The best way to monitor cash flow is to perform a cash flow analysis, ideally every month. There are three types of cash flow that should be analyzed, and each appears on a cash flow statement:

- Cash flow from operating activities. This is cash from customers after subtracting operating expenses.

- Cash flow from investing activities. This is cash garnered or spent from the purchase and sale of investments and property, plant and equipment (PP&E) assets.

- Cash flow from financing activities. This is cash inflows from friends, family, investors or institutions, such as banks or credit unions.

By tracking the cash coming in through these categories — as well as cash flow metrics and KPIs, like working capital and accounts receivable turnover — a business can see what money is coming in and where it’s going out. This info provides insight into the financial performance of the company and can help inform decisions about pursuing new marketing strategies and product lines, streamlining internal processes or finding ways to cut costs.

If cash flow is decreasing, take heed: Long-term negative cash flow can have serious consequences for a business’s solvency. To protect financial health, take action and get more cash into your business — by reducing expenses, increasing revenue, improving accounts receivable or even seeking financing.

16. Follow up on outstanding payments.

The terms “outstanding” and “overdue” are frequently used as synonyms to describe the state of an invoice. But the two words are not interchangeable. An outstanding invoice is an invoice that was sent out but has not yet been paid. An overdue invoice is an invoice that has passed its due date and still has not been paid. In other words, all unpaid invoices are outstanding but not all are overdue.

So why would an outstanding invoice be a problem? A customer may still pay before the due date, so why spend time and money chasing it? Two reasons:

- Get cash sooner. The sooner a business gets paid, the more liquidity it has — and the more funds to cover payroll and daily operations, or even invest in things that will drive future growth.

- Uncover potential customer problems early. When customers don’t pay promptly, it can mean they had a problem with the product or service, a disagreement about price or some other simmering discontent that should be resolved ASAP. Touching base can reveal issues that would delay payment.

KPIs, like days sales outstanding and accounts receivable turnover, can help a company gauge its billing and collection processes. If numbers are lower than desired or the business has been finding itself cash poor, despite being profitable, it’s time to start following up with customers. Here are a few tips:

- Invest in automated accounts receivable technology. Using a system that automatically invoices customers and reminds them of due dates limits the length of time your accounts receivable team needs to chase payments.

- Take a personal approach. A personal phone call or an informal email can help you understand why the customer hasn’t yet paid and when to expect the payment, if ever. This can help reveal the severity of the situation. Try to resolve any disagreements or misunderstandings on a friendly basis.

- Negotiate a payment plan. If a customer expects to make a late payment for a valid reason — perhaps their own cash flow is ebbing and flowing unevenly — it can help to establish a payment plan. This is a win-win for all: You get paid while salvaging the relationship. It also saves the cost and hassle of being forced to seek legal remedies.

- Hire a debt collection agency. This is a more drastic step and relevant only with overdue invoices. When an account is transferred to an agency for collection, the total owed must be deeply discounted. Many such agencies will offer instant cash payment on unpaid invoices, helping improve liquidity.

- Initiate legal action. Sometimes the courts are necessary, but it’s generally best to avoid this step because of the expense and hassle — and it’s relevant only for overdue invoices. Before taking legal action, send a formal letter of intent to let the customer know what’s looming if they don’t pay up. This in itself can trigger favorable results.

17. Apply for business financing.

Businesses that are trying to grow or improve financial performance often feel constrained by a lack of cash. They can be successful, even profitable, but, for various reasons, lack the liquidity needed to reach the next stage. A cash infusion via business financing can improve financial performance enough to stimulate progress. Financing can help a business broaden operations, expand to a larger facility, purchase inventory and equipment, hire additional staff or cover unexpected expenses. Financing can also be used to improve cash flow, invest in marketing and advertising or simply take advantage of opportunities that arise.

Businesses have options when it comes to financing:

- SBA loans: These are government-backed loans designed to help small businesses obtain financing.

- Bank loans: Small businesses can also obtain loans from banks, credit unions and other financial institutions. These loans can be secured with collateral or unsecured. There are also specialized forms of bank financing, like equipment financing, which can help businesses purchase costly equipment.

- Crowdfunding: This is a method of raising capital through small contributions from a large number of people, typically via the internet. There are a number of crowdfunding platforms, each of which takes a percentage of the money raised.

- Angel investors and venture capital: Angel investors and venture capital firms provide equity financing to small or new businesses in exchange for an ownership stake in the company.

- Business credit cards: Some credit cards are specifically designed for small business use, facilitating cash advances that can be useful for businesses trying to manage cash flow more effectively.

- Invoice financing and factoring: Invoice financing allows a business to borrow money against outstanding invoices. Invoice factoring allows them to “sell” accounts receivable to a third party, at a discount.

Although business financing can help improve financial performance, it also requires taking on debt — and debt comes with interest and other fees. And if a business relies too heavily on debt to fund operations, the company’s financial health is more vulnerable to risks, such as economic downturns or spiking variable interest rates. The debt-to-equity ratio is a commonly used financial ratio to determine if a business is taking on too much debt.

Debt-to-equity = Total liabilities / Total shareholder equity

It depends on the industry, but a debt-to-equity ratio of 1 or less is generally considered good. A ratio of 2 or more could be a red flag that the business might have financial trouble in the future. If a business is already relying on financing to fund operations, it may not be a good idea to apply for more financing.

18. Expand your customer base.

Your “customer base” is the group of people that regularly purchases your products or uses your services. They’re the lifeblood of the business and deliver the most long-term value.

When attempting to expand your customer base, keep in mind longer-term goals. You want repeat customers, not just one-offs or customers who divide their attention (and dollars) among brands. Extraordinary bargains, sales promotions and other attention-grabbing tricks won’t necessarily work to increase customer lifetime value, a key sales metric used to determine which customer segments generate the most revenue.

Customer lifetime value = (Average transaction size) x (Number of transactions) x (Retention period)

When you know how much you’ll earn from the typical customer, you can get a sense of how much to spend on new customer acquisition. For example, you might be able to increase spending to reach more customers and maximize profitability, or the figures might reveal a need to decrease customer acquisition costs. That said, comparing customer lifetime value to customer acquisition costs is key to homing in on a cost-effective strategy to expand your customer base.

Customer acquisition costs = Total sales & marketing costs / New customers

There’s a caveat to working hard to acquire new customers: You must simultaneously make sure to keep your existing customer base happy, as it costs more to acquire a new customer than it does to sell to an existing one. If churn rates start going up, it may be a sign that once-loyal customers are feeling neglected.

Customer churn = Number of customers lost in a period / (Number of customers at start of period + Number of customers at end of period)

With minimizing churn in mind, the cost of building your customer base will vary, based on your industry and sales strategy. Some associated costs include:

- Marketing and advertising expenses, such as online advertisements, social media campaigns or print ads.

- Sales team commissions.

- Trade show or other event expenses.

- Lead-generation costs, such as paying for a list of potential leads.

- Development costs to modify a product or service to meet the needs of a new (or new category of) customer.

One low-cost, but effective, way to improve your customer base is to make existing customers advocate for you through word-of-mouth marketing. Customer advocates write reviews, make referrals or allow their testimonials to be published on your website or in promotional materials. Customer advocates can dramatically improve a business’s reach and credibility. According to one survey, more than three-fourths of people (77%) “always” or “regularly” read reviews when searching for or evaluating a local business. And 89% say they would be “fairly” or “highly” likely to patronize a business that personally answers reviews, whether those reviews are positive or negative.

19. Consider external investment.

Not every company can grow organically throughout every stage of its business development journey. But finding external investors can help give a business the financial push it needs. And even if a business doesn’t need extra funding, per se, investors can bring more to the table than just capital. They can also provide the expertise and connections a business might need to innovate and grow beyond its current state. They may help with decision-making and strategic planning. Some investors may even be willing to help with hands-on management and operations. Done well, a round of investment funding can boost a business’s financial performance enough for it to reach the next level.

There are several sources of investment to consider, such as:

- Family and friends.

- Angel investors.

- Venture capitalists.

- Private equity firms.

- The public.

The ideal time to bring outside money into your business varies considerably from company to company. A young company still in its “seed” stage — meaning, it has a solid idea but might not yet have a product or be pulling in revenue — might look to family, friends or even angel investors as a source of external investment. Companies that already have a product in the works might be able to turn to venture capitalists, who generally tend to be a bit less adventurous than angel investors. Companies ready to expand, with a few years of solid footing under their belt, might look to go public by making an initial public offering (IPO). Or, if the company wants to scale up but stay private, they might look to a private equity firm.

Whatever type of investment a company seeks, it’s very important for the business owner to carefully consider the terms of any investment and the potential impact on the control and direction of their company. Capital is never free. In exchange for money, businesses almost always must give up partial ownership, or equity. This can dramatically reduce your influence on your own business. Private equity firms, for example, generally buy 100% of the company, whereas angel investors and venture capitalists might take 25% to 50% ownership, family and friends even less.

20. Upgrade your record-keeping with real-time data in NetSuite.

Because you can’t manage what you can’t measure, it’s essential to keep meticulous financial records of all your business activities. And if the goal is to improve business performance, it needs to be done in as close to real-time as possible — stale data leads to potentially misleading analysis and decision-making. Therefore, spreadsheets and on-premises solutions are out. Cloud-based financial management automation is in.

NetSuite financial management solutions are delivered via a cloud-based platform that offers real-time visibility into a business’s current financial performance, from a consolidated level down to individual transactions. Say goodbye to inaccurate financial reporting and hello to precise pictures of overall financial performance.

Generate financial reports that comprehensively reveal how the business is performing and access up-to-the-minute financial statements that comply with GAAP, IFRS and other accounting standards. Guide decision-making with what-if scenarios that reveal the potential and financial impact of any changes. Then, use personalized dashboards to drill down into underlying details and track key metrics over time. In addition, NetSuite seamlessly integrates with other business applications — including order management, inventory, CRM and ecommerce software — so you can run your entire business with a single solution.

The financial performance of a company is best represented by numbers. But you generally need to look at several metrics and financial reports before you have a solid understanding of a company’s financial soundness. If improving financial performance is the goal, common actions to take fall into several categories: cutting costs, managing debt, boosting revenue, looking to external sources and tightening financial management controls. But remember: Any actions taken to improve financial performance must be tracked and analyzed over time to ensure that your efforts are working as you expect.

Improve Financial Performance FAQs

What is financial performance?

Financial performance refers to how well a company is doing financially. It’s typically measured by analyzing financial statements, such as income statements, balance sheets and cash flow statements. Financial metrics and KPIs — such as revenue, net income, gross burn rate and return on assets, among many others — should also be assessed.

Why is financial performance important?

Financial performance is important because it allows a business to measure its success, identify areas for improvement, make informed decisions, attract investors or secure funding. Additionally, financial performance can also affect the business’s ability to pay employees, suppliers and taxes, as well as its ability to expand or grow in the future.

What are financial performance indicators?

Financial performance indicators are metrics used to evaluate the financial performance of a company or organization. They include measures such as revenue, profit, return on investment (ROI), return on assets, debt-to-equity ratio and many others. These indicators are used to assess a company’s financial health and to make investment decisions.

What is a financial performance analysis?

Financial performance analysis is the process of evaluating a company’s financial performance and position by analyzing financial statements, including the balance sheet, the income statement and the cash flow statement. This analysis can be used to assess the company’s overall financial health, identify trends and opportunities for growth and make informed investment decisions. It typically involves comparing the company’s financial performance to industry averages or other benchmark data and may also include an analysis of the company’s management and operations.

How do you build a financial performance?

There are several ways to build a small business’s financial performance. Here are a handful:

- Increase revenue through sales and marketing efforts.

- Decrease expenses by streamlining operations or cutting overhead costs.

- Improve cash flow by managing accounts receivable and payable effectively.

- Utilize financial tools, such as budgeting and forecasting, to make informed decisions.

- Consider seeking external funding or investment to support growth.

- Seek professional advice from an accountant or financial adviser.

What is financial performance of a company?

Financial performance refers to how well a company is doing financially, typically measured by analyzing financial statements, such as income statements, balance sheets and cash flow statements. Key indicators of financial performance include revenue, net income and return on investment (ROI).