Regardless of a company’s size or financial sophistication, the financial close process can become convoluted. Sequential steps — from recording transactions to generating financial statements — must be done efficiently, collaboratively and accurately before accountants can close the books on the current fiscal period. Fortunately, there are ways to make this recurring process more manageable and give financial teams and stakeholders the time they need to conduct analyses and make strategic business decisions.

What Is Financial Close?

The term “financial close” describes all the financial and accounting processes that regularly occur in a business leading up to, and including, closing the books on the preceding month, quarter or year. The eight core steps are identifying transactions, recording transactions in a journal, posting to the general ledger, preparing an unadjusted trial balance, reconciling debits and credit, creating adjusting journal entries, running an adjusted trial balance and financial statements, and closing the books to reset income statement accounts to zero and lock in balance sheet accounts as of the period’s end.

In companies with multiple subsidiaries, the financial close also includes consolidating the division’s financial statements, analyzing for intercompany eliminations and other post-closing adjustments. For external financial statements, data for footnotes and other disclosures are also generated.

The resulting financial statements are used by management to generate historical trend analysis, comparisons to prior periods and budgets, and to generate KPIs. In companies with real-time systems, this analysis may be ongoing. The financial statements are also used, and sometimes required, by external stakeholders, such as investors, lenders and public regulatory agencies.

Financial Close vs Closing the Books

Some finance teams use the terms “financial close” and “closing the books” somewhat synonymously. However, there is a key distinction between the two:

-

The financial close is a broad term that reflects all accounting processes for the month including, but not limited to, closing the books. The financial close encompasses the whole accounting cycle, culminating with generating financial statements and closing the books.

-

Closing the books is the last step in the financial close process and has two objectives. One, closing the books resets temporary accounts to zero and locks in the prior period’s balance. Temporary accounts, also referred to as nominal accounts, are those found on the income statement to accumulate the period’s revenue, expenses, gains and losses.

The net result is transferred to the balance sheet as part of the second objective: updating retained earnings to reflect that period’s results of operations. Retained earnings is an equity account found on the balance sheet, which holds undistributed profit or loss. It’s an important account, since it represents funds available for reinvestment.

Even accountants might casually use the “financial close” and “closing the books” terms synonymously, but the clear distinction is that closing the books is one step within the financial close. Nevertheless, all the steps within the financial close process are interdependent; errors in one step ripples through the entire process, so it’s important to get it right.

Key Takeaways

- The financial close is a key business process that ultimately provides an accurate snapshot of a business’s financial health.

- Closing the books is one step within the financial close process. Delays, inaccessible data, complex data sets and lack of process rigor make it difficult to achieve a timely and accurate financial close. The faster a business can close the books, the better. But companies should never sacrifice accuracy for speed.

- Process improvements, like continuous accounting, combined with automated accounting software can help make the entire financial close more manageable.

Financial Close Explained

The financial close process is integral to all organizations because it aims to provide stakeholders — line-of-business managers, financial analysts, executives, board members, investors, lenders — with an accurate account of the company’s financial position on a monthly, quarterly and annual basis.

Financial statements produced during the financial close process are used by internal management to communicate the health of the company to external stakeholders and to gauge results against preset objectives. Combined with other operational data, the underlying historical data in the company’s books are used for financial analysis, budgeting and forecasting.

It’s often said that CFOs help steer the economic health of their companies with one eye on the rearview mirror and one on the road ahead. The financial close process is an infamously tedious and time-consuming process, and financial statements — a key output— are valuable only when accurate and timely. Unfortunately, in many organizations, the financial close process is disjointed, inefficient and labor-intensive. In fact, a common KPI that CFOs monitor is cycle time for monthly close, in the effort to get financial data and statements in the hands of users more quickly and to redeploy accounting resources to higher value projects.

Financial Close Challenges

The financial close process, by its nature, can be difficult. Even small businesses may have dozens of accounts to track and reconcile, and it only gets more complicated as firms grow. International enterprises and companies with highly dispersed finance teams have their own challenges.

Here are six the top financial close challenges:

-

Need for speed: When it comes to the financial close process, a tension exists between getting the job done fast and getting it done right. The more easily accounting teams can access key financial data, the faster they can close the books.

-

Poor-quality or missing data: Whether it’s duplicate data, unrecorded payments, missing invoices, simple typos or calculation errors, finding and resolving inaccurate or incomplete data costs time and effort.

-

Disparate systems: It’s not always easy to track down all the necessary information and ensure all transactions from every business department have been accurately recorded in a single business location. Further, businesses with multiple operating entities typically use local accounting systems, and those may not integrate well at headquarters. For example, different locations may use different versions of accounting software or even wholly different systems. The greater the number of local instances, the more likely integration issues may arise, caused by inconsistent or inconsistently applied charts of accounts and other formatting disparities. International businesses with multiple locations all over the world and in different time zones can experience even more challenges, especially in the absence of strict schedules. Disparate systems can increase the likelihood of error, increase the number of closing issues, which reduces the efficiency of the accounting staff — and all of which can ultimately delay the production of consolidated financial statements.

-

Remote teams: Like data, accounting teams can be scattered and working remotely. Some teams closed the books virtually for the first time in 2020 and found a few key strategies helped make their remote closes go more smoothly. These included effective collaboration systems, mapped-out processes and solid security practices.

-

Human error: For many accountants, a combination of high-pressure deadlines and repetitive tasks makes the closing process one of the least enjoyable aspects of the job. For example, accountants might spend hours or even days doing little more than transferring numbers and double-checking calculations — with the risk of mistakes increasing the more the financial close process relies on manual data entry.

-

Under-supported teams: Some organizations lack the time, systems and/or staff to work on a continuous close and are stuck with manual processes, antiquated batch systems and paper documents. Inadequate support can lead to a vicious cycle that takes more time and manpower and still results in untimely information that is of little value. In turn, some companies resist investment in what has been seen as useless information and the process that supports it. The impact on accounting employees is significant and adds to the likelihood of errors as workers might purposely or unintentionally skip important steps just to get done.

6 Common Financial Close Challenges

-

It takes time: Closing is often a tedious, time-consuming process. But the sooner it’s done, the sooner businesses without robust, real-time financial systems can begin using the accounting data.

-

Bad data: Accurate financials depend on accurate data. But the closing process can be prone to errors like typos and formula errors, especially when handled manually or with spreadsheets.

-

MIA records: To close, financial teams need timely input from a variety of departments. That’s challenging, especially if other teams lack the resources or sense of urgency or see the value in the end result.

-

Far-flung teams: When department heads and accounting are not in the same office, that adds a new level of difficulty.

-

Mistakes are made: The closing process is infamously labor-intensive and repetitive with hours — or days — spent transferring numbers and double-checking calculations. Still, errors happen.

-

Lack of resources: Without enough staff and the right software, the close process can be inefficient and feel demoralizing to the accounting staff.

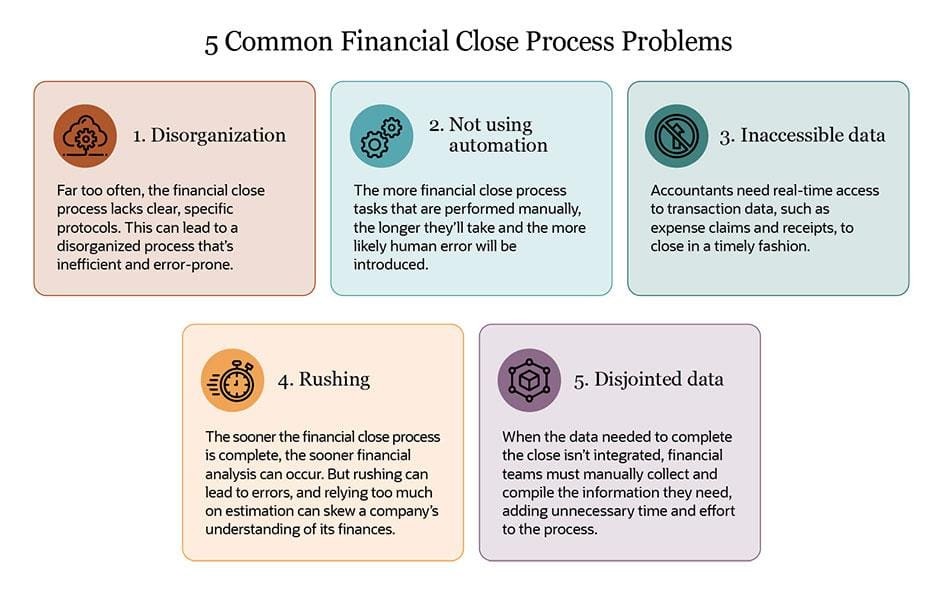

5 Common Financial Close Process Problems

While the financial close process is by its nature challenging, many organizations face avoidable process troubles that unnecessarily contribute to the difficulty. Addressing the following five common financial close problems could drastically improve your financial closing cycle.

-

Process lacks definition and organization: The financial close process is often run by institutional memory instead of clear, specific, documented protocols. Many accountants know close processes and have done it the same way for years, meaning rigorous standard operating procedures (SOPs) seem unnecessary. But just because they know how to get it done doesn’t mean there isn’t room for improvement.

Similarly, employees might have their own ways of reporting expense claims, for example, further contributing to the challenge of getting all the right information in the right place when closing. No matter what, lacking a uniform process breeds disorganization and potential errors, both of which add to the time and effort it takes to work through the close process.

-

Process lacks automation: The more tasks within the financial close process that are performed manually, the longer it’s going to take and the more opportunities for error open up. Automation and accounting software reduces the need to rely on manual workflows.

-

Process lacks complete data: Closing requires compiling data from all around the business — a process that quickly can become chaotic, especially if transaction data isn’t complete. Examples like missing purchase orders, invoices and expense reports can cause account balances to be incorrect if not filed according to company policies. Alternatively, incomplete data causes the accounting team to lose time and efficiency while tracking down critical details in the midst of the financial close process.

-

Process is rushed: The sooner the financial close process is complete, the sooner financial statements can be issued to the various stakeholders, the underlying data used for historical analysis and the accounting team can move on to more value-added tasks. But that’s not an excuse to take shortcuts. The ultimate output of the financial close, the financial statements, are often the face of the company to external parties, and errors can undermine the company’s reputation.

-

Process lacks integration: When the data necessary to complete the close is in disparate systems, accounting teams are forced to manually collect and compile information. This adds more time and risk of error into the financial close process.

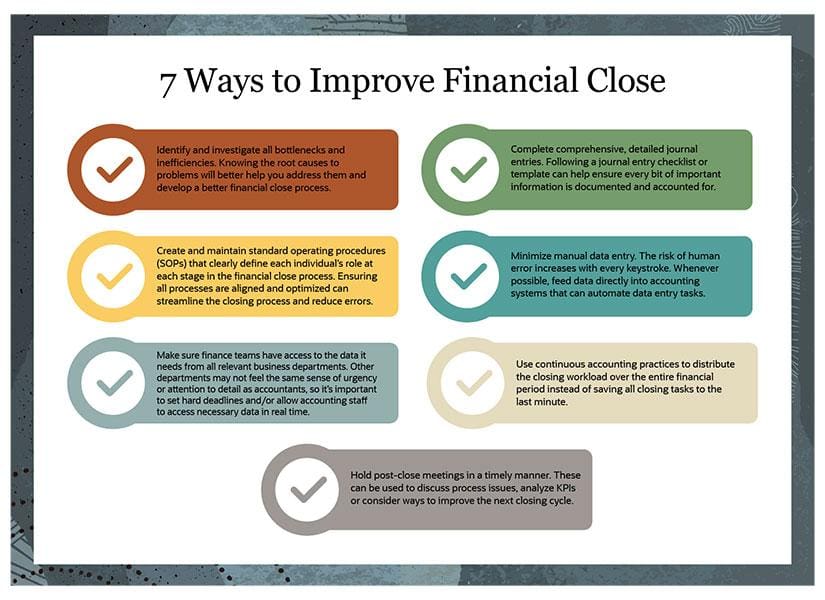

7 Ways to Improve Financial Close

Improving the financial close process doesn’t make life easier only for accountants, CFOs and the broader finance teams. It can also give executives and other business stakeholders timelier access to relevant financial data to help inform decision makers.

The less time spent closing, the more time organizations have to analyze operations, reallocate resources and evaluate whether they have the cash to take advantage of new opportunities. Still, accuracy cannot be sacrificed for speed, which means organizations must work smarter, not harder.

Here are seven ways companies can improve the financial close process:

-

Identify inefficiencies: The first step any organization should take is to find bottlenecks and inefficiencies. For example, are you waiting until the end of the month to reconcile accounts? Have you directed employees and vendors to submit invoices electronically, in a format that can be imported directly into your accounting system? Has your chart of accounts grown too big and complex? Knowing the root causes of process problems will set you on the right path.

-

Create and maintain standard operating procedures (SOPs): A financial close that lacks a documented, step-by-step operating procedure is going to be inefficient. To streamline the process, every individual or team involved in closing — whether an accountant working directly on the close or an employee tracking lunch expenses — should follow a clear and precise SOP. SOPs provide standardized, detailed instructions to ensure all steps in a financial close process are aligned and optimized for fewer errors and easier access to information. SOPs should indicate which tasks need to be completed when and by which role and include hard deadlines so accounting teams aren’t stuck waiting to receive data at the last minute.

-

Open access to information: To complete a close, accounting teams need data from all business departments: sales, shipping, procurement, marketing, human resources. Of course, these teams might not feel the same sense of urgency or attention to detail that accountants do. While hard deadlines can help, it’s also important that authorized accounting staff have direct access to the systems where this information is stored so they aren’t relying on departments for updates.

-

Document comprehensively: A better financial close process starts with better journal entries. Create a journal entry checklist that must be followed each month to ensure every bit of information is documented and accounted for. Journal entries should include type of transaction, the date executed, amount, a brief description, a journal number identifier and any other information relevant to your business and closing process. Consider using a journal entry template to ensure every journal entry is logged comprehensively.

-

Minimize data entry: Data-entry errors can be reduced by avoiding paper whenever possible. Besides electronic invoices that can be imported directly into accounting systems, avoid using spreadsheets when possible. Though convenient for managing calculations like depreciation and allocations, it’s more efficient to feed data directly into accounting systems that can automate these tasks.

-

Use continuous accounting practices: Continuous accounting, or a continuous close process, distributes the workload over the entire month, instead of accumulating them for the end of the month. For example, responsibilities like posting journal entries and reconciling accounts might be embedded in day-to-day activities, which will keep the general ledger up to date. In this way, a company is able to do a “soft close” at any point during the month and will greatly reduce the workload during a “hard close.” What’s more, accounting teams using continuous accounting may spot errors sooner so they don’t delay closing the books.

-

Hold post-close meetings: As long as they’re held in a timely manner so all information is still fresh in the mind and attendees aren’t already focused on the next cycle, post-close meetings can be helpful to review issues, track KPIs and discuss topics that could help the organization improve its next close cycle.

7 Steps to Better Financial Closes

-

Break bottlenecks: Find the factors slowing the process down and fix them. This may need to happen gradually.

-

Stick to SOPs: Write down standard operating procedures that clearly define each individual’s role and deadlines for each stage in the financial close process.

-

Distribute data: Ensure accounting teams have access to all sources that feed into the close and that departments have hard deadlines for data entry.

-

Templatize journaling: Create a journal entry checklist or template to help ensure every bit of important information is documented and accounted for.

-

Minimize manual data entry: The risk of human error increases with every keystroke. Whenever possible, feed data directly into accounting systems and automate data entry tasks.

-

Embrace continuous accounting: Do: Distribute the closing workload over the entire financial period. Don’t: Save all tasks for the end of the period.

-

Hold post-close meetings: No one wants another meeting, but it’s worth taking some time to discuss process issues, analyze KPIs and brainstorm ways to improve.

Make the Financial Close Process Easier With Accounting Software

With the right business accounting software — such as cloud-based financial management software that can integrate with enterprise resource planning (ERP) systems — businesses can improve processes and devote more time to valuable tasks, such as financial analysis and forecasting. For example, business accounting software can:

-

Turn monotonous tasks into repeatable automated functions by eliminating many manual chores, like transferring journal entries into the general ledger, thus reducing human error.

-

Improve the reconciliation process by automatically aligning data from discrete sources, spreadsheets and systems. Accounting software can also quickly detect errors so they can be mitigated as quickly as possible.

-

Integrate data and keep all information consistent. This makes it easier for accounting teams to access key financial data in real time, instead of waiting for peers to share the information necessary to complete a close. ERP systems can enable all departments to work from the same up-to-date data sources.

-

Provide real-time dashboards that give finance teams, management and executives access to the numbers they need to see, when they need to see them.

Modern business accounting software as part of an integrated ERP system can reduce the amount of time it takes to complete the financial close cycle. In turn, this allows accounting professionals to devote time to more valuable activities, like financial planning and analysis, instead of always playing catch-up.

The financial close is extremely important for the business. These reports provide an overview of a company’s financial health and support forward-looking decisions. But a financial close is a complicated process — the sheer amount of data finance teams must parse alone can be intimidating. To improve the financial close process, companies should look at the process holistically while taking advantage of accounting software that can automate error-prone tasks.

Financial Close FAQs

Q: What is the financial close process?

A: Here’s a simple breakdown of the financial close process:

- Identify transactions.

- Record them into a journal. Ideally, financial activity should be automated and recorded as it happens.

- Post transactions to the general ledger.

- Prepare an unadjusted trial balance.

- Reconcile all accounts to ensure all debits equal all credits.

- Create adjusting journal entries. Journal entries should include journal number, date, description and accounts affected.

- Run an adjusted trial balance and prepare financial statements. Ideally, companies should aim to generate these reports through accounting systems that automate the task to save time and minimize errors.

- Close the books for the time period. Once financial statements are accurate and management is satisfied with results, the accounting period is closed, preventing any unauthorized transactions in a period that has already been reported.

Q: What is month-end close?

A: The month-end close is the series of steps a company takes to ensure its monthly financial statements are true to the accounting equation (Assets = Liabilities + Equity). In other words, all temporary account balances for that period are reverted to zero to prepare for the next period, and the monthly financial statements provide an overview of the period’s transactions.

Q: How long should it take to close the books?

A: How long it takes to close the books depends on your business, how complex your finances are, your accounting team and whether you use automation. According to one study, companies that use spreadsheets extensively take an average of 8.2 days to close, while those that automate most tasks take about 6.2 days. Other data suggests top performers take 4.8 days to close, while low performers take as many as 10 days.

Q: What does Wd5 mean?

A: Wd5 refers to “workday 5,” or the fifth working day after month end. Closing by Wd5 is a common goal for many midsize companies, whereas world-class organizations may strive to close by Wd1, or the first working day after month end.