Finance teams that want to know whether their companies can withstand an unexpected downturn or crisis need a handle on two metrics: working capital and cash flow. These two metrics illustrate different aspects of a company’s financial health.

While cash flow measures how much money the company generates or consumes in a given period, working capital is the difference between the company’s current assets—including cash and other assets that can be converted into cash within a year—and its current liabilities, such as payroll, accounts payable, and accrued expenses. A business that maintains positive working capital will likely have a greater ability to withstand financial challenges and the flexibility to invest in growth after meeting short-term obligations.

What Is Working Capital?

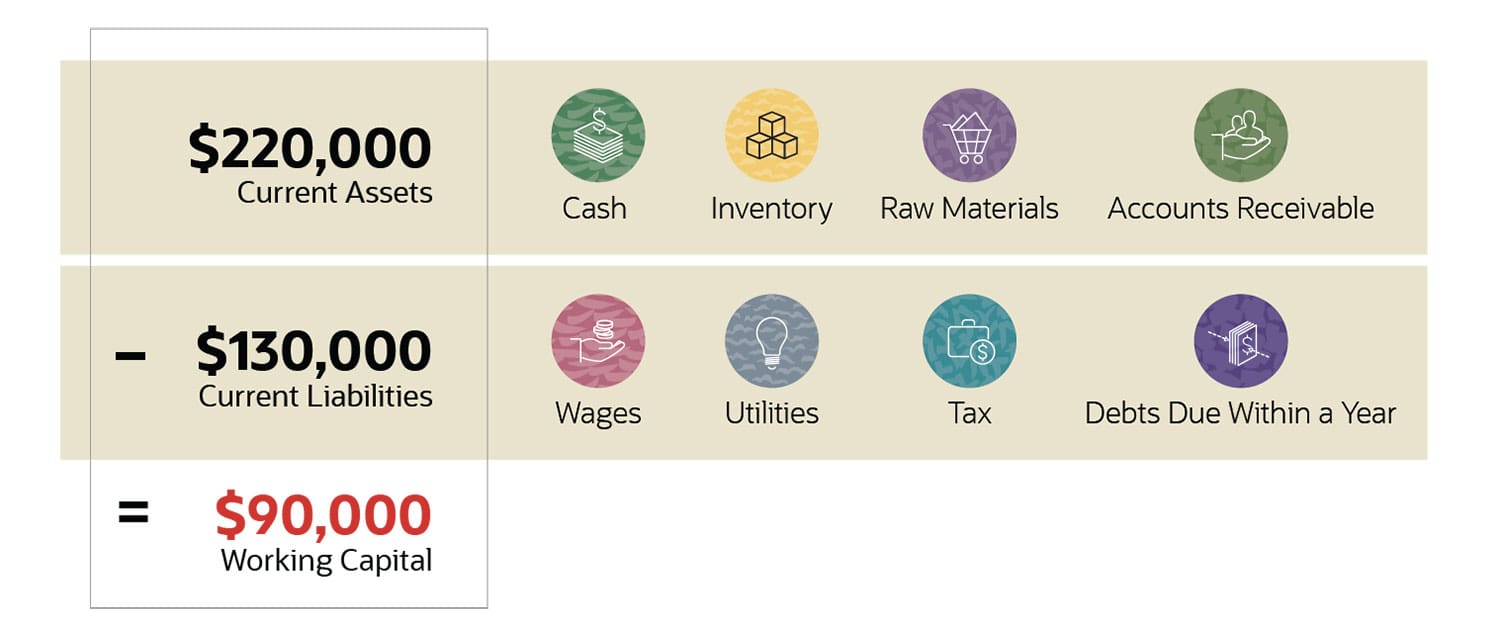

Working capital is calculated by subtracting current liabilities from current assets, as listed on the company’s balance sheet. Current assets include cash, accounts receivable, and inventory. Current liabilities include accounts payable, taxes, wages, and interest owed.

Key Takeaways

- Working capital is a financial metric calculated as the difference between current assets and current liabilities.

- Positive working capital means the company can pay its bills and invest to spur business growth.

- Working capital management focuses on ensuring that the company can meet day-to-day operating expenses while using its financial resources in the most productive and efficient way.

Working Capital Explained

Working capital is a financial metric that is the difference between a company’s current assets and current liabilities. As a financial metric, working capital helps plan for future needs and ensure that the company has enough cash and cash equivalents to meet short-term obligations, such as unpaid taxes and short-term debt.

Example: A manufacturer has assets totaling $220,000 and liabilities totaling $130,000, which means it has positive working capital of $90,000.

Why Is Working Capital Important?

Working capital is used to fund operations and meet short-term obligations. If a company has enough working capital, it can continue to pay its employees and suppliers and meet other obligations, such as interest payments and taxes, even if it runs into cash flow challenges.

Working capital can also be used to fund business growth without incurring debt. If the company does need to borrow money, demonstrating positive working capital can make it easier to qualify for loans or other forms of credit.

For finance teams, the goal is twofold: Have a clear view of how much cash is on hand at any given time, and work with the business to maintain sufficient working capital to cover liabilities, plus some leeway for growth and contingencies.

Advantages of Working Capital

Working capital can help smooth out fluctuations in revenue. Many businesses experience some seasonality in sales—selling more during some months than others, for example. With adequate working capital, a company can make extra purchases from suppliers to prepare for busy months while meeting its financial obligations during periods where it generates less revenue.

For example, a retailer may generate 70% of its revenue in November and December—but it needs to cover expenses, such as rent and payroll, all year. By analyzing its working capital needs and maintaining an adequate buffer, the retailer can ensure that it has enough funds to stock up on supplies before November and hire temps for the busy season while planning how many permanent staff it can support.

Working Capital and the Balance Sheet

Working capital is calculated from current assets and current liabilities reported on a company’s balance sheet. A balance sheet is one of the three primary financial statements that businesses produce; the other two are the income statement and cash flow statement.

The balance sheet is a snapshot of the company’s assets, liabilities, and shareholders’ equity at a moment in time, such as the end of a quarter or fiscal year. The balance sheet includes all of a company’s assets and liabilities, both short- and long-term.

The balance sheet lists assets by category in order of liquidity, starting with cash and cash equivalents. It also lists liabilities by category, with current liabilities first followed by long-term liabilities.

How to Calculate Working Capital

Working capital is calculated as current assets minus current liabilities, as detailed on the balance sheet.

Formula for Working Capital

The formula for working capital is as follows:

Working capital = Current assets – Current liabilities

Positive vs. Negative Working Capital

A company has positive working capital if it has enough cash, accounts receivable, and other liquid assets to cover its short-term obligations, such as accounts payable and short-term debt.

In contrast, a company has negative working capital if it doesn’t have enough current assets to cover its short-term financial obligations. A company with negative working capital may have trouble paying suppliers and creditors and difficulty raising funds to drive business growth. If the situation continues, it may eventually be forced to shut down.

Elements Included in Working Capital

The current assets and liabilities used to calculate working capital typically include the items detailed below.

Current Assets

Current assets are cash and other liquid assets that can be converted into cash within one year of the balance sheet date, including:

- Cash, including money in bank accounts and undeposited checks from customers

- Marketable securities, such as U.S. Treasury bills and money market funds

- Short-term investments that a company intends to sell within one year

- Accounts receivable, minus any allowances for accounts that are unlikely to be paid

- Notes receivable—such as short-term loans to customers or suppliers—maturing within one year

- Other receivables, such as income tax refunds, cash advances to employees, and insurance claims

- Inventory, including raw materials, work in process, and finished goods

- Prepaid expenses, such as insurance premiums

- Advance payments on future purchases

Current liabilities

Current liabilities are expenses due within a year of the balance sheet date, including:

- Accounts payable

- Notes payable due within one year

- Wages payable

- Taxes payable

- Interest payable on loans

- Any loan principal that must be paid within a year

- Other accrued expenses payable

- Deferred revenue, such as advance payments from customers for goods or services not yet delivered

Working Capital Challenges

Working capital represents the funds available for day-to-day operations. However, managing working capital effectively isn’t without its challenges. Companies often face numerous obstacles that can impede their ability to maintain optimal cash flow and operational efficiency. They include:

- External disruptions: Unexpected events outside a company’s control can significantly impact working capital. For example, economic downturns, natural disasters, and global pandemics can disrupt supply chains, reduce customer demand, or cause unexpected expenses, all of which strain a company’s working capital position.

- Poor cash flow management: The ineffective handling of cash inflows and outflows can lead to liquidity issues. Poor cash flow management often results from delayed customer payments, overextended credit to customers, or poor timing of payables. These factors can leave a company short on cash to cover its short-term obligations and operational needs.

- Substandard lending practices: This involves either borrowing on unfavorable terms or extending credit to customers without proper vetting. Such practices can lead to high-interest expenses, increased bad debt, or cash tied up in receivables, all of which negatively impact working capital.

- Inaccurate forecasting: This occurs when a company fails to predict its future cash needs and cash generation accurately. Inaccurate forecasts can result in poor decision-making regarding inventory purchases, staffing levels, and capital investments, potentially causing cash shortages or inefficient use of available funds.

- Ineffective inventory management: This challenge arises when a company carries too much or too little inventory. Excess inventory ties up cash and increases storage costs, while insufficient inventory can lead to lost sales and dissatisfied customers. Both scenarios negatively impact working capital.

Working Capital Example

The following working capital example is based on the March 31, 2020, balance sheet of aluminum producer Alcoa Corp., as listed in its 10-Q SEC filing. All amounts are in millions.

Alcoa listed current assets of $3,333 million, and current liabilities of $2,223 million. Its working capital was therefore $3,333 million – $2,223 million = $1,110 million. That represented an increase of $143 million compared with three months earlier, on Dec. 31, 2019, when the company had $967 million in working capital.

| March 31, 2020 | December 31, 2019 | |||||

|---|---|---|---|---|---|---|

| ASSETS | ||||||

| Current assets: | ||||||

| Cash and cash equivalents | $829 | $879 | ||||

| Receivables from customers | 570 | 546 | ||||

| Other receivables | 95 | 114 | ||||

| Inventories | 1,509 | 1,644 | ||||

| Fair value of derivative instruments | 53 | 59 | ||||

| Prepaid expenses and other current assets | 277 | 288 | ||||

| Total current assets | 3,333 | 3,530 | ||||

| Properties, plants, and equipment | 20,181 | 21,715 | ||||

| Less: accumulated depreciation, depletion, and amortization | 13,021 | 13,799 | ||||

| Properties, plants, and equipment, net | 7,160 | 7,916 | ||||

| Investments | 1,059 | 1,113 | ||||

| Deferred income taxes | 425 | 642 | ||||

| Fair value of derivative instruments | 446 | 18 | ||||

| Other noncurrent assets | 1,228 | 1,412 | ||||

| Total assets | $13,651 | $14,631 | ||||

| LIABILITIES | ||||||

| Current liabilities: | ||||||

| Accounts payable, trade | $1,276 | $1,484 | ||||

| Accrued compensation and retirement costs | 353 | 413 | ||||

| Taxes, including income taxes | 78 | 104 | ||||

| Fair value of derivative instruments | 80 | 67 | ||||

| Other current liabilities | 435 | 494 | ||||

| Long-term debt due within one year | 1 | 1 | ||||

| Total current liabilities | 2,223 | 2,563 | ||||

| Long-term debt, less amount due within one year | 1,801 | 1,799 | ||||

| Accrued pension benefits | 1,455 | 1,505 | ||||

| Accrued other postretirement benefits | 729 | 749 | ||||

| Asset retirement obligations | 548 | 606 | ||||

| Environmental remediation | 289 | 296 | ||||

| Fair value of derivative instruments | 164 | 581 | ||||

| Noncurrent income taxes | 299 | 276 | ||||

| Other noncurrent liabilities and deferred credits | 332 | 370 | ||||

| Total liabilities | 7,840 | 8,745 | ||||

How Working Capital Affects Cash Flow

Cash flow is the amount of cash and cash equivalents that moves in and out of the business during an accounting period. Cash flow is summarized in the company’s cash flow statement.

A company’s cash flow affects its amount of working capital. If revenue declines and the company experiences negative cash flow as a result, it will draw down its working capital. Investing in increased production may also result in a decrease in working capital.

Working Capital vs. Net Working Capital

The terms “working capital” and “net working capital” are synonymous: Both refer to the difference between all current assets and all current liabilities.

However, some analysts define net working capital more narrowly than working capital. One of these alternative formulas excludes cash and debt:

Net working capital = Current assets (less cash) – Current liabilities (less debt)

An even narrower definition excludes most types of assets, focusing only on accounts receivable, accounts payable, and inventory:

Net working capital = Accounts receivable + Inventory – Accounts payable

Working Capital vs. Fixed Assets/Capital

Working capital includes only current assets, which have a high degree of liquidity—they can be converted into cash relatively quickly. Fixed assets are not included in working capital because they are illiquid; that is, they cannot be easily converted to cash.

Fixed assets include real estate, facilities, equipment, and other tangible assets, as well as intangible assets like patents and trademarks.

What Is Working Capital Management?

Working capital management is a financial strategy that involves optimizing the use of working capital to meet day-to-day operating expenses while helping ensure that the company invests its resources in productive ways. Effective working capital management enables the business to fund the cost of operations and pay short-term debt.

Several financial ratios are commonly used in working capital management to assess the company’s working capital and related factors.

The working capital ratio, also known as the current ratio, is a measure of the company’s ability to meet short-term obligations. It’s calculated as current assets divided by current liabilities.

A working capital ratio of less than one means a company isn’t generating enough cash to pay down the debts due in the coming year. Working capital ratios between 1.2 and 2.0 indicate a company is making effective use of its assets. Ratios greater than 2.0 indicate the company may not be making the best use of its assets; it is maintaining a large amount of short-term assets instead of reinvesting the funds to generate revenue.

The average collection period measures how efficiently a company manages accounts receivable, which directly affects its working capital. The ratio represents the average number of days it takes to receive payment after a sale on credit. It’s calculated by dividing the average total accounts receivable during a period by the total net credit sales and multiplying the result by the number of days in the period.

The inventory turnover ratio is an indicator of how efficiently a company manages inventory to meet demand. Tracking this number helps companies ensure that they have enough inventory on hand while avoiding tying up too much cash in inventory that sits unsold.

The inventory turnover ratio indicates how many times inventory is sold and replenished during a specific period. It’s calculated as cost of goods sold (COGS) divided by the average value of inventory during the period. A higher ratio indicates inventory turns over more frequently.

Working Capital: The Quick Ratio and Current Ratio

Analysts and lenders use the current ratio (working capital ratio) as well as a related metric, the quick ratio, to measure a company’s liquidity and ability to meet its short-term obligations.

These two ratios are also used to compare a business’s current performance with prior quarters and to compare the business with other companies, making it useful for lenders and investors.

Quick Ratio

The quick ratio differs from the current ratio by including only the company’s most liquid assets—the assets that it can quickly turn into cash. These are cash and equivalents, marketable securities, and accounts receivable.

Current Ratio

In contrast, the current ratio includes all current assets, including assets that may not be easy to convert into cash, such as inventory.

Because of this, the quick ratio can be a better indicator of the company’s ability to raise cash quickly when needed.

Does Working Capital Change?

For most companies, working capital constantly fluctuates; the balance sheet captures a snapshot of its value on a specific date. Many factors can influence the amount of working capital, including big outgoing payments and seasonal fluctuations in sales.

6 Ways to Increase Working Capital

A business may wish to increase its working capital if, for example, it needs to cover project-related expenses or experiences a temporary drop in sales. Tactics to bridge that gap involve either adding to current assets or reducing current liabilities. Options include:

- Taking on long-term debt to increase current assets by adding to the company’s available cash but not overly increasing current liabilities.

- Refinancing short-term debt as longer-term debt to reduce current liabilities because the debts are no longer due within a year.

- Selling illiquid assets for cash, thus increasing current assets.

- Analyzing and reducing expenses, thereby reducing current liabilities.

- Analyzing and optimizing inventory management to reduce overstocking and the likelihood that inventory will need to be written off.

- Automating accounts receivable and payment monitoring to increase cash flow and reduce the need to draw on working capital for day-to-day operations.

Manage Working Capital With NetSuite

With NetSuite cloud accounting software, businesses can transform their general ledger, optimize accounts receivable, automate accounts payable, and streamline tax management with embedded AI capabilities. By providing a complete view of cash flow and financial performance, NetSuite empowers finance teams to be more strategic than ever before. Additionally, NetSuite accounting software seamlessly integrates with all the other modules of the NetSuite ERP solution to provide strong compliance management, improve business performance, and increase financial close efficiency—all while reducing back-office costs.

Manage Cash Flow With NetSuite

Effective working capital management is crucial for the financial health and operational success of any business. By understanding the components of working capital, recognizing common challenges, and implementing strategies to optimize its use, companies can make sure they have the necessary liquidity to meet short-term obligations, weather unexpected disruptions, and invest in growth opportunities. Regular monitoring of working capital metrics, coupled with proactive management of cash flow, inventory, and accounts receivable and payable, can significantly enhance a company’s financial stability and competitive position.

Working Capital FAQs

Why isn’t cash a part of working capital?

Cash actually is a part of working capital. As a current asset, cash is included in the calculation of working capital, which is the difference between current assets and current liabilities.

What is a good working capital ratio?

A good working capital ratio typically falls between 1.2 and 2.0. This range indicates that a company has enough current assets to cover its current liabilities and is making effective use of its assets without holding excessive idle resources.

What are the main objectives of working capital management?

The main objectives of working capital management are to ensure that the company has sufficient liquidity to meet short-term obligations and fund daily operations, while also optimizing the use of current assets to spur business growth. It aims to strike a balance between maintaining adequate cash flow and avoiding the inefficient use of resources.