Companies need to make sure their books are balanced and that they reflect all financial activity that occurred during an accounting period before the books are closed. This is accomplished through the accounting cycle, an eight-step process that helps businesses keep track of their financial activities by documenting, sorting, and analyzing all transactions to make sure that each one is accounted for. When handled manually, each step of the accounting cycle can be time-consuming, tedious, and prone to error. Automating the process increases efficiency and reduces potential risks of misstatement.

What Is the Accounting Cycle?

The accounting cycle is a multistep process used by businesses to create an accurate record of their financial position, as summarized on their financial statements. During the cycle’s various stages, companies will record their financial transactions in a journal, transfer the details into a general ledger, analyze the entries, and make sure the books are balanced and error-free before generating financial statements and closing the books for the period.

The amount of time it takes a company to advance through the accounting cycle depends on several factors, including the volume of transactions, whether it uses automated accounting software, and the type of financial close. A hard close is a thorough approach to closing the books, verifying that all information is accurate and marking the end of financial activity for an accounting period. A soft close is more like a solid estimate, typically used for internal management reporting, not for public or investor purposes. Ideally, a business will engage in a “continuous close,” spreading the workload across the course of the accounting period, rather than waiting until its end. This results in a faster close, regardless of whether the target is a weekly soft close or a hard close at the end of a quarter.

Key Takeaways

- Before companies can close their books, transactions must be balanced and devoid of errors.

- The accounting cycle is an eight-step process companies use to accurately identify, record, and report their financial transactions during a given period.

- Once the accounting cycle is completed, financial statements can be generated.

- Following the accounting cycle creates a foundation for enhanced financial insight, better compliance with standards and regulations, and data-driven decision making.

Accounting Cycle Explained

The accounting cycle consists of eight steps used by businesses to ensure balanced books that close easily and reset for the next accounting period, when the cycle begins again. Typically the domain of an accounting team or bookkeeper, the accounting cycle begins with a business event or transaction. Ensuing steps include data analysis and adjustments, if necessary. The sequence culminates in the preparation of standardized reports that reflect the company’s financial performance and help guide internal and external decision-making.

Why Is the Accounting Cycle Important?

Managing the accounting cycle effectively is vital for any business. The cycle offers a structured and repeatable process for recording, summarizing, and reporting all the financial transactions that have taken place during a given period. Having a systematic method in place allows the business to accurately capture each transaction, thereby minimizing the likelihood of errors or discrepancies in its financial records. These records then serve as a solid foundation for performing financial analysis and forecasting, maintaining compliance with financial regulations, and—most importantly—making data-driven, financially sound business decisions.

The Purpose of the Accounting Cycle

The main purpose of the accounting cycle is to keep track of all financial activities that occur during a specific accounting period, be it monthly, quarterly, or annually. In short, the accounting cycle verifies that every dollar going into or out of the various general-ledger accounts is reported.

Some steps in the accounting cycle are more tedious than others, but each one enables bookkeepers or accountants to diligently check their work before proceeding. This is especially crucial for the final steps of the accounting cycle, when financial statements are created and the books are reset.

Benefits of the Accounting Cycle

Companies that invest in effective accounting cycle management—implementing repeatable processes and investing in technology-enabled automation—experience a number of valuable benefits. These include:

- Greater accuracy and reliability: Following the accounting cycle reduces the likelihood of errors and discrepancies that may result from a more ad-hoc approach to accounting or bookkeeping. This increased accuracy builds trust in financial reports and provides a solid foundation for audits and financial reviews.

- Improved efficiency: A well-defined accounting cycle streamlines the bookkeeping process, freeing up accounting professionals to focus on higher-level analyses or tasks. This efficiency can lead to cost savings and improved resource allocation within the finance department.

- Enhanced compliance and standardization: The accounting cycle helps companies comply with accounting principles, standards, and regulatory requirements. A systemic process increases the consistency of recording and reporting financial information, which can make it easier to conform with legal and tax obligations.

- Increased visibility into financial performance: Because all financial activities are documented and therefore traceable throughout each step of the accounting cycle, this structured approach also boosts transparency into financial transactions and the overall financial position of the company. Such visibility facilitates quicker identification of financial issues or opportunities for more proactive financial management.

- Support for informed decision-making: A business that follows the accounting cycle is able to generate more reliable financial statements and reports. This provides a foundation for better decision-making by internal executives and managers, as well as investors, lenders, and other external stakeholders that require accurate visibility into the company’s financial standing.

- Consistency in financial analysis and planning: When a company consistently applies a full-cycle accounting approach, it creates a basis for comparing financial information across different reporting periods. This allows for better forecasting, trend analysis, and more meaningful benchmarking against industry standards and competitors’ performance.

What Are the 8 Steps of the Accounting Cycle?

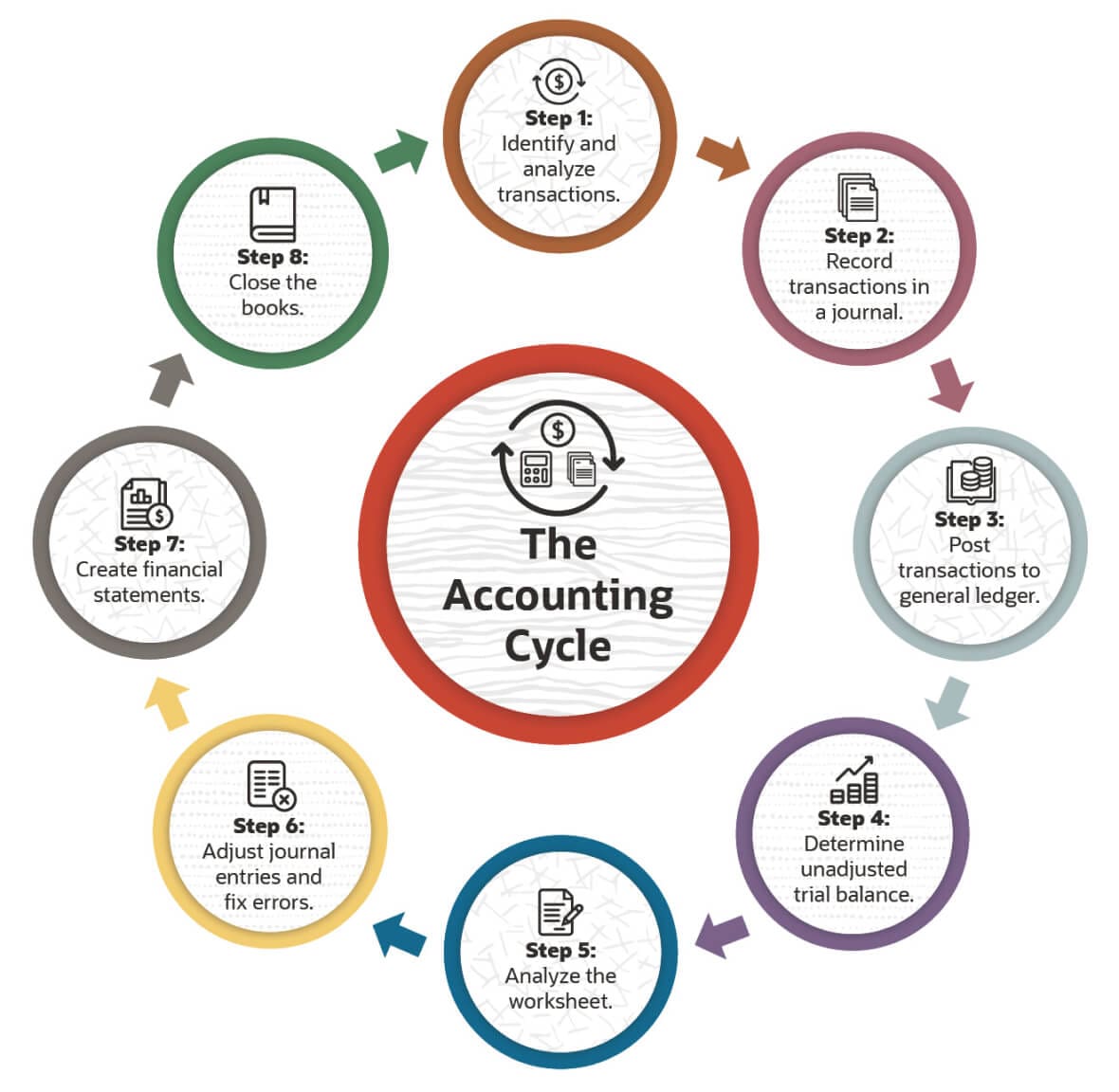

The goal of the accounting cycle is to develop an accurate account of a company’s financial position. The eight steps of the accounting cycle are:

- Identify and analyze transactions.

- Record transactions in a journal.

- Post transactions to a general ledger.

- Determine the unadjusted trial balance.

- Analyze the worksheet.

- Adjust journal entries and fix any errors.

- Create financial statements.

- Close the books.

-

Identify and Analyze Transactions

The first step in the accounting cycle is to identify and analyze all transactions made during the accounting period, including expenses, debt payments, sales revenue, and cash received from customers. During this initial stage, companies go through every transaction that affects their financials, though this should be an ongoing step for companies in a cycle of continuously creating customer invoices, buying inventory, paying bills, making payroll, and collecting cash.

Say, for example, a small business that sells custom picture frames—let’s name it Picture Perfect—sells a customer a $350 frame. This marks the accounting cycle’s starting point.

-

. Record Transactions in a Journal

The next step is to record the details of all financial transactions, in chronological order, as journal entries, whether in an actual book or in an accounting program. With double-entry accounting, each transaction is recorded as a debit and corresponding credit in two or more subledger accounts. Exactly when the transaction is recorded depends on whether the business prefers the accrual accounting method (as most do) or the cash accounting method.

When Picture Perfect generates an invoice for the $350 transaction in its billing system, the transaction is recorded (at its simplest) as a $350 debit in the accounts receivable (AR) subledger and as a $350 credit in the revenue subledger.

-

Post Transactions to a General Ledger

Once journal entries are recorded and approved, they are posted to the general ledger (GL). The GL is the master record and summary of all financial transactions, broken down by account.

On the same day Picture Perfect sold the $350 frame, it sold another two frames for $200 apiece. The total of the three sales is detailed in the AR subledger and posted to the GL.

-

Determine the Unadjusted Trial Balance

The trial balance reflects the closing balances of all the accounts in the GL at the end of an accounting period. At this point, the trial balance doesn’t reflect any adjustments that need to occur if errors—i.e., unbalanced debits and credits—are caught. That’s why it’s considered “unadjusted.”

Picture Perfect adds up the amounts of debits and credits, confident that the totals will balance.

-

Analyze the Worksheet

This step identifies errors and anomalies that may occur up until this point by lining up debits and credits from various accounts in a single spreadsheet. If the numbers don’t balance, a bookkeeper or accountant will need to review the transaction data entered into the journal and adjust entries accordingly.

Picture Perfect’s bookkeeper pours himself a coffee, puts on his reading glasses, and gets to work. He compares the balance of debits to credit and is surprised to find a $100 discrepancy.

-

Adjust Journal Entries and Fix Any Errors

This step is a continuation of the two previous steps. Any errors require correction and additional recording as an adjusting journal entry that reflects a change to a previously recorded journal entry. Additionally, manual adjustments are recorded in this step, such as accruals for expenses incurred that didn’t make it into the AP system before that account was posted to the GL, or for reconciling items uncovered during the account reconciliation process.

It doesn’t take long before Picture Perfect’s bookkeeper discovers the mistake: The $350 frame sale was mistakenly entered as $250. He creates an adjusting journal entry for $100 to correct the error.

-

Create Financial Statements

With adjustments completed and correct account balances, staff can now create financial statements. Financial statements are accounting reports that summarize a company’s activities and performance for a defined period of time, such as monthly or quarterly. The three key financial statements that companies generate are the income statement, the balance sheet, and the cash flow statement.

Picture Perfect’s bookkeeper is satisfied that the company’s financial statements are accurate and properly reflect its financial health.

-

Close the Books

This is the final stage of the accounting cycle, locking in the accounting period. Closing the books resets temporary accounts on the income statement, such as revenue and expenses, to zero balances, meaning that they don’t carry into the next accounting period. Net income or loss from the income statement is transferred to the retained earnings account, which is a permanent account on the balance sheet that carries over to the next period. Of note: the resetting of accounts to zero doesn’t apply to a soft close.

Picture Perfect’s bookkeeper clears off his desk and gets ready for the next day, when he starts working on the new accounting period.

Customizing the Accounting Cycle

While the steps of the accounting cycle are typically the same for most companies, a business must be consistent in its approach should it decide to do anything differently. One surefire way to achieve that is by using automated accounting software with customizations for handling the cycle in the best way possible for any company’s given circumstances.

Go from closing in days to closing in hours.

Accounting Cycle vs. Budget Cycle

The accounting cycle and the budget cycle are separate processes. The accounting cycle applies to transactions that have already occurred, from the moment they take place until financial statements are generated and the books are closed. The budget cycle looks at a business’s future expenses to determine strategies for allocating funds without spending more than available.

Accounting Cycle Timing

The accounting cycle kicks in the moment a sale is made. Thus, it’s a continuous process that culminates at the end of an accounting period—which can be a month, quarter, or fiscal year—only to start again when a new period begins the following day. Automated accounting software accelerates the cycle so that accounting staff have to focus only on analysis and possible adjustments, therefore cutting costs, saving time, and ensuring the accuracy of financial statements.

Automate the Accounting Cycle With Financial Software

NetSuite’s Cloud Accounting Software automates and simplifies every step of the accounting cycle, from creating journal entries all the way to creating financial statements that reflect the business’s profitability, net worth, and solvency. The software manages accounts payable and receivable, provides real-time dashboards and reporting capabilities, generates and disseminates financial statements in compliance with accounting regulations, and accelerates the financial close process. This automation saves accounting teams and bookkeepers time, reduces business costs, and facilitates more accurate financial reporting.

The accounting cycle is a series of steps that begin the moment a transaction occurs and culminates when a business closes its books at the end of an accounting period. From recording journal entries and posting to the general ledger to calculating a trial balance and analyzing results to correcting errors and issuing financial statements, each and every step in the cycle is essential to help provide the highest level of accuracy. Automation eliminates the need for a significant amount of manual intervention, thereby expediting the process so businesses can close their books with confidence.

Accounting Cycle FAQs

What is a “soft close?”

A “soft close” takes place when companies want to close their books quickly but not definitively, such as for internal management reporting purposes. It’s generally understood that results may be materially inaccurate, unlike a “hard close,” where a more rigorous approach ensures accuracy of reporting and eventual financial statements so that the books can be closed for an accounting period.

What is the purpose of the accounting cycle?

The accounting cycle is an effective way for companies to systematically record all financial transactions during an accounting period. The eight-step cycle helps companies make certain their financial information is correct before they close their books and reset them for the next accounting period.

What is the difference between a journal and ledger?

A journal is one of the first steps in the accounting cycle, where details of every financial transaction are recorded. A general ledger is the “master” document that summarizes the transactions and the company’s financial position.

Who is responsible for executing the accounting cycle?

The responsibility for executing the accounting cycle may vary slightly by company, but the onus typically falls on accounting professionals, whether individual bookkeepers or a larger accounting department. In some cases, different individuals may take responsibility for specific steps in the cycle.