Future accountants, get ready: July 2021 will bring significant modifications to the CPA Exam that reflect changes to the accounting profession as a whole. While the test's content has always been dynamic and subject to regular updates by the American Institute of Certified Public Accountants (AICPA), the changes taking effect in July are notable for their focus on technology.

In this article, we'll cover the changes, their implications, the future of the CPA role and tips for keeping up-to-date in this rapidly-changing field.

Key Takeaways

- In July 2021, the CPA Exam will change to reflect the new, technology-focused reality of the profession.

- The exam will test more on concepts like IT controls, automation and business processes — and less on topics like IFRS and U.S. GAAP.

- With these changes fast-approaching — and an even bigger overhaul coming in 2024 — current and prospective CPAs likely need to hone skills like strategic thinking, data analysis and communication that are increasingly in demand.

Summary of 2021 CPA Exam Changes

Early in 2020, the AICPA announced upcoming changes to its CPA Exam Blueprint, which outlines exam sections by topic, number of questions and more. The changes are a result of the AICPA’s 2019 Practice Analysis, which examined the duties and expected skills of newly-licensed CPAs in the field.

“The focus of this Practice Analysis was to assess the impact of analytics and technology on the work that newly-licensed CPAs perform,” Bukowski said on the NetSuite Podcast. “We also reexamined the core accounting competencies all CPAs must possess to protect the public interest.”

Listen to Bukowski’s full interview for more insights:

After its Practice Analysis, the AICPA published a draft of the proposed changes to the exam with an invitation to comment. It received more than 180 responses from CPA firms and individual accountants across the country, which further informed the exam changes.

The CPA Exam is composed of four sections:

- Auditing and Attestation (AUD)

- Business Environment and Concepts (BEC)

- Financial Accounting and Reporting (FAR)

- Regulation (REG)

The majority of the changes are to the AUD and BEC sections. The major themes of the changes, according to the AICPA, are:

- Understanding of business processes from inception to completion, including automated aspects, risk identification and internal control mapping

- The need for a digital and data-driven mindset and the use of data analytics

- Increased reliance on System and Organization Controls for Service Organizations: Internal Control Over Financial Reporting (SOC 1) reports

Additionally, the AICPA will remove some topics that aren’t considered necessary for newly-licensed CPAs (nlCPAs) to know, most notably the differences between the U.S. Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS).

-

Understanding of Businesses Processes

The first major change to the CPA exam requires that nlCPAs “understand the business including its operations, information systems, underlying business processes, information and data flows, and risks and related internal controls,” according to the AICPA.

In the AUD section, this requires a knowledge of “business processes and transactions that flow through them,” including IT systems, IT controls and manual controls. The revised AUD section will also include tasks on the completeness and accuracy of data to be used as audit evidence. In this regard, the AUD section will generally increase its focus on risk assessment and the testing of internal controls.

The BEC section will see more concentration on governance and the design of internal controls. The section will include questions on “business processes and transaction-level risks and controls” and the technology enabling these processes.

As mentioned, these changes reflect what’s going on in the accounting field.

“Newly-licensed CPAs need to have a better understanding of business processes, internal controls, and accounting information systems that they work with every day, not only from the management side [but] also from client and audit side,” said Bukowski. “Those really were the big themes we focused on [when making changes to the exam]. That’s what we heard loud and clear from the last Practice Analysis.”

-

Digital Mindset and Data Analytics

The AICPA’s Practice Analysis also revealed the need for “a digital and data-driven mindset and the use of data analytics” among nlCPAs.

To reflect this, the exam’s AUD section will now test on audit data analytics via “small case studies incorporating basic data knowledge, as well as interpreting the results of analytic procedures.” nlCPAs will be expected to analyze and identify anomalies in “the results of an audit data analytic procedure” and explain how to use “automated tools and audit data analytics in audit sampling.”

The BEC section will focus more on working directly with data, including questions on data management and relationships. Specifically, it will look at “topics related to data governance, and extracting, transforming and loading data and visualizations.”

-

Increased Reliance on SOC 1 Reports

SOC reports examine the controls that services organizations use to protect their clients’ assets. SOC 1 reports, specifically, deal with outsourced services that are relevant to a company’s financial reporting. Businesses are increasingly outsourcing information systems to third parties, as well as storing data in the cloud, so SOC 1 reports have come into focus as important for auditors.

As a result, the CPA Exam’s AUD section will test on the difference between SOC 1 and SOC 2 reports and ask candidates to examine these reports’ effects on controls and the testing of controls.

The BEC section will highlight this reliance as well, covering SOC 1 reports “from the user entity’s perspective, including consideration of the period covered and any complementary user entity controls.”

Content Removal

The CPA Exam will also bid farewell to several concepts. Perhaps the most significant removal will be questions on the differences between the U.S. GAAP and IFRS accounting standards. These were dubbed too “client-specific,” particularly since IFRS has not been adopted for U.S. public companies as had been expected when it was initially included in the exam.

Other notable omissions include niche topics like the alternative minimum tax, trusts and estate taxation in the REG section; and defined benefit pension plans and derivative journal entries in the FAR section.

2021 Changes to the CPA Exam

| Exam Section | Change |

|---|---|

| AUD | More testing of “business processes and transactions that run through them,” including IT systems, IT controls and manual controls |

| AUD | More tasks on the completeness and accuracy of data to be used as audit evidence |

| AUD | A new section on audit data analytics and automated tools |

| AUD | Tests on the differences between SOC 1 and SOC 2 reports and these reports’ effects on controls and the testing of controls |

| BEC | New content on businesses processes and transaction-level risks and controls, including technology that facilitates them |

| BEC | More focus on data governance and relationships; how to extract and transform data |

| BEC | More questions on SOC 1 reports from the entity’s view, including the period covered and complementary user entity controls |

| FAR | Removal of questions on differences between IFRS and U.S. GAAP |

| FAR | Removal of questions on defined benefit pension plans and derivative journal entries |

| REG | Removal of questions on the alternative minimum tax, estate taxation and trusts |

The Continuing CPA Exam Evolution

Changes to the CPA exam won’t stop in 2021. Already, the AICPA has begun its “CPA Evolution” project in a joint effort with the National Association of State Boards of Accountancy (NASBA). The project involves implementing a new CPA licensure model and then launching a new CPA Exam — yes, a completely revamped exam apart from the changes to be introduced this summer.

“The main focus of the CPA Evolution project is to transform the CPA licensure model to recognize the rapidly-changing skills and competencies in accounting and the different skills that are required of today’s CPA,” said Bukowski.

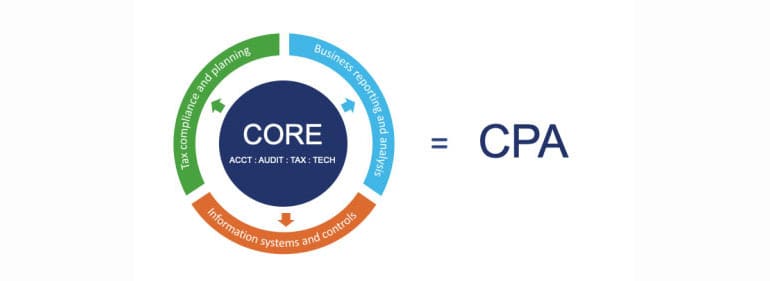

The new licensure will follow a “core + discipline” model. On that CPA Exam — again, not to come for several years from now — candidates will test in three core sections: accounting, auditing and tax. They’ll also test in a fourth discipline, which they will be able to choose:

- Business reporting and analysis

- Information systems and controls

- Tax compliance and planning

Bukowski said she sees this new model as enhancing public protection by giving nlCPAs a deeper knowledge of some of the disciplines involved in today’s work. She estimates that an overview of these future changes will be released in January 2023, and the entirely new CPA Exam will launch in January 2024.

Under the future licensure model, candidates will be required to exhibit core skills in accounting, auditing, tax and technology — and more in-depth skills in an additional discipline of their choosing.

CPA Exam Resources

Learn more about the 2021 CPA Exam changes and the CPA Evolution project:

The 2019 AICPA Practice Analysis

Provides research conducted by the AICPA in 2019 that delves into the state of

the profession, specifically the knowledge and skills most relevant to the

work.

AICPA Practice Analysis respondents and comments

Contains the list of respondents to the AICPA’s exposure draft on the

proposed changes to the CPA Exam. It also contains the full text of the comments

received.

AICPA CPA Exam Blueprint

Outlines the CPA Exam and the minimum level of knowledge and skills a CPA

candidate must have to qualify for initial licensure.

Overview of the CPA Evolution project by the AICPA

and NASBA

Summarizes the CPA Evolution initiative that will go live in 2024, including the

new model for licensure and the new CPA Exam.

The Accounting Profession’s Reaction to CPA Exam Changes

The accounting profession has evolved greatly since its ancient origins, particularly during the Renaissance with the publications of Luca Pacioli. In a sense, it’s approaching another renaissance — albeit more niche in nature — which the 2021 CPA Exam changes reflect. Overall, the accounting world says it’s about time.

“If you think about it, this progression took place years ago... when the large firms went to paperless audits,” said Becker’s Ken Koskay. “And the current CPA Exam [doesn’t reflect that]. So, in many ways, I think we’re a little bit behind the eight ball as a profession. But the good news is we’re catching up very quickly.”

Michael Parrinello, CPA and partner at The Bonadio Group, concurs.

“I think the [2021] change in the CPA Exam is an acknowledgement of the shift in the profession,” he said. “Technology has driven us to operate differently, think about operating differently, and plan for the next five years differently. I think the CPA Exam itself represents some of the critical thinking and skill sets that people in a professional, data-driven world will ultimately need, [which] is a net positive for us.”

The exam’s evolution will also “eventually raise the overall quality of the CPA credential across the board by not only equipping new licensees with a more relevant skill set but also, and perhaps more importantly, raising the business community’s awareness and expectations of what a CPA can do,” said Colin Smith, an independent CPA and founder of the CPA Exam Maven site.

Elevating the CPA credential is critical right now. CPA firms’ hiring of accounting graduates has declined 30% in recent years, according to Accounting Today. And the percentage of Fortune 1000 CFOs who are CPAs fell to 36% in 2019 to an all-time low, the Wall Street Journal reported.

“I noticed in working with our largest global customers that their hiring began to change roughly five years ago,” said Koskay. “Many of those firms are hiring fewer true accounting graduates. Instead, they’re hiring accounting, data sciences and IT graduates. All of those work on audits because you need that technology acumen to be able to apply AI; you need [data sciences proficiency] to apply data analytics to big data and harness large data sets. Ultimately, those skillsets are not always found in accounting graduates.”

Needed Skills for the “CPA of the Future”

If you search “changing role of the CFO,” you’ll get an overwhelming amount of results touting CFOs’ new responsibilities in technology, strategy and leadership. The CPA role is similarly changing from number-cruncher to strategic thinker. In order for CPAs to continue delivering value in the age of technology, they must become insights-focused strategic advisors.

For years, technology and automation have nipped at the accounting and auditing profession’s proverbial heels. Let’s play a little game: Do you need a CPA to do the following tasks?

- Bank reconciliations

- Auditing expense submissions

- Invoice categorization

- Data entry

- Verifying and processing invoices

- Fraud detection

If you answered “no” to all of the above, then you’re correct. CPAs’ value is transitioning — and will continue to shift for the foreseeable future — to the insights, judgment and business acumen they can bring to the table.

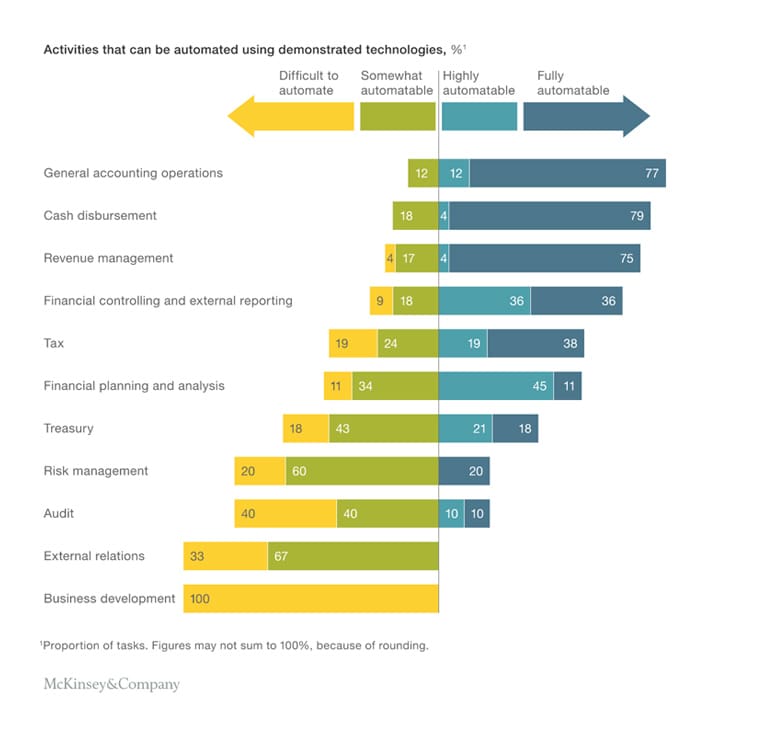

Research from McKinsey shows that many tasks, particularly those in general accounting operations, can be fully automated.

As compliance engagements decline due to the rise of automation and AI, many CPAs are finding success serving their clients in this advisory capacity — a trend that burgeoned during the pandemic. In an October 2020 survey by the Thomson Reuters Institute, 95% of tax professionals said they believe their clients want business advisory services. Many noted they were already in a de facto business advisor role due to the pandemic. CPAs found themselves guiding clients through the complicated process of getting financial relief, shedding light on the Paycheck Protection Program and Employee Retention Credit. They also helped clients navigate payroll issues like workers compensation insurance, unemployment insurance and payroll taxes as employees worked remotely, sometimes in different states.

“As a CPA, you truly are that trusted advisor,” said Koskay. “There’s a level of conservatism and levelheadness [among CPAs] that can create that trust factor.”

That need for a trusted advisor with a very particular set of skills will likely persist. And research suggests several of those “future CPA skills” are already in high demand:

Strategic Thinking

As technology takes over the manual, repetitive activities that used to be common for CPAs, clients desire strategic thinking and insights from these professionals.

“Clients in general [are] looking to you less for the answer and more for the possibility,” said Parrinello. “What are alternative possibilities, a range of solutions or opportunities that we as accountants glean from their financial information?”

Instead of being mired in numbers, CPAs are now expected — and will increasingly be expected — to have a broader strategic vision, offering high-level advice and critical thinking relevant to today’s economy, particularly as businesses pursue recovery, growth and expansion.

Data Adeptness

The CPA Exam’s shift toward data-driven mindsets and data analytics reflects demand in the marketplace. Many businesses are looking for CPAs capable of using data analytics for practices like continuous monitoring and auditing. And forget about data samples. Now, technology-powered CPAs are often expected to analyze full data sets vs. auditing only samples. The results: higher-quality audit evidence, fewer repetitive tasks and better correlation of audit tasks to risks and assertions.

This focus on strategic interpretation of data means that firms will look for entry-level CPAs that can do higher-level work formerly reserved for more senior accountants.

“I think [entry-level skills] are going to revolve around data analytics and data analysis, because it’s not like the way we used to do audits and tax work,” said Koskay. “Technology will do most of the rote tasks that were once done by entry-level professionals. They will now need to be able to apply the software applications and interpret the results. That type of work used to be done [only] by more senior-level professionals.”

These data skills inform the aforementioned strategic thinking. Effective data analysis — particularly through data exploration, data visualization and predictive modeling — during an engagement can allow CPAs to provide actionable intelligence and advice to their clients.

“Technology will do most of the rote tasks that were once done by entry-level professionals. They will now need to be able to apply the software applications and interpret the results. That type of work used to be done [only] by more senior-level professionals.”

- Ken Koskay, VP & head of global sales & business development, Becker

Ability to Partner With Technology

Technology can be a valuable partner to CPAs. Clients want to see more of that partnership from their accounting firms — and not just from the Big Four. Smaller firms with smaller clients have already started using more technology tools and are looking for CPAs able to use them.

“Even though smaller firms might not be on the leading edge of technology, they still use technology extensively,” said Koskay. “They need their staff to be able to understand these tools and implement them. For instance, a regional or community bank, which a mid-tier or smaller [accounting] firm could [work with], can have pretty large datasets. And so [software tools are] almost ubiquitous.”

Many of The Bonadio Group’s small to mid-sized clients pushed digital advancements in the past year, Parrinello said. Now, the task is to use the new tools while still delivering the service element.

“It’s not just embracing and implementing technology,” he added. “It’s, ‘How are we going to use technology as accounting professionals to help translate trends and opportunities in our clients’ businesses?’ and 'How is technology going to allow me to better deliver to those who consume my service?'”

CPAs who partner with technology effectively will find themselves freed of traditional, repetitive tasks like data entry and bank reconciliations and afforded time for differentiating, value-added activities like interpreting recommendations from cognitive tools, evaluating analytics, and providing clients with decision-making insights. In other words, CPAs will identify opportunities for growth or proactively recommend course corrections so businesses can forestall problems. And their firms will continue to evolve from compliance-focused accounting firms to problem-solving consulting and advisory firms. Koskay said he envisions a specific emphasis on technology consulting.

Soft Skills

Technology can’t yet replace the expertise and awareness of client needs which comes from personal interaction.

“I think those people in our firm who can connect — and not just maintain relationships but develop relationships, partnerships and pieces of the business — tend to be more successful,” said Parrinnello. “I think to the extent that we can foster more human interaction, the better off we will be maintaining relevance.”

As CPAs take on their advisory role, communication and relationship-building capabilities are crucial. CPAs will increasingly need to explain data to clients, help clients understand the numbers and expound their interpretations.

“I think data and technology are the big skills needed, but also the ability to communicate well, which is not something you always think about when you talk about an accounting major,” said Koskay. “The ability to communicate and present well is critical across both written and verbal platforms.”

Specialized Knowledge and Skills

Considering the expanding skills and knowledge required of CPAs — and the CPA Exam’s incorporation of those “disciplines” for candidates to choose from in 2024 — Koskay said he sees specialization as a trend.

“If you think about what we’re doing now in the CPA profession, it’s about taking on more concentrated skills,” he added. “I think what’s going to be necessary in terms of skill sets is, instead of going a mile wide and an inch deep, you’re going to need to go an inch wide and a mile deep. That’s where firms are going.”

Accordingly, Becker has started to create content in more specialized areas, he said.

“If you think about what we’re doing now in the CPA profession, it’s about taking on more concentrated skills. Instead of going a mile wide and an inch deep, you’re going to need to go an inch wide and a mile deep.”

- Ken Koskay, VP & head of global sales & business development, Becker

Continuing CPA Education

Koskay made it clear: The CPA profession will not survive without upskilling. This carries implications for CPAs that are already practicing.

“As a freelance consultant, my success will ultimately come down to the number of problems I can solve for my clients,” said Smith. “For example, if I can handle all of the accounting for a major acquisition and help my client merge their accounting information systems together, I know I’ll be in much higher demand in the marketplace than if I were only able to handle the accounting side of things.”

Smith is currently honing his data analytics and visualization skills, as well as practicing using various business intelligence software tools. With the massive amounts of data available to organizations, he said he already sees huge demand for these skills and expects that demand to grow.

Professional education firms like Becker are responding, too. When Koskay started at Becker nearly five years ago, the firm had around 125 continuing education courses. Now, it has over 700 due to demand for upskilling resources, especially in the realms of specialized technology and soft skills.

Upskilling Resources for CPAs

-

AICPA:

The AICPA provides webcasts, courses, research publications, credentials and exams. It also hosts virtual and on-site conferences in conjunction with the Chartered Institute of Management Accountants.

-

Becker:

An exam preparation company, Becker also offers a continuing education repository — with subscription or ad hoc pricing — for CPAs wishing to earn CPE credit and learn more about the profession.

-

Checkpoint Learning:

Run by Thomson Reuters, Checkpoint Learning offers live events and on-demand courses for individuals and teams.

-

NASBA:

NASBA’s site offers news, publications and meetings and events information. It also hosts a registry of approved CPE courses.

-

LinkedIn Learning:

The video learning platform offers numerous trainings in accounting skills, software and other technologies.

-

Udemy:

The massive course provider, which many companies use to upskill their workforces, offers a variety of accounting-related courses, notably in data analytics and data visualization.

Not all upskilling has to be formal. For example, Parrinello recommends that seasoned CPAs team up with new ones on the job — and thereby pick up the younger generation’s technology skills. The Bonadio Group does this via a pseudo-buddy system on projects.

“Where I see a benefit is when [seasoned and new CPAs] work side-by-side,” said Parrinello. “Someone who [has been a CPA longer] can bring the more conceptual business accounting mindset, and the younger professional can show them the tools available today. That can help them more efficiently, and maybe more precisely, execute on client service.”

The Bottom Line

The idea of changing the accounting profession to keep it viable may be intimidating, but it’s also exciting. The future CPA won’t be bogged down by repetitive, manual tasks. Instead, they will focus on strategy and bring even deeper value to their clients.

The CPA Exam is changing to reflect this, and experienced CPAs are upskilling in response to this. And for the accounting profession as a whole, this is more renaissance than doomsday. Despite their varied backgrounds, our sources reached consensus on these shifts: They represent an opportunity.

Sources

For this article, we spoke with:

Jenn Bukowski: CPA and senior technical manager of test development

at the AICPA

The AICPA is the world's largest member association representing the accounting

profession.

Ken Koskay: VP and head of global sales and business development at

Becker

Becker is a professional education company offering CPA exam preparation and

continuing professional education.

Michael Parrinello: CPA and partner at The Bonadio Group

The Bonadio Group is a mid-sized accounting firm with offices in New York, Texas

and Vermont, named a Top 100 Public Accounting Firm in 2020 by Inside Public

Accounting.

Colin Smith: CPA and founder of CPA Exam Maven

Smith is an independent CPA and founder of CPA Exam Maven, a site dedicated to

helping candidates prepare for the CPA exam.