What Is Perpetual Inventory?

Perpetual inventory is a continuous accounting practice that records inventory changes in real-time, without the need for physical inventory, so the book inventory accurately shows the real stock. Warehouses register perpetual inventory using input devices such as point of sale (POS) systems and scanners.

Perpetual inventory methods are increasingly being used in warehouses and the retail industry. With perpetual inventory, overstatements, also called phantom inventory, and missing inventory understatements can be kept to a minimum. Perpetual inventory is also a requirement for companies that use a material requirement planning (MRP) system for production.

Perpetual inventory has its own formula companies can use to calculate the ending inventory:

Ending Inventory = Beginning inventory + Receipts - Shipments

What Is a Perpetual Inventory System?

A perpetual inventory system is a program that continuously estimates your inventory based on your electronic records, not a physical inventory. This system starts with the baseline from a physical count and updates based on purchases made in and shipments made out.

Max Muller, president at Max Muller & Associates LLC and Author of “Essentials of Inventory Management”, says, “Perpetual inventory management systems keep track in real-time. It uses software to follow the rules, keep the system up-to-date, and it works great. I recommend doing 3D-counting, where you count cross-sections often enough to account for the whole over time. You could consider this perpetual, but it would need to be software-driven and follow the rules or do a variation.”

Inventory management software and processes allow for real-time updating of the inventory count. Often, this means employees use barcode scanners to record sales, purchases or returns at the moment they happen. Employees feed this information into a continually adjusted database that tracks each change. The automatic, or perpetual, updating of the inventory is what gives the system its name and differentiates it from the periodic approach.

In recent years, advances in inventory management software and the ability to integrate it with other business systems have made perpetual inventory a more practical and powerful option for many businesses. Additionally, cloud-based inventory management systems are often real-time, a key element of a perpetual inventory system.

The real value of perpetual inventory software comes from its ability to integrate with other business systems. For instance, real-time inventory information is vital for the financial and accounting teams. Inventory can make up a large part of your stated assets, so integrating inventory management with financial systems helps ensure accurate tax and regulatory reporting.

With access to real-time data, salespeople can provide accurate shipping information, manage expectations and provide a better customer experience that directly impacts your reputation. Integrating the inventory software with marketing systems provides that team with a current snapshot of what is selling and what is not. Marketers can set current information in the context of historical trends to understand customer behavior and position the company to meet anticipated customer demand.

What Is the Periodic Inventory System?

The periodic inventory system, also called the noncontinuous system, is a method companies use to account for their products. Based on a specified accounting period, periodic inventory does not keep a continuous tally of goods, purchases, sales and their associated costs.

This system works by the company accountant recording all purchases into a purchase account. The company then makes a count of the physical inventory and the accountant shifts any balance in the purchases into the inventory account. Next, the accountant adjusts the inventory account to match the cost of the ending inventory. A hallmark of a periodic system is the physical count of goods. This number is critical since the company does not track unique transactions. Whether the company performs it weekly, monthly, quarterly or annually, this inventory kicks off the records reconciliation.

In a periodic system, companies calculate Cost of Goods Sold (COGS) directly after a physical inventory, as they do not keep it on a rolling basis, nor do they update it continuously after each transaction. They do not keep an inventory account in a periodic system since they debit all purchases to a purchase account. Once the period is complete, the company adds the purchase account totals to the inventory’s beginning balance. Then, the company can also compute the cost of goods available for sale for the new period.

Perpetual vs. Periodic Inventory Systems

Perpetual and periodic systems require different tools and procedures around how employees document inventory, although they can be complementary. In a perpetual system, employees track the products all the time. In a periodic system, employees record products only at specified intervals.

Clearly, a perpetual system is more complex than periodic systems, as there are more records for the software and employees to maintain. Muller suggests, “When considering the system that you want to use, the fundamentals are the same — regardless of your approach. Even with the most advanced software, if there is a disconnect within the fundamental system, you are just speeding up your mistakes. You would make decisions about the system based on the nature of your products, their perishability and their physical handling: whether they were large or small and how much space they consume. The nature of the product also depends on how your company receives and stocks it. Some goods are unitized: They have small parts and are broken up into individual bins”.

Muller shares an example: “Years ago, I worked with a company that had no experience with frozen chicken. They would unload the chicken on the hot dock when they were checking it in. As a result, and even though it was still edible and safe, it became very unsightly after cooking. They learned to bring the stock into the freezer and then perform the check-in to their stock. They had to adjust their procedures and systems based on their product’s needs”.

Additional differences between the perpetual and periodic systems:

-

Updating Your Accounts:

In a perpetual system, updates to the general ledger and inventory ledger are continuous with every transaction. In a periodic system, updates to the general ledger only occur when there is a physical count, not based upon transaction.

-

Calculating Cost of Goods Sold (COGS):

Under a perpetual system, the software system maintains a running tally of transactions, so it is always able to provide COGS. A periodic inventory system calculates COGS after conducting a physical inventory, in a lump sum at the end of an accounting period. It is not possible to calculate a precise COGS before the end of the accounting period.

-

Record Transactions:

In a perpetual system, it is not possible to maintain records manually, because there could be thousands of transactions to track; a perpetual inventory system requires software. A periodic system, however, does not require software. You could manually track your inventory in a periodic inventory system.

-

Cycle Counting:

Cycle counting is when businesses count portions of their inventory with the intent of completing a full inventory over a time cycle. They do not count their entire inventory at once, but they do make small adjustments based on what they count. Also called sampling, businesses only use cycle counting in a perpetual system. They do not use cycle counting under a periodic inventory system because they are not able to set a baseline.

-

Recording Purchases:

In a perpetual system, you record purchases in the raw materials inventory account or the merchandise account. In a periodic system, you log purchases into the purchases asset account, without adding any unit-count information.

-

Performing Investigations:

In a perpetual system, transactions are available at a very detailed level. As such, you can conduct investigations into inventory-related errors easily. In a periodic system, these investigations are more complicated, because the system aggregates data at a high level. It is difficult to use this data to pinpoint errors in the process.

Even though GAAP standards say that either perpetual or periodic systems are appropriate for any business, each is more suited to different-sized organizations. Overall, perpetual systems are more suited to companies that have high sales volume or multiple retail locations because it is a timelier system. Periodic systems could hinder decision-making for these types of organizations. Periodic systems are more suitable for businesses not affected by slow inventory updates. These include emerging businesses, ones that offer services or companies that have low sales volume and easy-to-track inventory. Companies whose staff struggle with a perpetual system, for instance those with seasonal help, would also benefit from maintaining a periodic system. As their business grows, they can always institute perpetual inventory.

Not everyone agrees it’s wise to use periodic systems when you do not have a lot of products. Muller echoes the sentiment: “Periodic inventory systems are terrible. During the annual inventory, you go out and do a count. The chances are excellent that the paper life of the item is not going to match its real life (shelf count). So, you have a disconnect. If you only take inventory once a year, you do not know when the disconnect happened. There are so many issues between the beginning and end of a product’s life, there is no way to find the errors in a periodic system. We should be able to go back and find items shortly after problems happen to help improve inventory. Companies correct records and fix imbalances and move on — it is a snapshot in time. The problems will then reassert themselves almost immediately. For accounting purposes, though, it is important to perform this exercise, unless you have a mature cycle count program. Auditors will take a mature cycle count program as an annual physical count.”

The Advantages and Disadvantages of Perpetual Inventory

Perpetual inventory allows for more real-time inventory tracking, making it superior to other methods. However, the system requires consistent record-keeping and monitoring and is more expensive to set up than other methods.

Perpetual inventory can save you money in these ways:

- There is no need to close facilities regularly to perform physical inventories,

- Data from scanned barcodes help you forecast stock,

- You can account for all transactions, providing complete accountability of your products.

Even though perpetual inventory is superior, it is not perfect. While there is a constant, automatic product tracking system, there are still ways to lose positive inventory control.

The disadvantages of using perpetual inventory include:

- You must still perform an annual inventory to synchronize your data,

- You must input every transaction, which requires more consistent record-keeping and monitoring,

- Perpetual inventory systems have higher setup costs than other methods since they require software and training.

Who Uses a Perpetual Inventory System?

Large businesses with enormous quantities of inventory favor perpetual inventory systems. Perpetual inventory systems can also be ideal for emerging and small to medium-sized businesses looking for scalability.

Huge businesses have difficulty performing the cycle counts that are necessary for a periodic system. Further, an organization with several retail locations may find it is easier to control inventory when there’s a regularly updated database of products. Take, for example, a tool retailer that has a customer looking for a specific type of wrench, one that is rarely requested and sold. It has six locations in the local area. Using a perpetual system, it has real-time information about which site may have one in stock so the customer can go get his wrench quickly instead of driving from store to store looking for it.

Other businesses that need perpetual inventory include those that specialize in drop shipping, where the manufacturers ship directly to customers or those who specialize in trade and distribution. In these businesses, the inventory is always on the move. Also, there are constant returns and exchanges. Understanding which stock is available at a given time requires constant updates or a perpetual system.

When Would You Use a Perpetual Inventory System?

Perpetual inventory systems are helpful for those who always need to understand margins and profitability. A large business with many products or a company that wants the ability to scale an emerging business over time would use a perpetual inventory system.

Experts think perpetual inventory systems are the future, especially for product companies, as they are getting cheaper and more accessible for even small businesses to acquire and use. Muller explains, “The future of this industry is leaning towards more real-time identification of products and improving on everything having to do with transmitters in and on products. Really, these are automatic forms of identification. It doesn’t matter where you store it, you can find it”.

In a perpetual inventory system, software records changes into a sales revenue account each time the company makes a sale or purchases new inventory. This process of recording sales ensures that the accounting records reflect accurate balances in the accounts affected. The software also records the price charged. To record transactions in a perpetual system, you must know the selling price, the purchase price and the accounts affected. The selling price is what the customer pays for the item. The purchase price is the costs associated with the product, including the shipping, receiving and storage costs.

A typical journal entry would show which account the software debited and which account the software credited for each transaction.

Cash Sales Journal Entry

| Account | Debit | Credit |

|---|---|---|

| Cash | 300 | |

| Sales Revenue | 300 | 300 |

| Total | 300 | 300 |

How Is Inventory Tracked Under a Perpetual Inventory System?

A perpetual inventory system tracks goods by updating the product database when a transaction, such as a sale or a receipt, happens. Every product is assigned a tracking code, such as a barcode or RFID code, that distinguishes it, tracks its quantity, location and any other relevant details.

When new products enter a business, employees scan them (along with their details) into the computer system. Without a computerized inventory system, it would be difficult to track every transaction in a business manually, especially in companies that sell many products. For example, a retail big box store has thousands of products. Its supply chain provides deliveries daily of additional goods that the employees then scan into their database. If the product is new, the employee must add the details of the product when they initially scan it. That additional information includes a description, the product code or SKU and where customers will find it in the store. If the store already carries the product, this scan updates the quantity already in stock. When a customer buys one of these products, the database lists one less product in its count. At any time, the store manager can review the database to learn how much of that product is currently in stock and whether they need to order more.

This system depends on proper inventory control procedures. For example, the system needs to ensure that employees scan in any new inventory promptly. Physical counts to reconcile the database are rare, but necessary, since the true inventory count can become skewed over time with theft, loss or breakage.

Formulas in Perpetual Inventory

Inventory management formulas can tell you when to order more inventory, how much to order, the lead time needed before placing an order and how much stock you require to keep in safety.

Economic Order Quantity (EOQ) Formula

Economic Order Quantity (EOQ) considers how much it costs to store the goods alongside the actual cost of the goods. The results dictate the optimal amount of inventory to buy or make to minimize expenses.

EOQ Formula

| EOQ | = | √2DS/H, where, |

| D | = | Demand in units per year |

| S | = | Order cost per purchase |

| H | = | Holding cost per unit, per year |

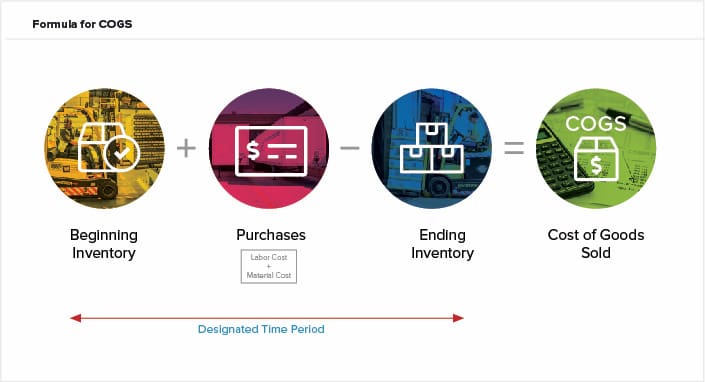

The Cost of Goods Sold (COGS)

When you sell products in a perpetual inventory system, the expense account increases and grows the costs of sales. Also called the cost of goods sold (COGS), the costs of sales are the direct expenses from the production of goods during a period. These costs include the labor and materials costs but leave off any distribution or sales costs.

COGS Formula

| COGS | = | BI + P - EI, where |

| BI | = | Beginning inventory |

| P | = | Purchases for the period |

| EI | = | Ending inventory |

Calculate the beginning inventory as whatever stock remains from the previous period if you do not have a true beginning inventory. The accounting period can be in months, quarters or a calendar year. The COGS in a perpetual system is rolling and recalculated after each transaction, but you can use the COGS formula to calculate it for a period.

Let’s say Ava, a product manager, wants to know if she is pricing generic Acetaminophen high enough to leave a healthy profit margin. COGS is an effective formula for setting prices on manufactured goods. If she calculates the COGS as $10 per 100-capsule bottle, she will need to price each bottle higher than $10 so her company can comfortably turn a profit.

Ava’s business uses the calendar year (starting on Jan. 1 and ending Dec. 31) for recording inventory. The company accountant valued the Jan. 1 beginning inventory of generic Acetaminophen at $49,000, or 4,900 bottles. During the year, generic Acetaminophen costs the company $40,000 for materials and labor. On Dec. 31, the company accountants valued the ending inventory at $30,000.

COGS Formula

| BI | = | $49,000 |

| P | = | $40,000 |

| EI | = | $30,000 |

| COGS | = | $49,000 + $40,000 - $30,000 |

| = | $59,000 |

Gross Profit

Ava can use the figure she calculated for COGS to make decisions about the product. For example, she can use COGS to calculate the gross profit her company made from generic Acetaminophen. Gross profit is simply the product revenue minus COGS, or

Gross Profit

| Gross Profit | = | Revenue - COGS |

| If the revenue for generic Acetaminophen was $113,000 last year, the gross income from it was: | ||

| Gross Profit | = | $113,000 - $59,000 |

| = | $54,000 | |

If Ava needs to raise the product cost to make more profit or lower the cost to make it more competitive in the marketplace, she now knows how it will affect her company’s bottom line.

Gross Profit Method

In a perpetual system, you will sometimes need to estimate the amount of ending inventory for a period when preparing financial statements or if stock was destroyed. To calculate this estimate, start with the beginning inventory and cost of purchases during the period.

Let’s say that you need to estimate the ending inventory from the current month. The values you need to know to calculate this are the gross profit as a percentage of sales, the total sales for the period, the beginning inventory for the period and purchases for the period. As shown below in the ledger, estimate the relative percentages of both COGS and gross profit for your total sales. From there, solve for the cost of goods sold, and then fill in the known values minus the COGS figure. The result should provide an ending inventory estimate and how much to claim as the bottom-line figure for this period.

Ledger to Calculate Gross Profit

| Estimate | Figures | |

|---|---|---|

| Sales | 100% | $156,000.00 |

| Cost of Goods Sold (COGS) | 55% | $85,800.00 |

| Gross Profit | 45% | $70,200.00 |

| Begin Inventory | $45,000.00 | |

| Purchases | $67,800.00 | |

| Cost of Goods Available for Sale | $112,000.00 | |

| Minus COGS | $85,800.00 | |

| Estimated Ending Inventory | $26,200.00 | |

What Is FIFO Perpetual Inventory Method?

FIFO (first-in, first-out) is a cost flow assumption that businesses use to value their stock where the first items placed in inventory are the first items sold. So the inventory left at the end of the period is the most recently purchased or produced.

A cost flow assumption is an inventory accounting method that uses the original value of products from the beginning inventory of a period and purchases of new inventory during that period to calculate the value of the ending inventory and the cost of goods sold. The three cost flow assumptions that businesses use for this are FIFO, LIFO, and the Weighted Average Cost (WAC).

In a perpetual system, the inventory account changes with every transaction. Companies debit their inventory account with the cost of the merchandise each time they purchase or produce inventory and when they sell inventory to customers. The perpetual inventory software updates the inventory account with each transaction. With each sale, the software also updates the COGS account with a debit. As an example, see the sample FIFO perpetual inventory card below. The retail sales for this product in this company were $25,000 from Jan. 1, 2019 to Jan. 15, 2019.

Inventory Card

| Purchases | Sales | Balance | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Date | Activity | Units | Unit Cost | Total Cost | Units | Unit Cost | Total Cost | Units | Unit Cost | Total Cost |

| 1/1/2019 | Begin Inventory | 600 | 5.00 | 3,000.00 | ||||||

| 1/3/2019 | Sale | 400 | 5.00 | 2,000.00 | 200 | 5.00 | 1,000.00 | |||

| 1/4/2019 | Purchase | 1,600 | 6.00 | 9,600.00 | 200 1,600 |

5.00 6.00 |

1,000.00 9,600.00 10,600.00 |

|||

| 1/7/2019 | Sale | 200 800 |

5.00 6.00 |

1,000.00 4,800.00 5,800.00 |

800 | 6.00 | 4,800.00 | |||

| 1/10/2019 | Purchase | 1,000 | 6.00 | 6,500.00 | 800 1,100 |

6.00 5.50 |

4,800.00 6,500.00 11,300.00 |

|||

| 1/15/2019 | Sale | 600 | 6.00 | 3,600.00 | 200 1,000 |

6.00 6.50 |

1,200.00 6,500.00 7,700.00 |

|||

This card shows the starting inventory, sales, purchases, prices and balances. Under a perpetual system, inventory records for this product are continually changing. When the company sells merchandise, the perpetual software records two transactions. First, the software credits the sales account and debits the accounts receivable or cash. Second, the software debits the COGS for the merchandise and credits the inventory account. In a periodic system, accounting does not perform this second step.

From the perpetual FIFO inventory card above, you can calculate the cost of ending inventory as the total cost balance from the last row, or $7,700. Calculate COGS by adding the total cost column in the sales category, or $2,000 + 5,800 + $3,600 = $11,400. Finally, you can calculate the gross profit as the total retail sales minus the costs of goods sold, or $25,000 - $11,400 = $13,600.

A company may prefer using a FIFO system when it’s trying to show its largest possible profit on its financial statements for investors, lenders and stakeholders. A FIFO system shows a lower COGS expense and a higher net income.

What Is LIFO Perpetual Inventory Method?

LIFO (last-in, first-out) is a cost flow assumption that businesses use to value their stock where the last items placed in inventory are the first items sold. So the remaining inventory at the end of the period is the oldest purchased or produced. In a perpetual LIFO system, the last costs available at the time of the sale are the first that software moves from the inventory account and debits from the COGS account. See the example LIFO perpetual inventory card below to get an idea of how it works. The retail sales for this product in this company were $25,000 from Jan. 1, 2019 to Jan. 15, 2019.

From the perpetual LIFO inventory card above, you can calculate the cost of ending inventory as the total cost balance from the last row, or $7,200. You can calculate COGS by adding the total cost column in the sales category, or $2,000 + 6,000 + $3,900 = $11,900. Finally, you can calculate the gross profit as the total retail sales minus the costs of goods sold, or $25,000 - $11,900 = $13,100.

During periods of inflation, a LIFO system may be more appropriate for companies that do not wish to pay as much in taxes, because it will show a higher COGS expense and a lower net income. Therefore, your company has a lower tax liability in a LIFO system, because businesses get taxed on profit. The Internal Revenue Service allows companies to use LIFO in their tax accounting, even when they use FIFO in their financial statements.

What Is the Weighted Average Cost Perpetual Inventory Method?

The Weighted Average Cost (WAC) is the cost flow assumption businesses use to value their inventory. WAC is the average cost of goods sold for all the inventory. Also called the moving average cost method, accountants perform this differently in a perpetual system as compared to a periodic system.

The goal of using the WAC is to give every inventory item a standard average price when you make a sale or purchase. In a perpetual system, you would not calculate the WAC using a formula for a specific period. You can use WAC to calculate an average unit cost, COGS for a period and ending inventory for a period. For example, Ava wants to figure out the average cost to assign for Acetone repackaged in her company’s warehouse. She will use this information to calculate the ending inventory and COGS for the period. Her company uses a perpetual system. See the ledger below for transactions for Acetone in Jan. using a weighted average. This ledger mimics that of a software ledger in a perpetual system.

January Perpetual Ledger of Sales and Purchases for Acetone

| Number of Units | Actual Unit Cost | Total Actual Cost | |

|---|---|---|---|

| Beginning Inventory | 300 | $10.00 | $3,000 |

| Purchase | 200 | $15.00 | $3,000 |

| 500 | $12.00 | $6,000 | |

| Sale | 300 | $12.00 | $3,600 (COGS) |

| 200 | $12.00 | $2,400 | |

| Purchase | 100 | $17.00 | $1,700 |

| 300 | $13.67 | $4,100 | |

| Sale | 250 | $13.67 | $3,418 (COGS) |

| 50 | $13.67 | $648 | |

| Purchase | 300 | $20.00 | $6,000 |

| Ending Inventory | 350 | $6,684 |

Notice the ledger above calculates the actual unit costs (in red) as a dividend of the number of units and total actual cost. The ledger adds the beginning inventory to the purchased inventory (500 units). The ledger then adds the beginning inventory cost to the purchased inventory cost ($6,000) to come up with a new unit cost of $12.00 for future sales. The next entry shows a sale made with this calculated unit cost. This sale enables you to calculate the COGS for this transaction. The ending inventory is just an arbitrary stopping point based on the period you are reviewing. For this ledger’s period, you can also calculate the total COGS as $3,600 + $3,418 = $7,018.

NetSuite Can Help Provide Visibility Into Your Inventory

Properly managing inventory can make or break a business, and having insight into your stock through the perpetual inventory method is crucial to success. Regardless of the type of inventory control process you choose, decision-makers know they need the right tools in place so they can manage their inventory effectively. NetSuite offers a suite of native tools for tracking inventory in multiple locations, determining reorder points and managing safety stock and cycle counts. Find the right balance between demand and supply across your entire organization with the demand planning and distribution requirements planning features.

Learn more about how you can manage inventory automatically, reduce handling costs and increase cash flow with NetSuite.