“Capital” is a popular term in the world of finance. The word on its own usually refers to a company’s available funds, such as its retained earnings or available credit or owner’s capital. When a company spends or invests its capital on a long-term asset, like a piece of machinery, it’s called “capital spending,” and the machinery is a “capital asset.” Further, the process of evaluating how best to invest a company’s capital—by making “capital expenditures”—is called “capital budgeting.” All of these “capital” terms share two common dogmas: that capital is finite and capital expenditures should be prioritized to get the most bang for the buck. The world of finance provides frameworks and tools to help business leaders objectively determine which capital projects to pursue or prioritize. This article explores different methods of capital budgeting, best practices, and steps in the process—because capital spending is too important to rely on gut instinct.

What Is Capital Budgeting?

Capital budgeting is the process of analyzing, evaluating, and prioritizing investment in large-scale projects that typically require significant amounts of funds, such as for the purchase of a new facility, fixed assets, or real estate. Capital budgeting provides an objective means of determining the best way to use capital to increase the value of a business and is useful to companies of all sizes and industries.

Consider these scenarios that call for capital budgeting:

- Should a large automobile manufacturer build a new factory to make electric vehicles or buy a company that already specializes in building them?

- Should a midsize retailer invest in automated inventory control software?

- Should a small restaurant owner buy a second pizza oven?

These examples challenge decision-makers to determine whether their spending will bring enough future benefits to their businesses. Business managers often have to weigh multiple projects that are competing for the same investment funds, which means the decision needs to be based on some kind of ranking rather than a simple yes or no. Capital budgeting is a structured way to approach these questions—incorporating the expected cash outlays and inflows—and to help manage the financial risks involved in these capital-intensive and strategically important projects.

Key Takeaways

- Capital budgeting is the process of determining whether a large-scale project is worth the investment and will increase a company’s value.

- Using a formal process for capital budgeting increases the likelihood of better outcomes.

- Some capital budgeting methods are somewhat subjective, while others are based on financial formulas.

- High-quality data increases the usefulness of capital budgeting.

Capital Budgeting Explained

Capital budgeting is a type of financial management that focuses on the cash flow implications of making an investment, rather than resulting profits (to avoid complicating calculations with accounting conventions, such as depreciation). It involves estimating the amount and timing of cash outflow—money that leaves the business to pay for a purchase or investment, such as new equipment—and cash inflow, or new sources of cash that come into the company, such as increased sales revenue made possible by the increased output from the new equipment. In some cases, a reduction in cash outflows can be considered a cash inflow for capital budgeting purposes—for example, when a new piece of equipment reduces the cost of producing a product. Different capital projects can be evaluated by comparing their amounts of cash outflow and cash inflow.

Two important concepts that underlie many capital budgeting methods are opportunity cost and the time value of money. Both apply due to the long-term nature of most capital projects.

Opportunity costs can be described as the value of the road not taken. Assuming that capital funds are not infinite, the opportunity cost represents benefits that are forgone by choosing one investment over the next best one. A simple example is choosing to keep cash sitting in a cookie jar, rather than in an interest-bearing bank account. The forgone interest income that could be earned is the opportunity cost of keeping cash in the cookie jar. Opportunity cost is especially relevant in capital budgeting when evaluating one project against another and is used to determine a “hurdle,” or minimum target return, that a capital project must meet.

The time value of money is a financial concept that considers the potential rate of return on an investment and the reduction in purchasing power over time caused by inflation. Its essential precept is that a dollar today is more valuable than that dollar will be at some point in the future. In other words, the farther into the future, the less valuable the dollar. The time value of money is based on the idea that if a person had a dollar today, they could invest and grow it based on some investment rate, so they’d have more than a dollar at the end of the investment term. If instead they opted to get that dollar in the future, they’d forgo that investment growth. Capital budgeting also includes a focus on the timing of the cash flows to reflect the time value of money.

Why Do Businesses Use Capital Budgeting?

Capital budgeting helps businesses evaluate and compare opportunities and then decide where to invest their limited capital resources for the best long-term benefit. Through smart capital investment decisions, companies can improve efficiency, expand capacity, introduce innovative capabilities, and even gain a competitive edge in their industry, leading to higher company worth and increasing shareholder value. More than just a financial exercise, capital budgeting plays a central role in strategic planning by aligning investments with organizational goals, navigating uncertainty, and staying relevant in a dynamic market. The following four key aspects illustrate why capital budgeting is indispensable for businesses committed to making sound, future-focused decisions:

- Maximize return on investment: Capital budgeting helps businesses assess and prioritize long-term projects by analyzing their potential returns relative to the investment required. This process supports smarter capital allocation by focusing on long-term value creation and aligning financial decisions with strategic goals.

- Strengthen resource management: This broader view considers both financial and nonfinancial resources, including human capital, production capacity, and technology, and balances them across the organization to prioritize promising opportunities and avoid overcommitment to less valuable projects. This approach boosts operational efficiency and overall financial performance, while maintaining essential liquidity and working capital.

- Assess cash flow: Capital budgeting focuses on the timing and amount of cash flows associated with investment projects, providing a clear picture of the company’s future liquidity. This influences cash flow forecasts, which help companies meet current obligations while also pursuing long-term growth opportunities.

- Evaluate risks: Capital budgeting techniques incorporate risk assessment into the investment decision-making process. Analyzing potential risks associated with different projects leads to smarter decisions and may assist a company with developing strategies that mitigate or avoid investments that could harm its financial stability.

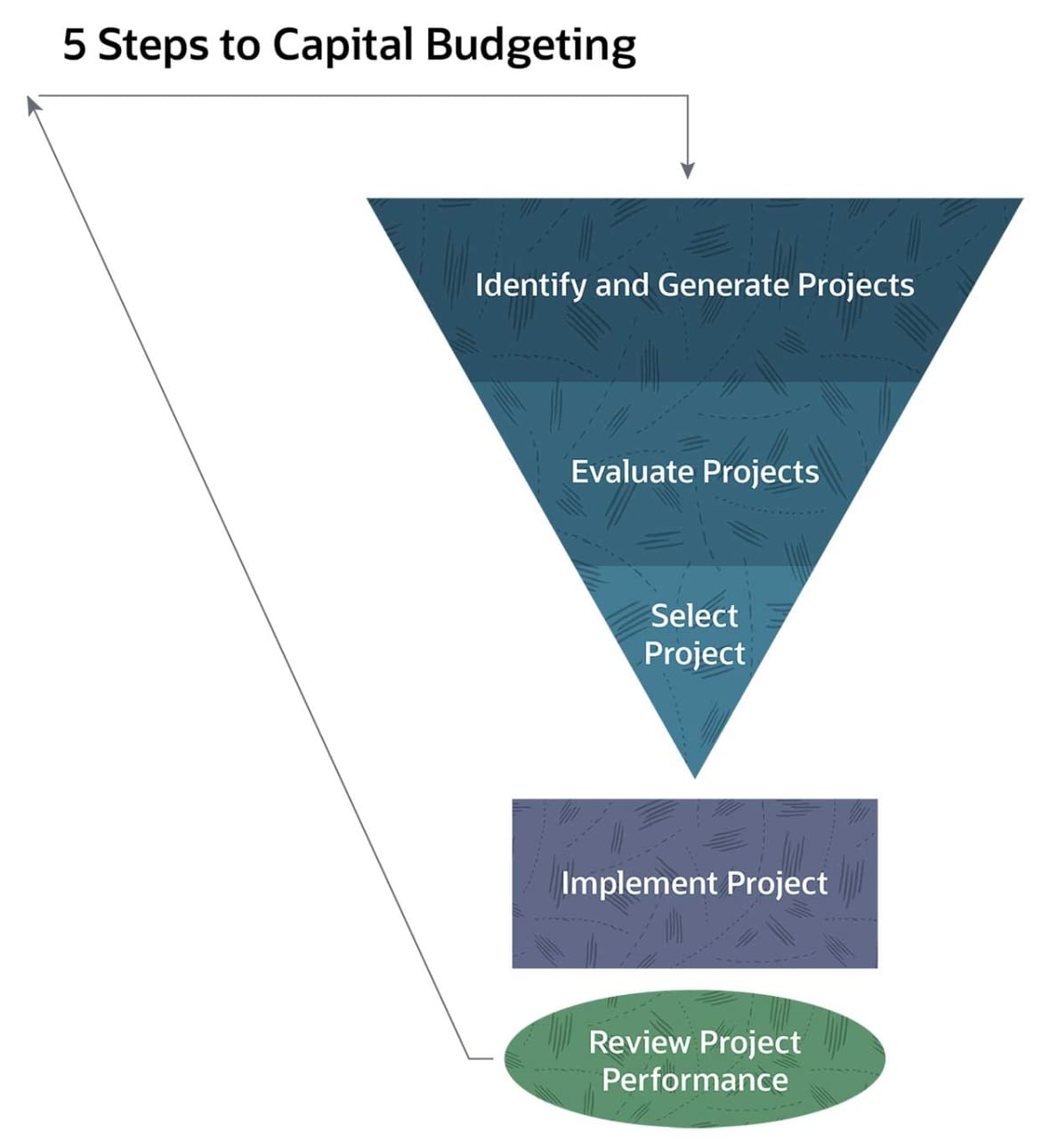

Capital Budgeting Steps

How a company manages the capital budgeting process depends on its organizational structure. Some large organizations have a capital budgeting committee who oversee all capital projects. In small and midsize businesses, capital budgeting decisions are made by the owner or a small group of executives, often supported by analysis from their accountants. In all cases, it’s important to keep the company’s strategic goals in mind before jumping into the first of five steps that govern the process.

- Identifying potential projects: Gather ideas and proposals, which can come from anywhere in the organization. It’s helpful to have a procedure for submission, which may include using templates, but always require cash flow, cost, and benefit estimates. It’s common for a growing business to have many proposals competing for available funds.

- Evaluating the projects: This step focuses on establishing the feasibility of the various proposals, beginning with screening to confirm that they contain all the right information and that the sponsor has done their due diligence. It’s common to require proposals to be vetted and reviewed by different areas of the company, obtaining endorsements from accounting, sales, or operations managers prior to submission. Another part of project evaluation involves establishing the criteria to be used to assess the proposals, such as tolerable risk, hurdle rates, and spending thresholds. Criteria are at management’s discretion, with the goal of increasing the company’s value.

- Selecting a project: Proposals are analyzed, and then those that meet the evaluation criteria and are considered a good business move are given the green light. The timing and priority of competing projects often play a part in selection, especially in situations where proposals exceed the company’s available funding or bandwidth for execution.

- Implementing a project: Once a proposal is approved, an implementation plan is developed. This plan describes key factors for accomplishing the project, such as how it will be funded and methods of tracking cash flows. It also sets a project timeline, including various milestones and a target end date. Additionally, the implementation plan identifies key personnel involved in the project, authority levels, and a process for escalation of exceptions, such as delays or budget overages.

- Review project performance: The final step in the capital budgeting process is to review the actual results of the project compared with the approved proposal. It’s a good idea to do this at predetermined implementation milestones as well as at the end of the project. Learning from one project can help inform future capital projects.

Ranking Projects With Capital Budgeting

Keeping in mind the goal of maximizing business value, it’s important to invest a business’s capital wisely. This requires business leaders to prioritize capital projects because it’s unlikely that any organization can, or should, undertake every proposal. Ranking projects is one way to objectively prioritize which projects to approve, defer, or reject. Ranking narrows down viable alternatives and is part of step 3 in the five-step capital budgeting process described in the previous section. There are several methods a business can use to value capital projects and develop a ranking, as outlined in the next section.

Capital Budgeting Methods

Businesses can choose to use one or more types of capital budgeting methods, described below, to help value and evaluate capital projects. These methods serve to eliminate projects that fall short of a company’s minimum performance thresholds. They are also helpful in comparing competing projects and developing rankings.

Payback Analysis

Payback analysis is a method of capital budgeting that focuses on how quickly a company can recoup its initial investment in a capital project. It is one of the simpler methods which makes it popular. The payback approach schedules out all future cash inflows from a project in chronological order. These inflows are accumulated until the point at which they equal the initial cash outflow, or capital investment. This future date is used to evaluate the project, with shorter paybacks being preferable because they are considered less risky. Companies may set a blanket, maximum acceptable payback period for their capital projects, such as “not to exceed 15 years,” as a way to rule out potential projects. This method is particularly useful for companies concerned about liquidity, as it shows how quickly the investment can be recovered. However, its simplicity is also its most significant limitation, since it ignores the time value of money, the size of the cash flows, and any cash flows, in or out, beyond the payback point.

Discounted Cash Flow Analysis

Discounted cash flow (DCF) analysis is a more sophisticated method for capital budgeting because it recognizes the time value of money. DCF estimates the present value of an investment, which can be compared with other investment opportunities; a higher value is generally preferred, all other factors being equal. DCF involves several key steps:

- First, it requires forecasting all future cash flows, both inflows and outflows, over the lifecycle of the project.

- Next, an appropriate discount rate is determined, often based on the company’s weighted average cost of capital or the specific risk profile of the project.

- This rate is then used to discount the projected future cash flows back to their present value.

- The sum of these discounted cash flows is the project’s total value.

The DCF method is a good way for companies to compare projects of different sizes, durations, and risk profiles on a level playing field. However, DCF’s reliability depends heavily on the accuracy of cash flow forecasts and the appropriateness of the discount rate used.

Throughput Analysis

Throughput analysis is a capital budgeting method favored by lean and agile manufacturers because it evaluates investments based on their ability to increase systemwide throughput—meaning the rate at which the entire process generates money through sales. Unlike traditional methods that focus on reducing costs or increasing profitability at individual steps, throughput analysis prioritizes capital projects that relieve bottlenecks and improve flow across the whole production system. This shift from task-level optimization to system-level performance helps keep investment selection fixed on boosting overall output and value, rather than just isolated functions, like assembly or packaging. While this approach supports more strategic, holistic decision-making, it requires a thorough understanding of operational interdependencies and can be more complex to implement than standard financial metrics-based methods.

Equivalent Annuity Method

The equivalent annuity method is a way to evaluate the net present value (NPV) of capital projects that are mutually exclusive and have different project lengths. It does this by creating an annual average to smooth out the individual discounted cash flows. The first step in this method is to calculate the NPVs of each cash flow over the life of the projects. Projects with positive, higher equivalent annual annuity are preferred. The equivalent annuity method is especially helpful when evaluating different proposed capital projects with varying life terms. However, a disadvantage is that the underlying calculations to derive the average assume that projects can be repeated into perpetuity, which is unlikely to be the case.

Constraint Analysis

Constraint analysis is a criterion used in capital budgeting to help select capital projects based on operational or market limitations. Unlike the quantitative methods previously described, this approach looks at company processes, such as product manufacturing, and determines which stages of the process make the most sense for investment. A key concept in constraint analysis is identifying bottlenecks—pinch points in the process that would make downstream investments of no use. For example, if a dine-in-only restaurant had a finite number of tables, it might not make sense to invest in more kitchen equipment, since sales are constrained by the number of diners. A constraint analysis might indicate that priority should be given to an investment in expanding the dining area instead. The advantage of this approach is that it helps a business avoid undertaking projects that may not increase profitability. However, identifying constraints can be challenging and somewhat subjective.

Cost Avoidance Analysis

Cost avoidance analysis draws on the concept of opportunity cost to approach capital-budgeting decisions. Using this method, a business evaluates capital projects using an estimate of costs that can be eliminated in the future by undertaking the project. For example, investing in automated accounting software could negate a company’s need to hire additional bookkeepers in the future. Capital projects that avoid more costs than others are prioritized first. Quantifying capital projects using cost-avoidance analysis is challenging since it is a theoretical exercise—if the correct capital decision is made, the costs never materialize and never hit a financial statement.

Real Options Analysis

Many times, business leaders must make capital budgeting decisions with imperfect information due to uncertainties about future conditions, especially since capital projects tend to be long-term in nature. Consider the cyclical disruptions in technology that present challenges or opportunities for capital projects in that industry. The real options analysis attempts to determine a value for a capital project’s flexibility. It does this as an extension of NPV, using probability estimates and assuming changes in the discounted cash flows for project adjustments, such as asset choice, investment timing, growth options and abandonment. Consider a manufacturing capital project that is altered halfway through the project life because different, cheaper raw materials become available. The real options method is helpful because it reflects dynamic changes a project might offer over its life, beyond a simple, static “go/no-go” approach. However, it can become extraordinarily complex depending on the number of uncertainties considered.

Capital Budgeting Metrics

While the methods discussed above describe ways to analyze capital budgeting decisions, the metrics derived from these methods offer empirical measures for evaluating and comparing projects. These metrics distill complex financial analyses into more easily interpretable data points—ranging from simple time-based measures to more advanced financial calculations—that give decision-makers quantifiable information to support capital allocation choices. Each metric has strengths and limitations. In practice, decision-makers use them in conjunction with one another and alongside qualitative factors for comprehensive capital budget decision-making.

Payback Period

This metric is the point in time when the project has “paid for itself.” It does not place a value on a project; instead, it is the specific amount of time to pay back the initial investment, usually expressed in months or years. Shorter payback periods are usually interpreted as being more favorable because they return liquidity back to the company faster, which means it can be redeployed into new opportunities more quickly. Additionally, shorter periods reduce exposure to future risks, such as market volatility or obsolescence. Also, it is often appealing to stakeholders focused on short- to medium-term performance.

Discounted Payback Period

This is an improved version of the payback period because it also reflects the time value of money, which always decreases as the years pass. To account for this, cash flows in future periods are discounted so as to revalue them in present value terms. As a result, the discounted cash flows are less than the non-discounted cash flows, which causes the discounted payback period to be longer than the non-discounted payback period. This difference between the discounted method and the non-discounted period increases when the payback period is longer or the discount rate is higher. The discount rate can be a company’s cost of capital or its required internal rate of return. The advantage of this method is that it more accurately calculates the payback period, reflecting the time value of money. However, the discounted payback period maintains the disadvantages of ignoring periods beyond payback and terminal values.

Net Present Value Analysis

Net present value (NPV) is one of the key metrics derived from the DCF method. The NPV of a project represents the excess of discounted cash inflows beyond discounted cash outflows. NPV is applied to the entire lifecycle of a project, including any terminal or residual values. It is a monetary value that can be positive or negative; a positive value indicates that the project is expected to add to a firm’s value, while a negative value reduces it. Projects with a larger, positive NPV are preferred over those with smaller or negative NPVs, assuming the projects have similar levels of risk. One of the main challenges of using NPV is the sensitivity to the discount rate used in the DCF calculations. For example, NPV calculations change significantly depending on whether the discount rate is based on a company’s cost of capital (its all-in borrowing rate), its internal cost of capital (akin to an opportunity cost), a specific rate of return expected by external investors, or an internally generated threshold rate of return.

Internal Rate of Return

The internal rate of return (IRR) is a capital budgeting metric that represents the discount rate at which a capital project’s NPV is zero. More simply, IRR is an expected percentage of return on a project, rather than a dollar value. The percentage is the embedded rate that would cause the total of all the discounted cash inflows and outflows to be even. Capital projects that have a higher IRR are typically selected first, all else being equal. Additionally, a company might compare this metric to its cost of capital or to an internal threshold in order to determine whether to take on a capital project. IRR is a helpful way to compare projects against each other and against a required hurdle rate. However, a primary disadvantage of IRR is that it doesn’t reflect a project’s size or impact on a business’s overall value.

Modified Internal Rate of Return

The modified internal rate of return (MIRR) is an extension of IRR. It also calculates a yield percentage on a project when the NPV is zero but in a more complex and accurate way. The metric reflects DCF that uses different rates for discounting cash inflows than it uses for cash outflows when calculating the NPV. Cash inflows are discounted using a company’s reinvestment rate, and the cash outflows, like the initial capital investment, are calculated using the company’s financing rate. Using a reinvestment rate for cash inflows tends to be more realistic than using a single rate for both financing and reinvestment, as with the NPV and IRR metrics. It also gives a better comparison for projects of different sizes. However, the use of multiple discount rates also makes calculating the MIRR more difficult.

Profitability Index

The profitability index is a metric that calculates the cash return per dollar invested in a capital project. This index is calculated by dividing the NPV of all the cash inflows by the nominal value of the initial investment (unless that investment is made over a period of time, where the denominator would be the NPV of the outflows). Projects with an index less than 1 are typically rejected, since, by definition, the sum of the projected cash inflows is less than the project’s initial investment when the time value of money is factored in. Conversely, projects with an index greater than 1 are ranked and prioritized. The profitability index is helpful in determining which capital projects make sense to greenlight, especially when analyzing several projects drawing on a fixed amount of investment capital. However, the profitability index is less useful for projects with a high amount of sunk costs—money already spent and irretrievable.

Which Method Should Your Business Use?

The capital budgeting methods and metrics discussed above all have advantages and disadvantages. Some are computational while others are more qualitative and process-oriented. Determining which approach to use is really a matter of the specific situation, the sophistication of the person or team evaluating a project, and the company’s objective. In addition, the size of the capital spending relative to the available funds might make a more sophisticated analysis appropriate. In other cases, simpler methods can be beneficial when time is of the essence. In practice, a company might use several of the techniques.

Capital Budgeting Best Practices

Capital spending deals with big-ticket items and projects with long lives, so it’s important to fine-tune the capital budgeting process as much as possible. Some best practices to consider include:

- Focus on cash flows: Use cash flows, rather than net income, for modeling capital projects. Incorporate cash flows from all sources, including changes in working capital, such as increases and reductions in accounts receivable and accounts payable.

- Be conservative with estimates: This means tempering enthusiasm for the benefits of a project when estimating potential cash inflows and taking more of a worst-case viewpoint when estimating cash outflows.

- Project timing carefully: The time value of money is an important concept for capital budgeting, so it follows that projecting the timing of cash flow as precisely as possible is a priority.

- Ignore certain costs: Exclude certain costs, such as tax, amortization, depreciation, and financing costs, to keep capital budgeting calculations purely focused on the impact of the capital project.

- Establish a procedural framework: Set up clear accountability and responsibility for capital projects. This includes procedures to track costs, schedules, and quality in a controlled environment.

- Incorporate review: Knowledge gained from past proposals and capital budgeting cycles can improve future projects. It’s helpful to conduct a formal review and document findings at various stages of a project as well as at its end.

Capital Budgeting Limitations

While capital budgeting is a necessary process to help a company estimate and evaluate its options for capital spending, it is inherently limited by the compound effect of estimates. Predicting any one of these variables is a challenge; when they are put together, the effect can lead to misleading information and suboptimal decision-making. Capital budget shortcomings can occur due to:

- Incorrect cash flow estimates: Over- or underestimating the cash flow into or out of the company can cause capital projects to be incorrectly accepted or rejected.

- Inaccurate timing estimates: The timing of cash flow is almost as important as the amount of the cash flow. The longer a project’s term, the more difficult these estimates can be, which can have a significant impact on NPV calculations.

- Determining the right rates: Choosing the right discount rates for capital budgeting is not always as easy as it sounds. It may take a bit of calculating to determine a company’s true cost of capital and financing rate. Even setting a hurdle rate—the least acceptable rate of return on an investment—may not be so simple. Using an incorrect discount rate can upend many of the common capital budget methods.

Capital Budgeting Considerations

When evaluating capital investment opportunities, smart financial analysis goes beyond the methods and metrics of cash flow projections, taking into account a wide range of factors that can significantly impact a capital project’s success and long-term value. A more holistic view encompasses the larger business environment to add additional context to a project’s potential risks and rewards. The following key areas can significantly influence project outcome:

- Macroeconomic trends: Broad economic factors, such as gross domestic product (GDP) growth, inflation rates, and interest rates, might impact the project’s cash flows over its lifetime, due to factors such as consumer demand, cost estimates, and cost of capital.

- Regulations and policy: Be aware of current and potential future regulatory changes that could affect the project’s costs, revenues, or legal feasibility.

- Competitor behavior: Assess the direct and adjacent competitive landscape and how competitors’ actions or potential new market entries might influence the project’s expected returns and strategic value to the company.

- Accounting methods: Understand how different accounting treatments, such as depreciation methods, might affect reported financial performance, even if they don’t impact cash flows directly.

- Tax implications: Analyze the tax consequences of the project, including potential tax deductions from depreciation, tax credits, or changes in the company’s effective tax rate from new jurisdictions or different tax brackets.

- Capital availability: Evaluate the company’s ability to raise the necessary capital for the project from either internal funding or external financing. Limited access to capital can constrain project selection, affect the cost of financing, and impact overall project viability and returns.

- Technology: Think through the likelihood of any advances in technology that could alter market dynamics or create new opportunities or threats and, in turn, affect the project’s efficiency, competitiveness, or even relevance over its expected lifespan.

NetSuite Has All Your Budgeting and Financial Planning Needs in One Place

The capital budgeting process helps business leaders make better informed decisions about how to invest their company’s capital. The quality of the data used in the process is important for producing the most accurate analyses. NetSuite Planning and Budgeting can help. The automated, collaborative tool offers complex modeling features that can help elevate the most investment-worthy capital budgeting proposals at the front end of the process. In addition, the software can help track actual project cash inflows and outflows against the estimates as the project is implemented. It also reduces budgeting cycling time and improves the accuracy of forecasts.

Capital budgeting is the process of evaluating long-term investments. Taking a formal approach increases the likelihood of selecting projects that are more likely to increase business value. A variety of methods and metrics exist to help quantify the impact of capital projects and compare them, most using the financial concepts of opportunity cost and the time value of money. Choosing the best options and understanding their limitations can help make sure that the right information is analyzed. Planning and budgeting software can make all five stages of the capital budgeting process easier and more accurate.

Capital Budgeting FAQs

What is the primary purpose of capital budgeting?

Capital budgeting is the process of analyzing, evaluating, and prioritizing investment in capital-intensive projects. It’s an objective way to determine the best use of funds to increase the value of a business.

What is an example of a capital budgeting decision?

An example of a capital budgeting decision is a small restaurant owner contemplating buying a second pizza oven. The owner must decide whether this investment is the best use of capital or if the opportunity cost of spending that money is too high. She might determine that the internal rate of return on the purchase is lower than the interest rate she could earn by simply leaving her cash in an interest-bearing savings account, representing the hurdle rate. She could also use the payback period to determine how long it would take to sell enough pizzas to make back the initial outlay of cash for the new pizza oven. But if hers is a dine-in-only restaurant with a finite number of tables, constraint analysis might indicate that it doesn’t make sense to invest in more kitchen equipment, since sales are constrained by the number of diners.

What is the difference between capital budgeting and working capital management?

Working capital is a measure of liquidity, being the difference between a company’s current assets and current liabilities. Working capital management is a process to optimize a company’s current assets and liabilities to meet short-term goals. Capital budgeting is the process of evaluating the best way to invest money in long-term projects that increase the value of a business, such as purchasing machinery, building facilities, or investing in new product development.

What is meant by capital budget?

When a company spends or invests its capital on a long-term asset, like a piece of machinery, it’s called capital spending, and the machinery is called a capital asset. The process of evaluating how best to invest a company’s capital—by making capital expenditures—is called capital budgeting.

What is capital budgeting and an example?

Capital budgeting is the process of evaluating long-term investments. Examples include the addition or replacement of a fixed asset, like machinery, or a large-scale project, such as buying real estate or another company.

What are the 3 methods of capital budgeting?

Several capital budgeting methods are used to help value capital projects. The valuations serve to screen out projects that fall short of a company’s minimum performance thresholds. They are also helpful in comparing competing projects and developing rankings. Three common methods of capital budgeting are payback analysis, net present value analysis, and constraint analysis.

What is the capital budgeting process?

A capital budgeting process typically includes the following five steps:

- Identifying and generating projects

- Evaluating the projects

- Selecting a project

- Implementing a project

- Reviewing project performance