In short:

- The pandemic reshuffled the deck on company financials.

- It’s always good practice to know what your business is worth. It’s critical when you’re seeking capital.

- Investors are actively looking for opportunities. Here are sources and advice to improve your chances of success.

Whether you’re approaching bankers or private equity firms, there is money to be had. But how do 2020’s unprecedented conditions affect both the process by which funders determine a company’s value and that value itself?

There are no universal truisms when it comes to valuation now — except to expect past governance and future revenue projections to be scrutinized more closely than in less-volatile times. If you go to the market seeking capital, a well-documented valuation and COVID-19-reflective business plan are absolutely required, of course. The methods of valuation, management’s ability to meet previous projections and the validity of forward-looking revenue scenarios will all be under a microscope.

Your vertical and, to a lesser degree, physical location will matter, but not as much as the narrative around your company’s ability to adapt to COVID-19 and create a sustainable business going forward.

There are five main paths to raising capital:

- Venture funding for young companies with strong growth potential.

- Private equity for those willing to give up a chunk of the company in exchange for cash now.

- SBA-backed loans. These are somewhat easier to get today than they were a year ago, but loan amounts are typically small.

- Bank loans without government backing. As always, strongly dependent on good collateral and stable, growing revenue. Also, in a small business, likely dependent on your personal credit. Your house may be part of the collateral.

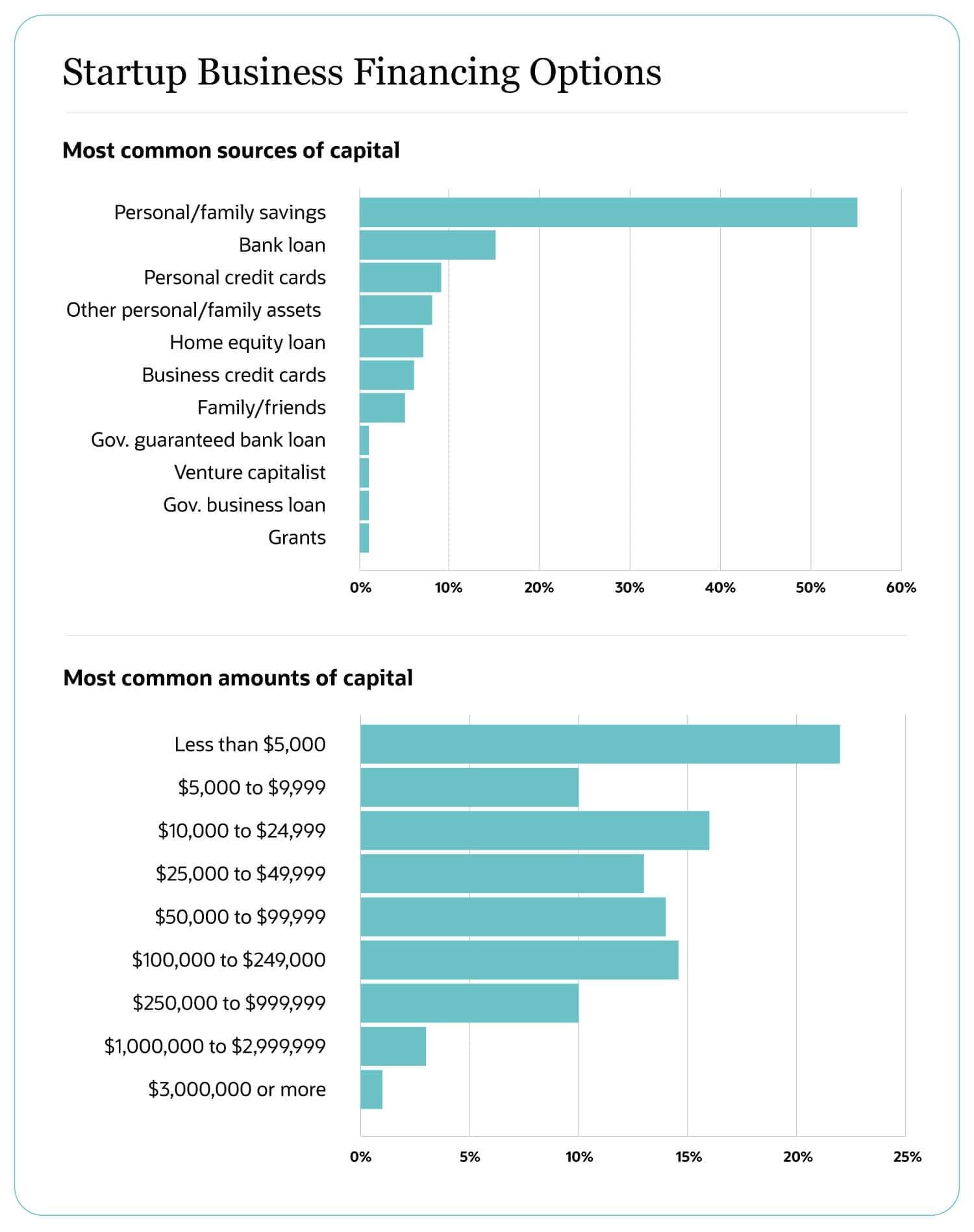

- Friends and family and personal savings — the most popular options.

The chart below shows how U.S. small and startup businesses are typically funded, based on data from the Bureau of Labor Statistics. This is generally early-stage funding, the data is pre-pandemic and software/technology companies are more likely to receive cash from VCs. Still, it’s an instructive reminder for most businesses: Beyond the government programs set up for relief from COVID-19, you’re your own best source of help.

Another source of business advancement that still makes sense is a merger or acquisition.

Doing Diligence Differently

“Misery acquaints a man with strange bedfellows,” wrote Shakespeare in The Tempest. Tough times might lead you to team up with those with whom you previously had little in common. Be creative — a strategic merger could be a way to lift both boats. You’ve got a new consumer product, you know another firm with a strong e-commerce presence, make some music together.

In April, M&A pretty much came to a halt as the vast majority of revenue assumptions and customer funnels changed drastically, and quickly, to unknowable. Even in June, Harvard Business Review surveyed a small number of executives in companies of various sizes and found that 51% of deals were paused, with an additional 14% stopped altogether. Of the 24% late-stage deals proceeding, half were looking to an accelerated process.

For large companies, HBR sees acquisitions happening in “opportunist hotspots,” and offers Verizon’s acquisition of videoconferencing vendor BlueJeans as an example. The synergy there is obvious, and the deal closed in just a few weeks.

For those not fortunate enough to be Zoom-wannabes or in a similarly hot market, HBR’s survey finds executives who think their companies are attractive acquisition targets waiting until “the perceived valuation gap” rights itself. That effectively means that PE firms with deep pockets are bargain hunting. But that doesn’t mean that mergers should be off the table for strategic pairings.

Using any of these sources will require both a good forward-looking plan and a solid idea of your company’s worth. So what will affect your company’s value and how creditors might view you?

5 Considerations for Capital Seekers

1. Different methods of valuation can yield very different results now. “We recommend always using more than one method to determine company value,” says Dave Bookbinder, senior director at advisory firm Corporate Finance Group Inc. “Currently, a discounted cash flow model could give you a very different answer than, say, using the multiples of publicly traded guideline companies within your vertical.”

There are many possible reasons for that. Bookbinder points out that guideline companies may not have reported recent quarterly revenue and profits, which could keep their valuations higher than they should be. Another factor at play now is a “big company” multiple. In retail, huge players with strong ecommerce capabilities are doing well, mostly at the expense of brick-and mortar shops.

Looking at the major market indices from July 2019 to July 2020, the Dow is flat, the S&P 500 is up 9.5% and the NASDAQ is up 29.5%. The tech-centric NASDAQ is predictably doing better than the S&P largely because of technology’s key role in work-from-home efforts and the fact that a rapid increase in online spending brought an associated push to beef up e-commerce and other SaaS capabilities that have been key to success during COVID-19.

If it’s good to be in technology right now, biotech is even better. Discount rates will reflect the state of your industry, with a realization that certain companies don’t follow the overall trend within the vertical.

2. New businesses are going to have a tougher time than those with track records. If your company has been around since before the Great Depression, it’ll be useful to show how you weathered previous downturns and how you’re applying those learnings now.

A history of strong, conservative management since company inception, with revenue growth and profits that have at least kept pace with the economy, will be important. A track record also helps in justifying your financial projections. The discount rate used in determining valuation is, essentially, an assessment of risk, so if your forward-looking statements track your history, with an adjustment for the period of COVID-19, it’ll raise your perceived value.

3. Similarly, if you were able to modify your business to stay stable or even grow during COVID-19 by changing your product mix or delivery methods, that will help establish your case for a higher valuation or better credit worthiness.

Sources not shown here are suppliers, customers and special funds. We’ve all heard about people purchasing gift cards to help local restaurants and shops, and depending on the criticality of your business to theirs, suppliers may be willing to help. There’s even a vehicle for big enterprises and philanthropies to fund grants.

8 Ways to Get Funded Without VC Cash (and Why It Might Be a Great

Idea):

Need more creative ways to raise capital, without the

“venture”? We’ve got

them.

4. Prudence is an even more attractive quality. There’s not much you can do about it now, but if you’ve got a big debt load, or haven’t used it all, it’ll weigh against you. Credit history has a determinative effect on credit worthiness in good times; now, it’ll be any easy reason for banks to say no, or for PE firms to lowball you.

5. Complete documentation and working with a well-known firm to set your valuation is critical, particularly if you’re eyeing venture or PE funding. Again, it’s all about risk, and an attestation from insiders who are known to produce reliable valuations has a calming effect.

Proving that your business was affected by COVID-19 will be key to taking part in certain SBA programs. Proving that you’re past COVID-19’s worst will determine whether you can claim the downside of it as a one-time, nonrecurring expense and create an adjusted EBITDA.

Bookbinder calls visibility into future earnings “chaos,” meaning January’s projections were completely wrong — and updates have since been pretty far off, too. So, clear documentation of ongoing business relationships and expected revenue are critical. Essentially, you’ll be required to more carefully justify your earnings projections, both short term and after the pandemic is better under control.

Where’s the Money?

SBA Economic Injury Disaster Loans are commonplace now and won’t likely require a valuation done by an outside firm. These loans are averaging around $50,000 and continue to be issued at the rate of about $12 billion a month.

Private equity activity has increased in recent months as PE firms face deadlines to either invest funds or return them to their own investors.

“With interest rates at 0%, any investment generates positive returns,” said Marty Wolf, president of martinwolf M&A advisors and an expert on prepping for M&A. “Many PE groups were doing poorly prior to coronavirus and need to invest smartly to improve returns for their funds and investors as well as for competitive purposes.”

That doesn’t mean that PE is continuing just as it was. Firms have their own risk tolerances within their funds, and certain industries are simply dicier to back now than they were last year. That means portfolios need to adjust, and in some cases, new investments won’t follow old.

The same is true in the venture space. While more likely than PE to focus on what’s hot at the moment, VCs are now more concerned with sustainable profits, having been burned on some huge deals that went south before the pandemic.

What’s changed for both: Growth alone isn’t enough.

To see just how volatile and unpredictable various market segments can be, consider PitchBook’s assessment of venture in the financial technology space:

“Venture investors closed 360 fintech deals in Q2, the lowest quarterly total in three years, yet capital invested in North America and Europe remained roughly on pace with Q1, topping $6 billion. The pandemic’s effects on different corners of the industry have been similarly incongruent, with some segments hammered while others thrive.”

In the PE market, PitchBook notes that the biggest firms are recovering after disastrous first quarters. But there are three shadows on the horizon: Federal stimulus measures end in the September timeframe, as do moratoriums on evictions in the rental market. Layoffs of workers in no-longer-supported markets are possible. Any, or some combination, of those could send new shocks through markets, a point made at this summer’s Milken Institute conference.

The result will be increased caution and avoidance of investments that could be affected by those programs ending.

Bottom line, private equity funding will be very targeted as investors look to achieve returns while avoiding industries where losses seem inevitable without further federal funding.

Art Wittmann is editor of Brainyard. He previously led content strategy across Informa USA tech brands, including Channel Partners, Channel Futures, Data Center Knowledge, Container World, Data Center World, IT Pro Today, IT Dev Connections, IoTi and IoT World Series Events, and was director of InformationWeek Reports and editor-in-chief of Network Computing. Got thoughts on this story? Drop him a line.

For more helpful information from the Brainyard and our friends at Grow Wire and the NetSuite Blog, visit the Business Now Resource Guide.