Ever wonder why your favorite store always seems to have exactly what you want while the place across the street is perpetually out of stock on popular items? The answer involves a complex balancing act known as inventory management—the art of having just the right amount of stuff, at the right time, in the right place.

It’s a crucial skill for businesses that expect to retain customers and turn a profit.

What Is Inventory?

A company’s inventory comprises the finished items, component parts, and raw materials that it either sells or uses in production. As a verb, inventory refers to the act of counting or listing items. As an accounting term, inventory is a current asset and represents the value of goods a company holds for sale or use. While having enough on hand is essential, excess inventory can become a liability.

Businesses practice inventory management to ensure that they have what they need to continue to sell or build items to fulfill demand without tying up capital on goods that sit idle for an extended period or worse, expire.

Video: What Is Inventory?

Key Takeaways

- The four major categories of inventory are raw materials and components; work in progress; finished goods; and maintenance, repair, and operating supplies.

- While there are many ways to count and value inventory, the key is accurately tracking, analyzing, and managing it.

- Insights gained from inventory evaluations are necessary for success as they help companies make smarter and more cost-efficient business decisions.

- Companies that adhere to inventory management best practices tend to enjoy higher customer satisfaction and profitability.

Inventory Explained

An organization’s inventory, which is often described as the step between manufacturing and order fulfillment, is central to business operations and a primary source of revenue generation. Inventory can be classified in numerous ways, and how well it’s managed directly affects an organization’s order fulfillment capabilities.

For example, in keeping track of raw materials, safety stock, finished goods, or even packing materials, businesses are collecting crucial data that should inform future purchasing and fulfillment operations. Understanding purchasing trends and the rates at which items sell determines how often companies need to restock inventory and which items are prioritized for repurchase. Having this information on hand can improve customer relations, cash flow, and profitability while also decreasing the amount of money lost to wasted inventory, stockouts, and restocking delays.

Types of Inventory

There are four different top-level inventory types: raw materials, work-in-progress (WIP), merchandise and supplies, and finished goods. These four main categories help businesses classify and track items that are in stock or that they might need in the future. However, the main categories can be broken down even further to help companies manage their inventory more accurately and efficiently.

4 Main Types of Inventory

While each type of inventory serves a specific purpose within the production process, they all contribute to the overall value chain and the financial health of the business. All are classified as current assets on the balance sheet, meaning they will ideally be converted into cash within a year, and all generally incur costs beyond the purchase price, including for storage, management, and financing.

Raw Materials

Raw materials are unprocessed or minimally processed materials that are used in the production of finished products. A manufacturer should keep sufficient levels of raw materials in stock to maintain uninterrupted production flows. When a product is completed, its raw materials—such as the oils used in the manufacture of shampoo—are often unrecognizable from their original form. Other examples of raw materials include steel, plastics, minerals, and lumber. It’s worth noting that some raw materials, like perishable ingredients, have shorter shelf lives than others and must be managed tightly to ensure they’re used before they expire or become obsolete.

Work in Progress or Process (WIP)

When the “P” in WIP inventory refers to “process,” it represents items with a relatively short production cycle—partially finished goods that are still in the manufacturing stream. For a bicycle maker, WIP inventory might include frames that have been built but not yet been painted or assembled with the rest of the bike components. For a women’s clothing designer, it might include fabric that has been cut for dresses but not yet sewn or embellished with buttons and zippers.

When the “P” in WIP stands for “progress,” it denotes a longer-term, complex production cycle that spans more than one accounting period. Work in progress is also commonly used to describe long-term capital projects. Either way, staying on top of WIP inventory helps keep production moving along efficiently.

Finished Goods

Finished goods inventory are items that have proceeded through all stages of production and are ready for sale. These can include anything from computers and televisions to medical equipment and office supplies to boxes of cereal and winter coats. Effective management of finished goods inventory helps a business satisfy customer demand for its products, reducing the likelihood of missed sales and lost revenue. By analyzing the volume and value of finished goods in stock, companies can gain a better understanding of their financial positions, determine future budgeting needs, and reduce wasteful spending on raw materials and storage space.

Maintenance, Repair, Operations (MRO)

MRO inventory refers to the materials, equipment, and other supplies a business uses to support maintenance, repair, or operations. This category includes a wide range of products, from spare parts to fix a malfunctioning machine on the production line to supplies for cleaning the break room to basic office supplies. These items are essential to keeping the business up and running, so maintaining the right levels of MRO inventory is important. However, this can also be one of the more complex and time-consuming categories of inventory to manage because it can comprise hundreds or thousands of different items from a wide range of sources.

Additional Types of Inventory

- Components: Components are similar to raw materials in that they are used to create and finish products; however, these semi-finished goods generally remain recognizable when the product is completed. An example is a screw holding a bicycle together or a decorative clasp on a garment.

- Packing and Packaging Materials: There are three types of packing materials. Primary packing protects the product and makes it usable. Secondary packing is the packaging of the finished good and can include labels or SKU information. Tertiary packing is bulk packaging for transport.

- Safety Stock and Anticipation Stock: Safety stock is the extra inventory a company buys and stores to cover unexpected events. Safety stock has carrying costs, but it supports customer satisfaction. Similarly, anticipation stock comprises the raw materials or finished items that a business purchases based on sales and production trends. If a raw material’s price is rising or peak sales time is approaching, a business may purchase safety stock.

- Decoupling Inventory: Decoupling inventory is the term used for extra items or WIP kept at each production line station to prevent work stoppages. Whereas all companies may have safety stock, decoupling inventory is useful if parts of the line work at different speeds and applies only to companies that manufacture goods.

- Cycle Inventory: Companies order cycle inventory, sometimes referred to as working inventory, in sufficient quantities to meet typical expected demand. The key is to have enough stock to serve customers and keep production moving without incurring excess storage costs.

- Service Inventory: Service inventory is a management accounting concept that refers to how much service a business can provide in a given period. A hotel with 10 rooms, for example, has a service inventory of 70 one-night stays in each week.

- Transit Inventory: Also known as pipeline inventory, transit inventory is stock that’s moving between the manufacturer, warehouses, and distribution centers. Transit inventory may take weeks to move between facilities.

- Theoretical Inventory: Also called book inventory, theoretical inventory is the least amount of stock a company needs to complete a process without delays. Theoretical inventory is used mostly in production and the food industry. It’s measured using the actual versus theoretical formula.

- Excess Inventory: Also known as obsolete inventory, excess inventory is unsold or unused goods or raw materials that a company doesn’t expect to use or sell but must still pay to store.

Inventory refers to goods and products that can be sold. It is labeled as a current asset on a company’s balance sheet and represents an intermediary between manufacturing and order fulfillment.

Inventory Examples

Real-world examples can make inventory models easier to understand. The following use cases demonstrate how different types of inventory work in retail and manufacturing businesses.

- Raw Materials/Components: A company that makes T-shirts has on hand components that include fabric, thread, dyes, and print designs.

- Finished Goods: For our T-shirt maker, the printed shirt might be labeled and wrapped in a cellophane envelope to create a finished product, ready for sale. The cost of goods sold (COGS) of the item includes both its packaging and the raw materials and labor used to produce it.

- Work In Progress: A smartphone consists of a touchscreen, a processor, internal circuitry, a battery, and other components. Because it is produced over a period of time at dedicated workstations with specialized labor, the process can be considered a work in progress. The simpler effort of making a screen protector or case would be a work in process.

- MRO Goods: Maintenance, repair, and operating supplies for a condominium community might include copy paper, printer toner, gloves, glass cleaner, lawn mowers, and brooms for sweeping up the grounds.

- Packing Materials: At a seed company, the primary packing material is the sealed bag that contains, for example, flax seeds. Placing the flax seed bags into a box for transportation and storage is the secondary packing. Tertiary packing is the shrink wrap required to ship pallets of product cases.

- Safety Stock: A veterinarian in an isolated community might stock up on disinfectant and critical medications to meet customer demand in case the highway floods during spring thaw and delays delivery trucks.

- Anticipated/Smoothing Inventory: An event planner buys discounted spools of ribbon and tablecloths in January in anticipation of the June wedding season.

- Decoupled Inventory: In a bakery, decorators keep a store of sugar roses with which to adorn wedding cakes. Now, even when the team’s supply of frosting mix is late, the decorators can keep working. Because the flowers are part of the cake’s design, if the bakery ran out of them, it couldn’t deliver a finished cake.

- Cycle Inventory: As a restaurant uses its last 500 paper napkins, the new refill order arrives. The napkins fit easily in the dedicated storage space.

- Service Inventory: A café is open for 12 hours per day, with 10 tables at which diners spend an average of one hour eating a meal. Its service inventory, therefore, is 120 meals per day.

- Theoretical Inventory Cost: A restaurant aims to spend 30% of its budget on food but discovers the actual spend is 34%. The “theoretical inventory” is the 4% of food that was lost or wasted.

- Book Inventory: The theoretical inventory of stock in the inventory record or system, which may differ from the actual inventory when a count is performed.

- Transit Inventory: An art store orders and pays for 40 tins of a popular pencil set. The tins are en route from the supplier and, therefore, in transit.

- Excess Inventory: A shampoo company produces 50,000 special shampoo bottles that are branded for the summer Olympics, but it sells only 45,000 and the Olympics are over—no one wants to buy them at full price, so the company is forced to discount, donate, or discard them.

The Importance of Inventory Control

Inventory control involves monitoring and managing stock levels to ensure that just the right amount of product is available at just the right time. Inventory control, also known as stock control, is important because it helps companies keep production and profitability on track by preventing both excess purchasing, which ties up cash, and stockouts, which can lead to lost sales and dissatisfied customers.

Success depends on maintaining accurate inventory records and demand forecasts to inform purchasing decisions, but it’s well worth the effort. Controlling how much money is tied up in stock allows for flexibility—purchasing too much or inessential inventory limits a company’s options. Done right, inventory control wrings maximum profit from the leanest investment in stock without affecting customer satisfaction.

Inventory Best Practices

The business saying “if you can’t measure it, you can’t manage it” absolutely applies to inventory. While the first and foremost best practice is keeping track of your stock, others include:

- Carry Safety Stock: Also known as buffer stock, these products help keep companies from running out of popular or high-demand materials. If a company depletes its expected supply because the level of demand increased unexpectedly, safety stock serves as a backup and keeps production and sales moving.

- Invest in a Cloud-based Inventory Management Program: Because they’re hosted by a cloud provider and accessible from anywhere, cloud-based inventory management systems let companies know in real time where every product and SKU is located globally. This data helps an organization be more responsive, up-to-date, and flexible.

- Start a Cycle Count Program: Cycle counting benefits extend well past the warehouse by keeping stock reconciled and customers happy while also saving businesses time and money.

- Use Batch/Lot Tracking: Record information associated with each batch or lot of a product. While some businesses log precise details, such as expiration dates, companies that do not deal in perishable goods can use straightforward batch/lot tracking to understand their products’ landing costs or shelf lives.

Inventory management is critical in strengthening companies’ supply chains because it helps to stabilize the dynamics between customer demand, storage space, and cash restraints.

What Is Inventory Turnover?

Inventory turnover is the number of times a company sells or uses an item in a specific timeframe. This metric can reveal whether a company keeps too much or too little inventory on hand. To determine inventory turnover, use the following equations:

Average inventory = (Beginning Inventory + Ending Inventory) / 2

Inventory turnover = Sales + Average Inventory

The Inventory Turnover Ratio

The inventory turnover ratio is a financial metric that indicates how efficiently a company uses or sells its inventory over a given period. It’s calculated by dividing COGS by the average inventory value during that period:

Inventory turnover ratio = COGS / Average Inventory

A low inventory turnover ratio could indicate lower sales or too much inventory. It might also suggest problems with a company’s marketing strategy. A higher inventory ratio could be a sign of stronger sales or could suggest inadequate inventory stocking. Thus, it’s important to have some additional context in order to accurately interpret the inventory ratio. Looking at an inventory turnover ratio in relation to historical trends or against competitive or industry benchmarks can help assess a company’s operational and inventory management efficiency and effectiveness.

What Is Inventory Management?

Inventory management is the business process that ensures a company has the right amount of the right items in the right place at the right time. It includes oversight of everything from ordering and storing inventory to using or ultimately selling it.

For many businesses, such as manufacturers and retailers, inventory is one of their most valuable assets, enabling them to meet customer demand and make money. But inventory can also be a drain on profitability if not carefully managed. Holding on to too much inventory carries significant costs, and there is also the risk of spoilage, theft, and damage to factor into the equation. The goal of effective inventory management is to achieve a just-right level to avoid overstocking, shortages, or stockouts, all of which can be extremely costly to a business.

What Is Inventory Analysis?

Inventory analysis is the study of how product demand changes over time. It helps businesses stock the right amount of goods and project how much customers will want in the future.

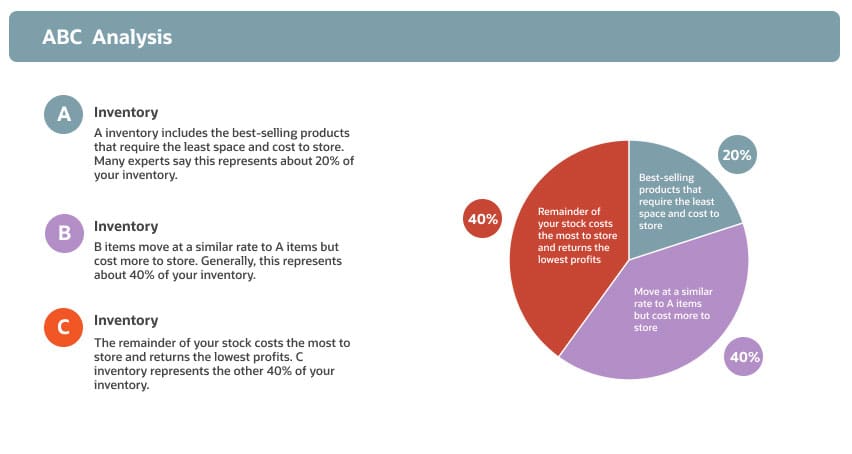

A well-known method for performing inventory analysis is ABC analysis. To perform an ABC analysis, group goods into three categories:

- A inventory: A inventory includes the best-selling products that require the least space and cost to store. Many experts say this represents about 20% of your inventory.

- B inventory: B items move at a similar rate to A items but cost more to store. Generally, this represents about 40% of your inventory.

- C inventory: The remainder of your stock costs the most to store and returns the lowest profits. C inventory represents the remaining 40% of your inventory.

ABC analysis leverages the Pareto, or 80/20, principle and should reveal the 20% of your inventory that garners 80% of your profits. A company will want to focus on these items to increase sales and net profit margins. Inventory analysis may influence the choice of inventory control methods, whether just-in-time or just-in-case.

Benefits of Inventory Analysis

Inventory analysis raises profits by lowering costs and supporting turnover. It also:

- Improves Cash Flow: Inventory analysis helps you identify and reorder items you sell often, so you don’t spend money on inventory that moves slowly.

- Reduces Stockouts: When you understand which inventory moves the fastest, you can better anticipate demand and prevent stockouts.

- Increases Customer Satisfaction: Analyzing inventory offers insights into when and how your customers purchase goods.

- Reduces Wasted Inventory: Understanding what, when, and how much people buy minimizes the need to store obsolete products. Analysis can also help companies develop a strategy to move perishable items before they expire.

- Reduces Project Delays: Learning about supplier lead times helps you understand when to reorder and how to avoid late shipments.

- Improves Pricing From Suppliers and Vendors: Inventory analysis can lead you to order high volumes of products regularly rather than small volumes on a less reliable schedule. This regularity can put you in a stronger position to negotiate discounts with suppliers.

- Expands Your Understanding of the Business: Reviewing inventory provides insights into your stock, customers, and business.

NetSuite Software for Managing All Your Inventory Needs

Properly managing inventory can make or break a business. Having insight into your stock at any given moment is critical to success, and decision-makers know they need the right tools to manage inventory effectively. NetSuite offers a suite of tools for tracking inventory in multiple locations, determining reorder points, and managing safety stock and cycle counts. Find the right balance between demand and supply across your entire organization with industry-leading demand planning and distribution requirements planning features.

NetSuite provides cloud inventory management solutions that are the perfect fit for companies from startups to the Fortune 100. Learn more about how you can use NetSuite to help plan and manage inventory, reduce handling costs, and increase cash flow.

Inventory FAQs

What is manufacturing inventory?

In manufacturing, inventory consists of in-stock items, raw materials, and the components used to make goods. Manufacturers closely track inventory levels to ensure there isn’t a shortage that could stop work.

Accounting divides manufacturing stock into raw materials, WIP, and finished goods because each type of inventory bears a different cost. Raw materials typically cost less per unit than do finished items.

What does inventory mean in the service industry?

In the service industry, inventory refers to the resources that a business uses to serve its customers. Instead of physical goods, as in a product-based business, that list might include staff time, equipment, and intangible assets like intellectual property or customer relationships. For example, in a law firm, the billable hours of attorneys and paralegals represents inventory, while items such as computers and paper on which to print legal documents is the firm’s maintenance, repair, and operating supplies, or MRO.

What is an inventory process?

An inventory process tracks inventory as companies receive, store, manage, and withdraw or consume items as work in progress. Essentially, the inventory process is the lifecycle of goods and raw materials.

What are the four different inventory types?

There are four main types of inventory: raw materials/components; work in progress or process, or WIP; finished goods; and maintenance, repair, and operating supplies, or MRO. However, some people recognize only three types of inventory, leaving out MRO. Understanding the different types of inventory is essential for making sound financial and production planning choices.

How is inventory controlled?

Inventory control—or stock control—is making sure that your business has the right supply of goods to meet customer demand. This usually requires inventory management and supply chain management (SCM) software that brings in data from purchases, shipping, warehousing, reorders, receiving, storage, loss prevention, and even customer satisfaction surveys.

What is an inventory record?

An inventory record, or stock record, contains data about the items a company has in stock, such as the amount of inventory on hand, what’s been sold and reordered, what’s on order, the product’s value, and where it’s stored. It’s important to keep accurate inventory records to assist with inventory control and keep accurate balance sheets.

What is demand forecasting?

Demand forecasting is the practice of predicting customer demand by looking at past buying trends, such as promotions and seasonality. Accurately predicting demand provides a better understanding of how much inventory you’ll need and reduces the need to store surplus stock.

Inventory forecasting relies on data to inform decisions, applying information and logic to guarantee you’ve got enough product on hand to meet demand while not tying up cash with unnecessary inventory. There are a number of advanced simulations used, but it typically comes in the form of trend forecasting, graphical forecasting, qualitative forecasting, or quantitative forecasting.

What is average inventory cost?

The average cost of inventory is a method for calculating the per-unit cost of goods sold. To calculate the average cost, get the sum of the cost of all stock for sale, and divide it by the number of items sold.

This method is also called weighted average cost and is a valuable way to determine the value of your current inventory. It works best for brands that have high volumes of inventory and SKUs that are similar in cost. One of its benefits over other methods is that it makes it easier to track and consistently calculate inventory value by using a blended average.

What is inventory count?

An inventory count is the physical act of counting and checking the condition of items in storage or a warehouse. An inventory count also checks the condition of items. For accounting purposes, inventory counts help assess assets and debts.

Inventory counts help you understand which stock is moving well and inventory managers often use this information to forecast stock needs and manage budgets.