Ending inventory, defined as the value of sellable inventory remaining at the end of an accounting period, is a crucial metric for any business that sells goods. Accurately assessing ending inventory is essential for a clear picture of the company’s assets, profit and tax liability. Businesses using inventory management software don’t need to actually calculate ending inventory, since they have a constant view of it, but they will report inventory level for accounting purposes. Companies can use a variety of methods to calculate ending inventory, the choice of which affects both the company’s balance sheet and its income statement.

What Is Ending Inventory (or Closing Inventory)?

Ending inventory, also known as closing inventory, is the value of goods that a company has available for sale at the end of a given accounting period. Calculating ending inventory is important for businesses in virtually every industry. Understanding how much stock is left at the end of an accounting period helps companies get a better picture of their current assets and gross profit, whether their inventory management systems are accurate and whether they should adjust their ordering and production to align more closely with demand.

What Is Inventory Value?

A critical figure for understanding a business’s financial health, inventory value refers to the monetary worth of a company’s inventory at a specific point in time. This includes all products that are ready for sale, raw materials and goods in production. Accurate inventory valuation helps companies assess their cost of goods sold (COGS) and gross profit. Different inventory management methods, such as first in, first out (FIFO), last-in, first-out (LIFO) and weighted average cost (WAC), can influence the final inventory value, impacting financial statements and tax calculations.

Key Takeaways

- Ending inventory measures the value of goods a business has available to sell at the end of a given accounting period.

- The method used to calculate ending inventory has implications for the company’s balance sheet, profit and tax liability.

- Many companies use the first in, first out (FIFO) or weighted average cost (WAC) methods for accuracy and simplicity.

- The gross profit and retail methods can be used to estimate ending inventory when accurate inventory counts are not feasible.

- Inventory management software can automate inventory tracking and simplify the calculation of ending inventory.

Ending Inventory Explained

To calculate ending inventory, businesses need to track the number of inventory items they have. This tracking can be performed automatically using inventory management software and when necessary confirm those numbers using physical inventory counts. Companies then choose an appropriate method to assign a value to those items in order to calculate the total value of ending inventory. Where an accurate count of inventory items is not feasible, it may be possible to estimate ending inventory from other business data.

Why Is Ending Inventory Important?

Tracking ending inventory is important for business management, accounting and tax purposes. Ending inventory can be among the company’s biggest assets, so it’s important to ensure it is accurately tracked and valued. The choice of inventory valuation method also affects the company’s COGS, which, in turn, has an impact on the company’s gross and net profit and resulting tax liability. Ending inventory has implications for business strategy and planning. In the retail sector, accurately assessing ending inventory as part of a broader inventory management process may be critical to a company’s survival. Efficient inventory management helps companies ensure they have enough goods to supply customers and set appropriate pricing and sales strategies.

How Is Ending Inventory Used?

Determining the value of ending inventory helps companies get a clear picture of their financial health. The calculation of ending inventory affects both the company’s balance sheet and income statement, which are two of the primary financial statements closely scrutinized by executives, lenders and investors. Ending inventory is recorded as a current asset on the balance sheet at the end of each period; for retailers and some other businesses, it is often the most valuable asset.

The cost of inventory that’s sold during each period is subtracted from ending inventory and added to the company’s COGS. This directly affects the gross profit reported on the income statement, which is calculated by subtracting COGS from net sales revenue. Ending inventory valuation therefore affects the amount of income tax the company needs to pay for the period. An accurate measure of ending inventory is important not only for the current period but also for future periods because each period’s ending inventory is used as the beginning inventory for the next period.

Companies can also compare their calculated ending inventory value with actual physical inventory to identify potential problems, such as inventory shrinkage.

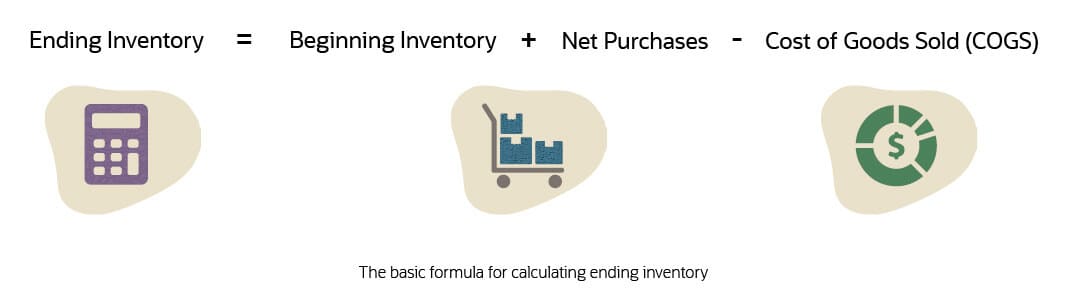

How to Calculate Ending Inventory

The basic method for calculating ending inventory is straightforward. You simply take the beginning inventory at the outset of the current accounting period, add the cost of new purchases and subtract the cost of goods sold (COGS).

Ending inventory formula: The basic ending inventory formula is shown below. Although the formula is simple, the way in which a business calculates COGS plays a major role in the ending inventory value.

Ending inventory beginning inventory + net purchases – cost of goods sold (COGS)

- Beginning inventory is the value of inventory at the start of the period. It is equal to the ending inventory value from the previous accounting period.

- Net purchases is the cost of any items that a company has purchased and added to its inventory during the accounting period.

- COGS is the cost of manufacturing and/or purchasing the finished goods that were sold during the period.

Ending Inventory Methods

There are multiple methods for calculating ending inventory, each with its own advantages and disadvantages. All valuation methods use the basic ending inventory calculation formula shown above. Many companies use FIFO or WAC as they tend to be more accurate for their purposes and may be simpler to apply.

First in, first out (FIFO). The FIFO method assumes that items are sold in the order they were ordered. It therefore calculates COGS — the cost of the goods that were sold during the period — based on the inventory that was purchased earliest. This approach follows the way many companies actually operate, selling older items first to make space for newer goods in their inventory. Because the prices of materials and other inventory tend to increase over time, this method often produces a lower COGS and higher gross profit than other methods of calculating ending inventory. The higher profit can mean a greater income tax burden for the current period.

| FIFO PROS | FIFO CONS |

|---|---|

|

|

Last in, first out (LIFO). LIFO assumes that the most recently purchased inventory was sold first. When prices are rising, LIFO increases COGS and therefore results in a lower gross profit and income tax bill for the current period. The higher COGS also results in a lower ending inventory value. While LIFO is allowed under U.S. Generally Accepted Accounting Principles, it is not allowed under International Financial Reporting Standards (IFRS). In other words, it can be used in the U.S. but not in many other countries.

| LIFO PROS | LIFO CONS |

|---|---|

|

|

Weighted average cost (WAC). With this method, a business simply averages all inventory costs to calculate COGS and ending inventory. WAC is particularly useful when a company sells many identical items. In these cases, it simplifies calculation of ending inventory because there’s no need to track the cost of individual inventory purchases. It’s less useful when the company sells many different products with widely differing prices and costs.

| WAC PROS | WAC CONS |

|---|---|

|

|

Gross profit. The gross profit method is used to estimate ending inventory value in situations where it’s not possible or desirable to measure the actual number of inventory items that the company holds. It can be used to get a rough snapshot of inventory value during the interval between physical inventory counts, or to estimate the inventory remaining after losses due to fire, flood or theft.

This method uses the company’s expected gross profit margin for the current period as a starting point for estimating COGS and ending inventory. Companies often use their historical gross profit margin as a guideline for their current expected gross margin. A company’s gross profit margin is its gross profit expressed as a percentage of net sales.

Here are the steps to calculate gross profit:

- Multiply the net sales during the current period by (1 - expected gross profit margin) to obtain an estimate of COGS.

- Apply the standard inventory valuation formula: Add up the period’s beginning inventory and the cost of all further inventory purchases to date, and subtract the estimated COGS to obtain the ending inventory.

| GROSS PROFIT PROS | GROSS PROFIT CONS |

|---|---|

|

|

Retail method. The retail method is used by retailers to estimate the value of their merchandise at a specific point in time. Retailers may be likely to use this method if their business involves selling large volumes of low-cost items, making accurate inventory counts difficult. It uses the cost-to-retail ratio, which is the ratio of the total cost of goods available for sale divided by the retail value of those goods. The method is most useful for retailers that apply a standard markup percentage to all of the items they buy. For example, if a company typically buys inventory for $100, applies a 25% markup and sells the goods for $125, its cost-to-retail ratio is $100/$125 = 80%.

Here are the steps to calculate:

- Multiply net sales for the period to date by the cost-to-retail ratio to obtain an estimate of COGS.

- Use the standard inventory valuation formula: Add together the period’s beginning inventory plus the cost of additional inventory purchases to date, and subtract the estimated COGS to get your ending inventory.

| RETAIL PROS | RETAIL CONS |

|---|---|

|

|

Examples of Ending Inventory

The fictitious company 123 Holdings needs to calculate ending inventory to prepare financial statements at the end of the current period. The company started the current quarter with 100 units of inventory, all of which were purchased at $10 each. During the quarter, the company sold 200 units. It replaced them with three additional batches of inventory purchased at different prices, leaving the company with 100 inventory items at the end of the period.

| Number of units | Unit cost | Total Cost | |

|---|---|---|---|

| Beginning inventory | 100 | $10 | $1,000 |

| Purchase #1 | 50 | $12 | $600 |

| Purchase #2 | 50 | $15 | $750 |

| Purchase #3 | 100 | $16 | $1,600 |

| Beginning inventory plus net purchases | $3,950 | ||

The next three examples show how the company can calculate its ending inventory value using the FIFO, LIFO and WAC methods. For each example, the same basic formula is used to calculate ending inventory:

Ending inventory = beginning inventory + net purchases - COGS

Two more examples follow that illustrate the gross profit and retail methods.

Example 1: FIFO

The first step is to calculate COGS for the 200 items sold during the quarter. Using FIFO, the assumption is that these were the earliest items purchased:

- 100 items were purchased at $10 each as part of the beginning inventory, for a total cost of $1,000.

- 50 items were purchased at $12 each for a total of $600.

- 50 items were purchased at $15 each for a total of $750.

- Purchase #3 is not part of the calculation because they were the last items in and weren’t sold.

COGS, therefore, is $2,350 ($1,000 + $600 + $750) and ending inventory is $1,600 ($3,950 - $2,350).

Example 2: LIFO

With LIFO, COGS for the 200 sold items is based on the most recent purchases:

- 100 items were purchased at $16 each for a total of $1,600.

- 50 items were purchased at $15 each for a total of $750.

- 50 items were purchased at $12 each for a total of $600.

- Beginning inventory is not part of the calculation because they were the first items in and weren’t sold.

COGS, therefore, is $2,950 ($1,600 + $760 + $600) and ending inventory is $1,000 ($3,950 - $2,950).

Example 3: WAC

With WAC, the company assigns the same weighted average cost to every unit, whether sold or unsold.

- 300 units were purchased for a total cost of $3,950, giving a weighted average cost per unit of $13.17 ($3,950 / 300).

COGS, therefore, is $2,633 (200 x $13.17) and ending inventory is $1,317 ($3,950 - $2,633).

Example 4: Gross Profit Method

Components distributor Widgets Wholesale Inc. was hit by a devastating warehouse fire that destroyed much of its inventory. The company wants to quickly estimate the value of its remaining inventory. It uses the gross profit method to estimate ending inventory based on its net sales and expected gross profit margin.

- Beginning inventory = $500,000

- Net purchases = $250,000

- Net sales = $300,000

- Expected gross profit margin (based on historical business performance) = 40%

The company uses the gross profit method formula to estimate COGS: net sales x (1 - expected gross profit margin). Estimated COGS, therefore, is $180,000 ($300,000 x 60%).

The company then applies the standard ending inventory valuation formula: beginning inventory + net purchases - COGS. Estimated ending inventory, therefore, is $570,000 ($500,000 + $250,000 - $180,000).

Example 5: Retail Method

All Cheaper Stuff Inc. sells thousands of low-cost items through a chain of retail stores, applying a standard markup of 25% to the items it buys. Because it would be incredibly difficult and time-consuming to obtain an exact inventory count, it uses the retail method to estimate ending inventory.

- Beginning inventory = $400,000

- Net purchases during the current period = $250,000

- Net sales = $300,000

- Cost-to-retail ratio (COGS divided by retail value of goods) = 80%

The first step to calculate estimated COGS: net sales x cost-to-retail ratio. Estimated COGS, therefore, is $240,000 ($300,000 x 80%).

The company then uses the basic ending inventory valuation formula: beginning inventory + net purchases - COGS. Estimated ending inventory, therefore, is $410,000 ($400,000 + $250,000 - $240,000).

How to Use Ending Inventory

Ending inventory isn’t just a number on the balance sheet — it serves as a critical tool for making informed financial decisions. Whether it’s used to verify stock counts, calculate net income or shape future financial reports, understanding how to use ending inventory can help companies make informed adjustments to purchasing strategies and production plans.

Accurate Inventory Counts

Ending inventory helps businesses keep tabs on their stock by ensuring that inventory records align with the actual physical count of goods. This process reduces the risk of costly mistakes, such as overordering, underordering or mismanaging stock levels, all of which can disrupt operations and impact sales. By regularly comparing inventory counts with sales and purchase data, companies can quickly spot and fix discrepancies to minimize losses. Regularly updating these counts also confirms that inventory management systems are functioning properly, allowing for better forecasting and a clearer understanding of future stock needs and customer demand.

Calculate Net Income

Ending inventory has a direct and significant role on a company’s net income by influencing COGS. When ending inventory is higher, COGS decreases, leading to a higher net income. Conversely, when ending inventory is lower, COGS increases, resulting in lower net income. This relationship highlights the importance of accurate inventory calculations in financial reporting. By understanding how inventory levels affect profitability, businesses can make more informed decisions about pricing strategies, how to best manage production and ways to maximize profit margins. Regularly calculating ending inventory also ensures financial statements reflect the true cost of operations, providing insight into the company’s overall financial health.

Guide Future Reports

Ending inventory data is essential for generating accurate financial statements, sales forecasts and other reports that enable businesses to quickly respond to market changes and stay competitive. On the financial side, for instance, ending inventory directly impacts balance sheets and income statements by influencing COGS and net income.

By tracking trends in ending inventory over time, businesses can better predict seasonal demands, adjust procurement strategies and optimize stock levels. This data then contributes to inventory turnover reports, which support a company’s ability to identify slow-moving items, prevent overproduction and avoid underordering.

Ending inventory also plays a key role in budgeting, cash flow projections and sales forecasts by offering insights into the company’s financial standing and future capital needs. Accurate inventory data helps businesses anticipate how much cash will be tied up in stock, enabling them to allocate resources more effectively for future periods. When integrated into sales forecasts, ending inventory trends provide a clearer picture of expected revenue, guiding financial planning and strategic investments.

Calculate Ending Inventory With Inventory Management Software

As a business grows, inventory management can become extremely complex. Accurately calculating ending inventory may involve tracking large numbers of items as well as their purchase prices and associated costs. Manually tracking this inventory with spreadsheets is extremely labor-intensive and error-prone, which is why many businesses use inventory management software to automate the process. Comprehensive cloud-based inventory management systems can automatically track inventory in real time across all locations. Whether a company operates locally or in many markets, leading inventory management solutions scale with the organization to ensure ending inventory calculations are accurate and based on up-to-date inventory and sales data. This helps companies optimize inventory levels, reduce cost, improve cash flow and profitability, and increase customer satisfaction.

Ending inventory is a critical metric for any company that sells physical goods, affecting both the balance sheet and income statement. It’s important to choose a valuation method that matches the company’s needs — the choice can affect the stated value of the company’s assets as well as its profit and the amount of taxes it owes. Inventory management software can help businesses track ending inventory more easily while reducing the potential for manual error.

Ending Inventory FAQs

What should be included in ending inventory?

Ending inventory is the value of finished sellable goods at the end of a given accounting period. It takes into account the beginning inventory at the start of the period, any purchases during the period and the cost of the items sold during the period.

What is current period’s ending inventory?

The ending inventory for a current accounting period is equal to beginning inventory from the same period plus all purchases made during that period, minus the total cost of goods sold (COGS) in the period.

Is ending inventory an expense?

Ending inventory is an asset, not an expense. When inventory is sold, its cost is then treated as an expense and is added to the company’s cost of goods sold (COGS) for the period.

How do you calculate beginning and ending inventory?

Beginning inventory is equal to the ending inventory from the previous accounting period. Ending inventory is calculated by adding the period’s net purchases to the beginning inventory, then subtracting cost of goods sold (COGS). Although all methods for calculating ending inventory use this formula, they calculate COGS in different ways and may yield different values for ending inventory.

Where is ending inventory on an income statement?

Ending inventory isn’t a line item that directly appears on a company’s income statement, but it does play a critical role in calculating cost of goods sold (COGS), which generally appears after revenue to determine gross profit.