Cash flow is the lifeblood of growing businesses, essential for covering costs in every area of their operations. Yet it’s the rare business that isn’t occasionally affected by slow or uneven cash flows. In some cases, poor cash flow may mean missing out on an opportunity to grow the business. In other cases, consequences can be as dire as a company going out of business because it can’t pay its debts.

Invoice factoring is one way to smooth out cash flow challenges. Typically used by small and medium-sized businesses (SMB) in business-to-business (B2B) industries, the process involves the sale of unpaid invoices to a third party, known as a factor or factoring company, which retains a percentage of the original invoice amount. For a small company, factoring often provides faster access to cash than bank financing because factors are less likely to be deterred by a small company’s credit history.

What Is Invoice Factoring?

Invoice factoring is a financial agreement where businesses sell their unpaid invoices to a third-party company, called a factor, who gives the business a percentage—typically 70% to 90%—upfront, paying the rest, minus a 2% to 5% fee, after the customer pays. With invoice factoring, the company gets immediate cash, rather than waiting 30, 60, or 90 days for customer payment.

In most factoring arrangements, the factor assumes responsibility for collecting payments from the customer. Unlike traditional financing, this is an asset sale, rather than a loan, that helps businesses convert their accounts receivable into working capital quickly, improving cash flow for operations, growth initiatives, or meeting immediate financial obligations.

Key Takeaways

- Invoice factoring involves selling unpaid invoices to a third-party company so that a business can improve its cash flow in order to fund operations or pursue growth opportunities.

- A factoring company pays the business the majority of the invoice up front and the balance when the invoice is paid by the customer, minus its factoring fee.

- Invoice factoring is most often used by growing businesses that don’t have the time or necessary credit to get a bank loan.

- Downsides include higher costs than those related to conventional bank loans and diminished control over customer interactions.

Invoice Factoring Explained

Most companies need to be profitable to stay in business—i.e., their revenues must exceed their expenses. But profitability doesn’t always equate to positive cash flow. If a company has customers with extended payment terms it can make it difficult for them to meet their financial obligations. This situation can become almost as perilous as if the company’s entire business is unprofitable.

Invoice factoring is a way to cushion some of the effects of delayed payments and the cash flow problems they may create. The approach is most often used by startups and growing companies that are trying to act quickly and may not want to go through the conventional bank loan application process. Factoring can be more costly than other kinds of financing, but many companies like the assurance it provides that they’ll obtain needed cash quickly.

Why Is Factoring Important?

Factoring alleviates cash flow concerns during a slow period, especially for companies with few resources and slow-paying customers. Just about every small-business owner knows what it’s like to lie awake at night wondering whether they’re going to be able to make their payroll or cover some other critical business expense. A lack of cash could also keep a business from paying its own vendors on time or from seizing an opportunity such as working with a major new retailer in time for the holidays or expanding internationally. Cash-strapped companies have little choice but to make short-term decisions that may cut off or limit long-term opportunities.

Invoice Factoring vs. Other Financing Options

Invoice factoring is just one of several options for businesses seeking to accelerate cash flow from accounts receivable. Alternative approaches, such as invoice financing and invoice discounting, also allow companies to gain immediate cash from pending receivables—but with different approaches to ownership and collection. Each method has different impacts on cost, control, and customer relationships, and the right choice depends on specific needs and circumstances.

Invoice factoring vs. Invoice Financing

Invoice factoring and invoice financing are two types of accounts receivable financing. Invoice financing is similar to invoice factoring in that it’s a way for businesses to get paid quickly on an invoice, rather than having to wait weeks or months before payment is officially due. However, invoice financing doesn’t involve selling invoices. Rather, the company uses them as collateral for borrowing money from a lender. Collection remains the company’s responsibility. Invoice financing involves somewhat less work than invoice factoring; hence, the associated fee is usually somewhat lower than that incurred through invoice factoring. This option appeals to businesses that need accelerated cash flow but prefer their internal collections processes to protect their customer relationships.

Invoice Factoring vs. Invoice Discounting

Invoice discounting is another form of receivables-based funding where companies borrow against invoices, rather than selling them. Discounting follows a similar cash timeline as invoice factoring—discounters pay a large percentage upfront, with the rest following (minus fees) when the customer pays. But unlike factoring, the arrangement typically remains confidential, with customers paying the business directly, unaware of the financing agreement. Like invoice financing, the business retains full responsibility for collections, making it a popular choice for companies with established accounts receivable processes. Because of these reduced services, invoice discounting generally costs less than factoring but requires strong credit and more collections capabilities.

Invoice Factoring vs. Financing vs. Discounting

| Invoice Factoring | Invoice Financing | Invoice Discounting | |

|---|---|---|---|

| Transaction type | Sale | Loan | Loan |

| Who collects payment | Financer | Business | Business |

| Confidentiality | Customers notified | May or may not be disclosed | Typically confidential (customers remain unaware) |

| Credit requirements | Based on customer credit | Based on business credit | Based on business credit |

| Control over receivables | Financer controls collections | Business controls collections | Business controls collections |

| Cost level | Highest | Moderate | Lowest |

| Best for | Companies outsourcing collections | Companies with existing collections processes | Companies with existing collections processes |

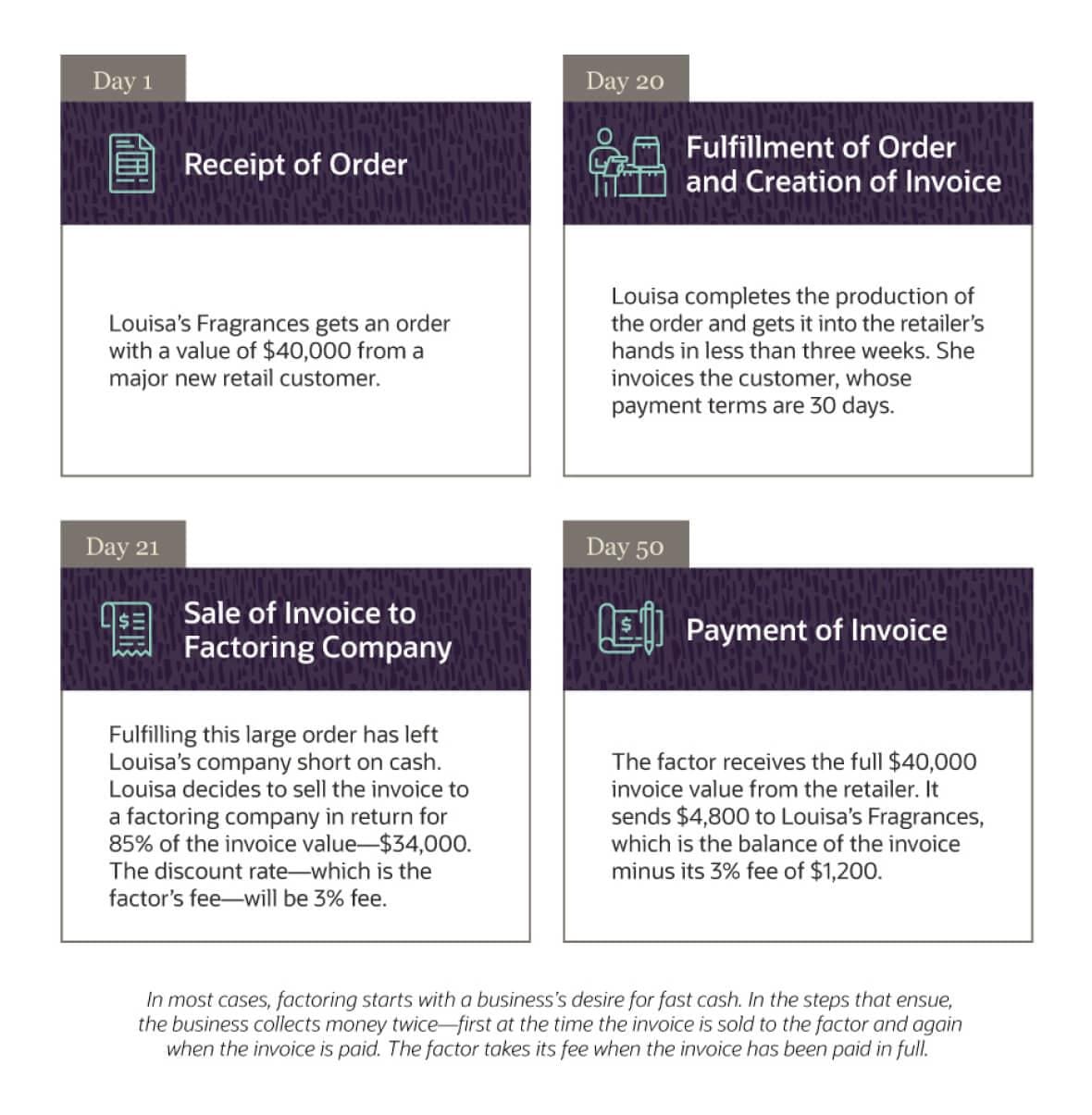

How Does Invoice Factoring Work?

In a typical business situation, a company makes a sale, creates an invoice, and sends it to the customer. 30, 60, or 90 days after the good or service is delivered, as stipulated on the invoice, the buyer pays for the purchase, and the company gets its money.

But what if the company finds itself in a position where, for any number of reasons, it can’t wait? With invoice factoring, the company can sell the invoice to a third party, called a factoring company or factor, which buys unpaid invoices at a discount. The factor negotiates the amount they’re willing to pay and agrees to payment terms—a certain amount will often be paid up front, with the remainder being paid after the factor collects.

Bear in mind, not every invoice is a good candidate for factoring. Most factors won’t buy invoices that are already past due, and many won’t buy invoices whose payment terms exceed 90 days.

The process of invoice factoring, using a hypothetical company, looks like this:

How Invoice Factoring Works

When determining whether to purchase an invoice, the factoring company will examine a business’s customers and the likelihood they will remit the full value of the invoice. To this end, the factor will look at the customers’ credit ratings, try to assess their accounts payable performance, and consider other issues that may affect payment, such as outstanding litigation. The factor must also make sure the invoice is valid, which may include a review of shipping statements and other documentation.

Recourse Factoring vs. Non-Recourse Factoring

Most factoring agreements include a “recourse” provision, meaning the company selling the invoice must return some or all of the advance cash payment if a customer doesn't pay. If a customer fails to pay within a specified timeframe (90 days, for example), the business must buy back the unpaid invoice or replace it with another invoice of equal value. This reduces the factor’s risk by returning some responsibility to the business, which contributes to recourse factoring’s lower fees (typically 1% to 3%) and higher initial payment percentages than non-recourse factoring.

Non-recourse factoring clauses shift the credit risk to the factor, except in specific situations like customer bankruptcy or insolvency. Disputes over product quality, service delivery, or contract terms may or may not qualify for non-recourse, depending on the factor’s terms. Non-recourse protections often come at a premium, typically costing 1% to 2% more than recourse factoring. The choice between recourse and non-recourse depends on customer creditworthiness and the business’s risk tolerance—companies with reliable customers may choose recourse factoring to minimize costs, while those dealing with less creditworthy customers or large invoices might find the risk mitigation from non-recourse worth the added expense.

When Should Companies Use Invoice Factoring?

Invoice factoring generally makes the most sense for growing B2B businesses with good—but often slow-paying—customers. The definition of “slow,” of course, is relative to the business’s point of view, but even standard net 30 payment terms can be problematic if the invoice is a big part of the company’s near-term revenues. It can make or break a company’s ability to take advantage of a new business opportunity, particularly if it does not have enough business history or collateral to secure a line of credit with a bank or a decision must be made before a loan application process can be completed. That brings us to one of the benefits of using invoice factoring: The company’s own credit matters less than that of its customers, who are, after all, the ones who will be paying the factor.

A business might also turn to factoring so its employees in finance don’t have to spend time on collections, which can be a frustrating and thankless activity.

Advantages of Invoice Factoring

A business may consider invoice factoring for a variety of reasons. Here are five of the most important:

-

Fast receipt of cash:

Companies that work with third-party factors typically receive a substantial portion of the value of their invoices within a few business days—sometimes within 24 hours. That timely cash flow can provide smaller companies, in particular, with peace of mind about their ability to cover near-term expenses.

-

Removal of a likely distraction:

Slow-paying customers—and, of course, those whose bills are overdue—can cause big headaches, especially for small businesses. If it’s the owner who has to follow up on a late invoice, that’s time not spent with other customers or on higher-value activities. If an accounts receivable department handles collections, the tedious time spent chasing down a delayed payment may impact morale.

-

Quicker approvals than with bank loans:

Bank loans or lines of credit are certainly a possibility for access to cash. But they can take a long time to get and, for many small businesses, may be capped at levels that limit the company’s ability to grow. The approval process for invoice factoring is much faster, and, given how the arrangement works, factors often provide more cash than banks.

-

Less scrutiny of a founder’s personal credit history:

Bank loans typically depend, in part, on the credit score of the company’s founder. This can be problematic for many small-business owners, especially if funding the business has required significant credit card use. Fortunately, an invoice factor is more interested in the credit rating of the customer that has placed an order than in the company whose invoices it purchases.

-

Helping businesses work with important new customers and accounts:

Some very big and otherwise reliable customers have payment schedules that may be too stretched out for small businesses. The problem of payment timing could possibly complicate their ability to fulfill a very large, potentially fortune-changing, order, such as one from a government entity or a Fortune 500 company. Invoice factoring may help them fulfill these new orders.

Disadvantages of Invoice Factoring

Factoring also has some downsides that a business should consider before selling an invoice to a third party. Disadvantages include:

-

Requires a big commitment:

Factoring companies occasionally provide so-called “spot,” or selective, factoring, meaning that they offer their services for a single invoice. More often, though, factoring companies only work with businesses that are willing to turn over most or all of their invoices. Sometimes a contractual minimum is set and a fee is charged when invoices don’t meet that minimum.

-

Can be expensive:

As with bank loans, a factor’s fees are partially dependent on perceived risk—though with factoring, the credit assessment is of a company’s customers, not the company itself. Even in cases where the risk of nonpayment is low, a factor’s fees are generally several percentage points higher than the percentage a business would pay in interest for a bank loan.

-

Doesn’t shift the payment risk:

Working with a factor means an earlier receipt of cash, but it doesn’t necessarily offer a company protection against a nonpaying customer. If an invoice goes unpaid, the selling company must typically return the cash advanced by the factor unless a “non-recourse” clause is in place. However, inclusion of this clause increases the price of the arrangement.

-

Allows less control over certain customer interactions and impressions:

In most factoring arrangements, the factor takes responsibility for making sure that the invoice gets paid. This is part of the value of factoring—one less chore for a company selling an invoice to worry about. But it also means the company loses control over the handling of collection requests. An overly aggressive factor, focused on its own short-term needs, could negatively affect a customer’s impressions of the company it purchased from. A factor’s presence may also lead customers to think that the company doesn’t have the proper resources to handle its business.

These downsides can be managed. For instance, a company can opt for confidential factoring, wherein the factor represents itself as part of the company’s financing department. Or it can opt to handle its own invoice-collection efforts, even after ownership of the invoice has passed to a factor. This is known as “CHOCC” factoring—short for “client handles own credit control.” But these approaches come with their own inherent risks, as well.

Invoice Factoring Example

Sophie’s Churn, a hypothetical maker of premium yogurt in Portland, Oregon, achieved local success selling to gourmet stores and a big co-op in its health-conscious home city. It hand-assembled and sold 2,000 units a month with the help of two employees.

After being featured on a network television show, Sophie’s Churn was approached by a national grocery chain that wanted to purchase 20,000 units of the yogurt. This is windfall for Sophie’s Churn, adding $80,000 in monthly revenue based on its per-unit wholesale price.

Fulfilling the order was going to cost the company $49,000, and the $56,000 Sophie’s Churn had in its bank account seemed ample. But with only $7,000 remaining on the day Sophie’s Churn fulfilled the order, and 45 days until payment was due, the owner was feeling uneasy. So she approached a factoring company with experience in the food service and retail industries. The factoring company checked to make sure that the grocer—which owed the money—didn’t pose a payment risk, and two days later it agreed to buy the invoice. It charged a 5% fee, or $4,000, on the total invoice value ($80,000). The next day, the factor wired $64,000 to the business account of Sophie’s Churn—the pre-agreed 80% of the order’s value to be paid up front. When the grocer paid the invoice six weeks later, the factoring company paid Sophie’s Churn another $12,000—the unpaid portion of the invoice minus its $4,000 fee.

Cost of Invoice Factoring

Understanding the complete costs associated with invoice factoring helps businesses strategically choose which invoices to factor and when by evaluating the immediate cash flow benefits against the total expense. The actual cost often goes beyond the basic fees explored above, involving multiple components that can increase prices above the advertised rate. These components typically include both percentage-based fees and fixed charges based on invoice characteristics, customer profiles, and contract terms.

- Discount rate: This primary fee can be a flat percentage (3% regardless of payment timing, for example) or tiered rates that increase over time (2% for 30 days, then 0.5% per additional 10 days). Rates vary based on industry risk, invoice size, and customer creditworthiness, with large invoices in low-risk industries typically receiving better terms.

- Service fees: Administrative charges beyond the discount rate include a flat setup fee, monthly minimums that guarantee the factor's revenue regardless of volume, or transaction fees for wire transfers and credit checks. These additional costs are especially common for large batches of factored invoices and usually add 0.5% to 2% to the effective rate.

As an example, say a business factors a $10,000 invoice with 30-day terms. The factor offers an 85% advance rate with a 2% discount rate for 30 days and a $50 service fee.

- Advance amount: $8,500 (85% of $10,000)

- Total fees: Discount fee of $200 (2% of $10,000) + Service fee of $50 = $250

- Reserve amount returned if customer pays on time: $1,250 ($10,000 - $8,500 - $250)

In this scenario, the effective cost to the business for receiving $8,500 immediately instead of waiting 30 days is $250, or about 2.5% of the invoice value.

Leveraging Software to Manage Cash Flow

Managing cash flow requires financial visibility, accurate revenue and expense forecasts, and detailed analysis that informs when to use financing options like invoice factoring. NetSuite Financial Management provides comprehensive tools, such as automated invoice tracking, to identify aging receivables before they impact cash flow. Customizable dashboards display key metrics, such as days sales outstanding (DSO) or financial performance KPIs, alongside automated payment reminders and collection workflows that help AR teams accelerate customer payments to reduce the need for factoring. During cash flow constraints, real-time forecasting allows businesses to predict funding gaps and determine if and when to factor an invoice.

NetSuite Bill Capture further enhances cash flow management by providing visibility into upcoming payment obligations, helping businesses align factoring decisions with payables schedule. By centralizing both incoming and outgoing financial data, businesses can make data-driven decisions on factoring, internal collections, and traditional financing to optimize working capital management while minimizing costs.

NetSuite’s Invoice Software

Cash flow constraints are an undeniable business impediment. Invoicing factoring is one way to address the problem. By selling unpaid invoices to a third-party factoring company, a business receives the majority of their value within a few business days. It then has the cash on hand to fulfill new orders, pay its own expenses and pursue growth opportunities. The business receives the remainder of the invoice’s value when the factoring company collects payment from the customer. For many small businesses that can’t or don’t want to work with banks, factoring is an attractive financing option.

Invoice Factoring FAQs

Is invoice factoring a good idea?

It depends on who is seeking the funding. Invoice factoring isn’t widely used by large companies with access to bank loans or lines of credit. Small and medium-sized businesses may find invoice factoring appealing as a means of helping them improve their cash flow and obtaining the funds they need to pay their expenses.

How much does factoring invoices cost?

The main cost of invoice factoring is the so-called discount rate on the invoice. This is typically between 2% and 5% of the invoice’s total value, though the rate can be outside this range depending on the volume of business and the risk the factoring company is taking.

What is the difference between invoice factoring and financing?

Both are mechanisms that growing businesses may use to generate cash. In invoicing factoring, the invoice is sold to a factoring company, which also assumes responsibility for collection. In invoice financing, the invoice serves as collateral for either a term or a revolving loan from a financial company.

Do banks do invoice factoring?

Yes, some banks offer invoice factoring services, typically through specialized divisions or subsidiaries/partnerships rather than as a core service. Banks with factoring operations generally focus on clients with substantial invoice volumes and often have more stringent qualifications than factor companies. However, most factoring is provided by independent factoring companies rather than traditional banks.