Employees’ understanding of the payroll process usually begins and ends with their paychecks. For employers, though, payroll accounting is a lot more involved. Businesses must perfect the many steps that lead up to issuing a paycheck, and many more that need to happen afterward. It’s vital to get it right because payroll accounting errors can significantly harm employee motivation — and fixing them is costly. This article explains what businesses need to know about payroll accounting, including a detailed description of the steps involved in the payroll accounting process, whether a business has just a few or many employees.

What Is Payroll Accounting?

Payroll accounting is the process of paying and recording employee compensation, including the amounts owed to employees as well as all mandated and optional withholdings, such as taxes and benefits. While that may sound simple on the surface, payroll accountants must perform a multitude of related calculations, many of which are regulated by more than one government agency. Then they have to record the results, disburse the funds and produce the reports for analyzing employee compensation, individually and in aggregate for the organization.

Key Takeaways

- Payroll accounting is the process of paying and recording employee compensation.

- Accurate payroll processing helps employers monitor labor costs, stay compliant with government regulations and maintain their employees’ trust.

- Payroll accountants must understand the various compensation structures, deductions and withholdings calculations and stay current on tax and legislative changes.

- Payroll software can ease the burden and increase the accuracy of an otherwise error-prone 12-step process.

Payroll Accounting Explained

For most businesses, the payroll accounting function is part of the accounting department but closely coordinated with the human resources (HR) team. Collaboration between the two groups is required to align the financial and compliance aspects of payroll with employee-facing issues. Payroll accountants are tasked to ensure that employees are paid the amounts they earned, accurately and on time. They must also make certain that the company is properly withholding payroll taxes and submitting them, along with the correct employer portion, to the appropriate agencies at the right times. Payroll accountants are also responsible for adjusting pay for all benefit withholdings, such as health insurance, retirement savings accounts and legal garnishments. Finally, payroll accountants must correctly record all payroll expenses and liabilities in the company’s accounting books so that labor costs can be monitored and managed.

Importance of Accurate Payroll Accounting

Payroll expenses are often many businesses’ largest cost. Payroll is also one of the most sensitive exchanges between employer and employee. As a result, accurate payroll accounting is essential — but it’s not always achieved. A recent study of U.S. companies with between 250 and 10,000 employees showed that their average payroll accuracy rate was only slightly above 80%. Furthermore, each error cost about $300 to fix, on average. Beyond the quantifiable cost of inaccuracy, other studies have shown that employees have little tolerance for payroll errors and are even willing to quit when they occur. Accurate payroll accounting is especially important for the following three purposes.

Maintain Employee Cost Records

The payroll accounting team is responsible for maintaining employee records, as needed to fulfill its mission and as required by regulatory agencies. These cost records are the part of an employee’s “file” that pertain to payroll, rather than personnel documents, like performance reviews, that would be part of the HR file. In the U.S., the Fair Labor Standards Act (FLSA) requires companies to keep certain records for nonexempt workers, who are typically hourly workers and are eligible for overtime.

Cost records include basic personal data for each employee, such as name, address, birthdate and Social Security or tax ID number. They also include pay data, such as pay rate, time sheets, contracts and work schedules. In addition, records extend to all of the source documentation for payroll deductions, such as income tax withholding forms and payroll additions, such as employer matches for retirement savings. Similar requirements exist for exempt or salaried workers, including calculations for paid and unpaid time off and bonus plans.

Maintain Records of Tax and Legal Obligations

It’s not enough to perform payroll accounting accurately. It also has to be proved. To comply with tax rules and employment laws, payroll teams must maintain various specific records. For the payroll team this means ensuring that both the employee and employer portions of taxes are paid to the respective agency on time, as well as maintaining records of those payments to verify compliance for the company and the employee. Examples include federal, state and local income taxes, Social Security and Medicare/Federal Insurance Contributions Act (FICA) taxes, state disability taxes, court-ordered garnishments and union dues.

More Easily Assess Profitability

Labor costs tend to be significant expenses for most businesses, regardless of their size or industry. It’s important that they are calculated precisely and recorded accurately in the company’s general ledger. Payroll expenses are reflected in a company’s income statement (aka the profit-and-loss statement, or P&L), where errors or omissions can significantly impact the net income or loss for the period. Classification of payroll expenses, using accurate general ledger account codes, is also important, since direct labor is part of allocated overhead, inventory costs and cost of goods sold, all of which are key variables for analyzing gross profit and managing profit margins.

Types of Payroll Accounting Entries

All payroll activity is recorded in the company’s accounting books using the appropriate general ledger accounts. Payroll expense accounts become part of the P&L, while the various payroll liability accounts are included in the company’s balance sheet. Typically, these accounting entries — also known as journal entries — are made by payroll software and automatically fed into accounting systems, although some small businesses may process payroll manually.

Generally speaking, there are three types of payroll accounting entries: initial recordings, accrued wages and manual payments.

Initial Recording

The initial recording journal entry is done for each pay period. This is the primary journal entry for recording gross wages and all of the payroll withholdings for the pay period. Gross wages are calculated based on employee time sheets and the salaries of exempt employees. Withholdings, such as payroll taxes, health insurance premiums, retirement plan contributions and garnishments, are calculated based on information employees provide in the tax and employment forms that they fill out.

Accrued Wages

Naturally, payroll processing happens before payments are made. This is one reason why most employers pay their employees in arrears — in other words, on a lag. For example, payday may be on Friday, March 27, but that paycheck will typically cover the previous workweek ended on Friday, March 20. Because of this lag, companies that follow accrual-basis accounting must accrue a liability on their balance sheets for any compensation that has been earned by employees but not yet paid. Following this same example, the next payday would be April 3, covering the workweek ended March 27. When the accounting team closes the books for the fiscal month of March, accountants will need to accrue the wages earned between March 28 and March 31 that have yet to be paid and add that to wages previously accrued for the week ended March 27 (which will be paid on the April 3 payday).

Manual Payments

The term “manual payments” can be misleading, conjuring up visions of pencil calculations and paper checks. But manual payments are simply payments made to employees separately from the normal payroll-processing cycle, aka the “off-cycle.” They are usually nonrecurring and come about to fix an error or make an adjustment, such as a retroactive pay raise or a final paycheck for a departing employee. Because of the off-cycle timing, manual payments may be processed offline or via the company’s accounts payable system instead of the regular payroll system. But either way, the information must be added to the payroll system and corresponding general ledger accounts to ensure that full-year payroll data is accurate.

12 Steps in the Payroll Accounting Process

It’s helpful to think about the steps of the payroll accounting process in four categories: company set-up, employee onboarding, payments and reporting. Company set-up (steps 1 through 4), including compensation policies, are nonrecurring, although they should be reviewed periodically. The other three categories are ongoing processes.

1. Obtain an EIN and Register with Your State

Registering a new business requires applying for an employer identification number (EIN) from the IRS. This is a unique identification number for the business, used for federal tax purposes, similar to Social Security numbers for individuals. An EIN is needed to set up a bank account and to pay employees. It generally doesn’t change unless there are structural changes to the business. In addition, businesses in most states also need a state ID number, which are used when the business remits state-level payroll withholdings for employees, as well as when it pays any company state income tax. Because state tax laws vary widely, it’s worthwhile to get advice from local tax experts.

2. Decide on Employee Compensation Factors

Businesses need to consider several policy issues before paying their first payroll. Typically, these policy decisions are made by senior company executives, HR and accounting, in collaboration. It’s a best practice to review these policies periodically to ensure that they stay aligned with company values.

- Salaries: This is the amount employees are paid, whether based on hourly rates or a preset annual amount. Salaries should be commensurate with job responsibilities, employee experience and other company-specific factors.

- Benefits: These are nonwage offerings, such as health insurance, retirement savings plans and paid time off. Employees generally view benefits together with salaries when evaluating their relationships with employers. Businesses have wide latitude in determining the benefits to offer employees, although some, such as health, worker compensation and disability insurances, are required by law in many states.

- Payroll schedule: Select the frequency of paychecks, such as weekly, biweekly, semi-monthly or monthly. Payroll schedules have a direct impact on the workload of payroll accountants and the cost of processing payroll. Lower frequency tends to be easier and cheaper for payroll processing, but employees often prefer more frequent paydays.

3. Establish a Chart of Accounts

It’s important for new businesses to set up dedicated payroll accounts when they establish their chart of accounts — a list of all general ledger accounts that acts as a sort of blueprint of the company’s financial architecture. The chart of accounts should include payroll expense accounts that will flow from the general ledger into the company’s income statement, as well as payroll liability accounts that will be reflected in the balance sheet. It’s also common for a company to open a dedicated bank account for paying payroll, with a corresponding general ledger cash account.

- Expenses: Establishing distinct general ledger accounts for each of the various payroll expenses makes it easier to track and analyze labor costs that impact a company’s P&L. Separate payroll expense accounts are usually established to show costs incurred for gross wages, overtime, commissions, bonuses and benefits.

- Liabilities: Likewise, dedicated general ledger accounts for each payroll liability help to clearly identify payroll costs that have been incurred but not yet paid. In addition to accrued wages, other common payroll liability accounts are for federal, state and local tax withholdings, FICA taxes, workers’ compensation and any benefits that have been earned by employees but not yet paid, such as accrued vacation or paid time off. In addition, liability accounts are where the employee portions of tax withholdings are recorded until they are remitted to the proper authority.

4. Complete Required Forms

Several standard forms are collected from each employee to provide information for setting up the employee’s payroll. These forms are usually completed during the onboarding process and must be maintained as part of the employee’s cost records.

- I-9: The Employee Eligibility Verification form (I-9) from the U.S. Citizen and Immigration Services is required for all employees who work for pay. It verifies that the employee has the right to work in the U.S. because they either are a citizen or have work permits (commonly called “working papers”). Proper identification, such as a passport or driver’s license and a Social Security card, is required along with the I-9.

- W-4: The IRS’s form W-4, Employee’s Withholding Certificate, must be filled out by the employee. Information on this form, such as IRS filing status, helps the employer determine how much money to withhold from the employee’s paycheck for federal taxes. A W-4 can be changed at any time, but most employees do so only when they have a major life event, such as changes in marital status, number of dependents or amount of compensation.

- Direct deposit authorization: An employee completes a direct deposit authorization form to allow the employer to send money electronically to the employee’s designated bank account(s). Direct deposit is an alternative to physical paychecks that need to be cashed or deposited. The bank’s routing number and the employee’s bank account number are the key pieces of information on direct deposit forms.

5. Collect Timekeeping Information

Collecting records of the hours worked during the pay period for all hourly employees is the first step in the payroll accounting process, and it recurs for each pay period. This information can be tracked in a variety of ways, from handwritten time sheets to sophisticated, automated timeclock software that uses badges, logins or even biometrics to track hours worked. It’s a best practice for managers to verify timekeeping information. For salaried employees, a separate system is usually used to track attendance, rather than hours worked.

6. Calculate Gross Earnings

Gross earnings are the amount an employee has earned before considering any withholdings or deductions. Also called gross wages, this is the starting point for most paychecks, so it’s important to calculate it accurately.

- Hourly employees: To calculate gross earnings for an hourly employee, simply multiply the number of hours worked in the pay period by their hourly wage. Consider fractional hours, in accordance with company policy, and overtime, if applicable.

- Salaried employees: For a salaried employee, calculate gross earnings by dividing the employee’s annual salary by the number of pay periods in the year — for example, 52 for weekly, 26 for biweekly, 24 for semi-monthly or 12 for monthly.

7. Compute Net Pay

Net pay is the final amount paid to an employee — that is, the amount of gross earnings left after all payroll deductions and withholdings. It is commonly referred to as “take-home pay.” The formula for net pay is:

Net pay = Gross earnings – Total deductions

While the net pay formula looks relatively simple, the challenge is in the details of calculating deductions. Using the forms in the payroll cost records, each deduction must be calculated individually for each employee. This includes taxes, FICA, employee retirement contributions, medical insurance premiums, life insurance premiums, union dues and legal garnishments.

8. Issue Payments

At this point, it’s finally time to pay employees (on the scheduled payday). Payments are typically made via paper check or direct deposit. Alternative disbursement methods, such as payroll cards and mobile wallets, are becoming increasingly popular but come with additional payroll accounting challenges for record-keeping and compliance. Regardless of the distribution method, a payroll remittance or “pay stub” is also issued to the employee, showing all the details of gross wages, deductions and net pay.

9. Pay Payroll Liabilities

Payroll liabilities are a catch-all term for any payroll-related amounts owed by the employer that have been incurred but are not yet paid. This step involves paying those liabilities to the various agencies. It’s actually a multistep process that can be tricky and time-consuming because each type of payment has its own due date and remittance process. For example, when dealing with federal tax liability, an employer forwards the amounts withheld from employees and the employer portions using a tool from the U.S. Treasury Department called the Electronic Federal Tax Payment System. This must be completed on a particular schedule, as described in IRS Publication 15, to avoid late fees. Along the same lines, state and local tax liabilities have their own payment schedules and processes. Other typical payroll liability payments include FICA, insurance premiums, employee contributions to retirement plans and any employer-matching contributions.

10. Prepare Payroll Reports

At the end of each payroll period, payroll accountants prepare several payroll reports. Some are used for internal analysis to help a company monitor and control its labor costs. Internal payroll reports can be customized to highlight information that is pertinent to the business, such as overtime costs, labor costs by department or employee turnover. These reports are also helpful for preparing budgets, forecasts and cash flow projections. Other reports are mandated by the FLSA and/or the IRS. Preparing these reports helps an employer track its tax liability and stay compliant with regulations.

11. Maintain Records

Maintaining payroll records serves two purposes. First, it achieves compliance with FLSA and IRS regulations, which require records to be held for three and four years, respectively. Second, payroll records give the company important data to help manage employees and reconcile any disputes.

12. Review and Reconcile

Payroll errors can be costly, so it’s essential to regularly review payroll and reconcile any errors quickly. Mistakes can rack up fees and penalties from agencies like the IRS. They can also embarrass the organization and create ill-will with employees. For example, having insufficient funds in the payroll bank account can cause payday delays and incur bank charges. Reviewing payroll runs for input, calculation and processing errors is a best practice, whether payroll accounting is handled internally or outsourced. Payment reconciliation, where payroll records are matched against general ledger accounts, bank statements and digital wallet data, helps uncover errors and detect potential fraud.

Challenges of Manual Payroll Accounting

Payroll accounting is challenging and requires significant expertise, which is why many companies choose to outsource the function. For those that don’t, most use automated software. The minority of businesses that do their payroll processing manually face a long list of challenges beyond the obvious risks of manual error. Three top challenges — legislative changes, varied pay structures and managing remote and international workers — can create significant problems for employers that don’t get them right.

Keeping Up with Legislative Changes

Payroll legislation and tax codes are constantly changing. HR and payroll teams stay current through self-study, training seminars, webinars and articles like this one about tax credits. It takes time to keep up with legislative changes — time that just isn’t available when performing manual payroll accounting. But failing to keep up can have significant repercussions for employers, including costly penalties.

Handling Different Pay Structures and Compensation Packages

Calculating gross earnings may appear straightforward on the surface. But when a company uses several different pay structures for different positions, it becomes more difficult. Consider the time consumed and potential for error when payroll accountants switch from manual calculations for hourly employees to the different formulas needed for salaried workers, commissions, tip-eligible, union scale and other compensation schemes.

Managing Payroll for Remote and International Employees

The way businesses recruit talent has changed in the past few years as the percentage of mobile and remote workers has increased. While this offers many advantages, it also brings significant challenges to payroll accounting. Consider that payroll managers must now become familiar with the regulations and processes of every locale where a remote employee resides, such as state tax withholding rules and the many more agencies to which they might owe payroll liabilities. Crossing international borders compounds the complexity, since other countries have unique labor laws and taxation schemes, some of which are governed by international treaties.

When to Use Payroll Software

Determining when to switch from manual payroll to payroll software is often a matter of circumstance. Companies make the move, for example, when the time and effort in manual payroll becomes overwhelming, when the complexity of compensation packages and taxes become unwieldy, or when errors and noncompliance become commonplace. At such times, payroll software is a game-changer for payroll accounting. It helps a company organize and store all payroll documents, such as cost records and pay data. It automates payroll accounting tasks, including reviews and approval workflows, and reduces calculation errors. And payroll accounting software is typically updated automatically to reflect current tax schedules and legislation.

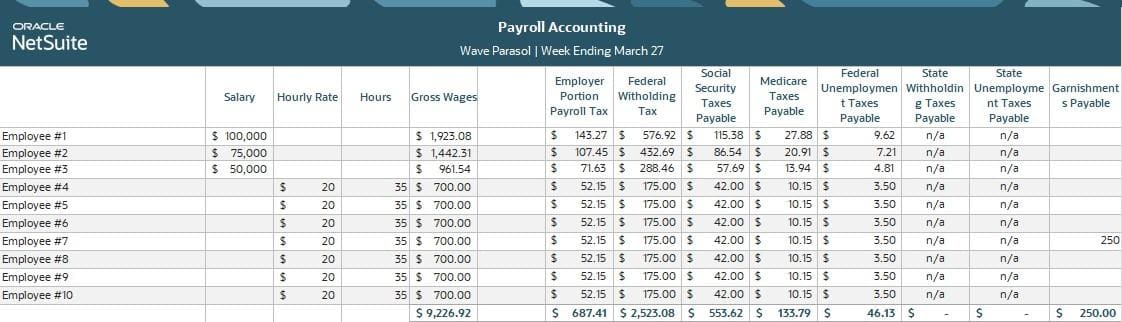

Payroll Accounting Example

Let’s look at an example of a typical payroll journal entry. The journal entry is made in the payroll journal, a subsidiary to the general ledger, for every payroll cycle. The payroll journal is summarized and transferred into the general ledger using the payroll accounts included in the chart of accounts.

Wave Parasols, a fictional retailer of parasol umbrellas, employs 10 people. Three are salaried, earning $100,000, $75,000 and $50,000 per year. The other seven are paid $20 per hour and work varying amounts of hours each week. They all reside in a state that does not have income tax or state unemployment taxes and are paid weekly. One employee has a court-ordered garnishment of $1,000 per month. For the week ended March 27, the payroll accountant made the following calculations:

Using the information calculated above, the payroll accountant makes the following journal entry to record the weekly payroll:

| Debit | Credit | |

|---|---|---|

| Gross Wages | $9,226.92 | |

| Payroll taxes expense (ER) | $687.41 | |

| Cash | $6,407.71 | |

| Federal withholding taxes payable | $2,523.08 | |

| Social Security taxes payable | $553.62 | |

| Medicare taxes payable | $133.79 | |

| Federal unemployment taxes payable | $46.13 | |

| State withholding taxes payable | $ - | |

| State unemployment taxes payable | $ - | |

| Garnishments payable | $250.00 |

Streamline All Your Business Functions With NetSuite

Payroll accounting is an important function in any business, but it can be challenging and time-consuming. Consider the hypothetical example above, showing the work and calculations required for one weekly payroll in a company with just 10 employees. Payroll software helps relieve the burden and reduce the likelihood of errors by making all of the tedious calculations, from gross compensation through all the deductions and withholdings, to pay the right amount of net pay. It can also automate the process of remitting funds to various agencies and disbursements to employees. When integrated with a dynamic accounting system, like NetSuite’s cloud accounting software, payroll information can automatically flow into a company’s general ledger. NetSuite eliminates the need to upload payroll data into your accounting software and enables monitoring and managing it with role-based dashboards that highlight the KPIs that matter most to your organization. Additionally, because it’s in the cloud, compliant payroll records are securely stored.

Payroll accounting is a critical process that covers calculating, recording and paying compensation to employees. Moreover, it’s a complex process with many steps that happen before and after payday, bearing a significant cost that requires continual management oversight and analysis. Getting it right means overcoming significant challenges, such as handling various compensation structures without error and staying abreast of tax and legislative changes. Most companies rely on automated payroll and accounting software to stay on top of payroll expenses, comply with government labor and tax regulations — and to pay their employees correctly and on time.

Payroll Accounting FAQs

What types of expenses fall under payroll accounting?

In addition to gross earnings, other expenses that fall under payroll accounting include overtime, commissions, bonuses and benefits. Further, all payroll withholdings and deductions are handled as part of payroll accounting, such as federal, state and local tax withholdings, Federal Insurance Contributions Act (FICA) taxes, workers’ compensation, paid time off, retirement plan contributions, insurance premiums and garnishments.

Is payroll accounting hard?

Payroll accounting is complex and has little tolerance for errors, which makes it difficult. It becomes harder as each of these factors increase:

- Number of employees

- Variety of compensation structures

- Locations where employees reside

- Pay cycle frequency

- Benefit deductions

- Employee payment options

What is a best practice for payroll accountants?

A best practice for payroll accountants is to use automated payroll software. Doing so reduces the amount of time involved in payroll tedium and increases calculation accuracy, especially for tax withholdings.

What is a payroll journal entry?

Payroll journal entries are made in a company’s payroll journal to record compensation-related financial activity for every payroll cycle. The payroll journal is summarized and transferred into the general ledger using payroll accounts included in the chart of accounts.

Is payroll HR or accounting?

The payroll accounting function is part of the accounting department in most companies. However, the two departments work closely together to appropriately address the financial and compliance aspects of payroll along with the employee-facing issues.

How to do payroll as a bookkeeper?

Bookkeepers can be involved in payroll accounting in several ways. They are typically tasked with keeping payroll records up to date so that all changes are processed prior to upcoming payroll cycles. This includes entering new hires, pay rate changes, W-4 changes and benefit updates. Payroll bookkeepers also may be called on to maintain accurate payroll records and run internal and/or government-mandated payroll reports.