In short:

- Three factors determine whether any merger will succeed — and the priority may not be what you expect

- If a combined company is suffering from slow growth, high turnover and customer defections, a cultural mismatch is the top likely culprit

- Price is the last thing you should zero in on. A great deal that fails wasn’t really a bargain

During the late ’90s dot-com boom, Whittman-Hart bought USWeb/CKS for $5.7 billion. The deal combined two powerhouse internet consulting and services firms. And it was a colossal failure.

USWeb/CKS management had acquired a spate of consulting firms in the years before the Whittman-Hart purchase. At the time of the deal, it was a compilation of approximately 45 companies. After the ill-thought-out merger, the combined company’s workforce grew to 9,700 from 4,500, office locations ballooned from 22 to 71 and receivables skyrocketed to more than $400 million from $90 million. It was too much for management, employees and customers to digest.

Not long after the deal closed, MarchFirst, the name of the joint company, took a $59.8 million charge for bad receivables in one quarter alone. It put $70 million into a venture capital firm to invest in potential clients and bought $65 million of its shares back. It launched a major ad campaign and was spending upwards of $100 million annually on office space, while available cash was sinking at a rate of about $30 million per month.

Barely a year after the acquisition, MarchFirst tumbled headfirst into bankruptcy court — taking more than 4,000 jobs and two once-leading firms down with it.

“I made a major mistake buying a company that grew over four years and 45 acquisitions,” said Bob Bernard, the original CEO of Whittman-Hart who led the acquisition, as he resigned. “There was never a culture. The culture was based on buying companies.”

The Whittman-Hart and USWeb/CKS merger failed for a whole slate of reasons. But most notably, as Bernard admitted, it was first and foremost a cultural mismatch.

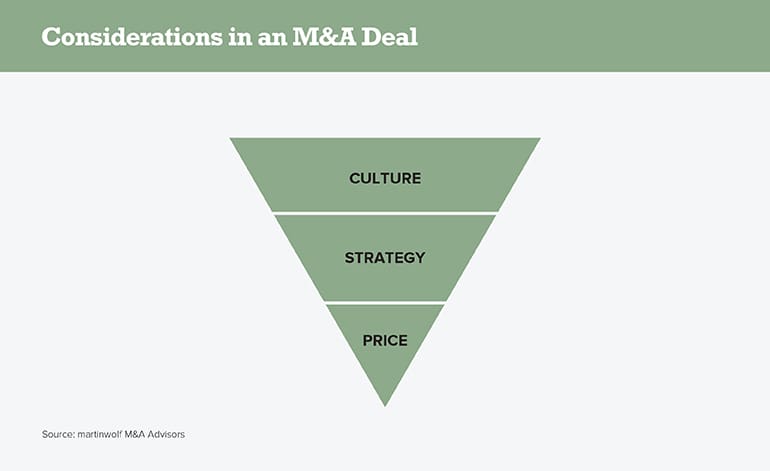

Unfortunately, decision-makers tend to get distracted by shiny objects, like a bargain asset or a significant increase in valuation. Which leads me to the point of this piece. The ‘“secret” to M&A success is that there is no secret. The go/no go calculation for any transaction must be based on three factors: culture, strategy and price, with the former the most important and the latter the least.

Why Culture is King

When two companies lack a cultural fit, that fact manifests after the acquisition in some unpleasant ways: slow to no growth, low employee morale, poor customer experience and a turnover of key personnel.

The Harvard Business Review defines culture types as tight or loose: “Tight company cultures value consistency and routine. They have little tolerance for rebellious behavior and use strict rules and processes to uphold cultural traditions. Loose cultures are much more fluid. They generally eschew rules, encourage new ideas, and value discretion.”

In a study done by experts at HBR on tight/loose cultures, companies in mergers with tight/loose differences saw their return on assets decrease by 0.6 percentage points three years after the merger, averaging $200 million in net income per year. For especially severe cultural mismatches, like Whittman-Hart-USWeb/CKS, average yearly net income dropped by over $600 million.

An acquisition succeeds only when there is cultural alignment. And that’s more than the tight/loose model. Culture includes factors like salaries and pay structure; benefits, like retirement plans; perks such as company cars or generous allowances for technology or memberships; reimbursement and T&E policies; and whether the company is customer-, employee- or operational-efficiency-centric.

Culture drives success. It’s what keeps key personnel from leaving, allows for customer stability and new customer development, boosts employee morale and ultimately makes for a more valuable company.

Nail cultural integration, and the acquisition is much more likely to succeed. Fail, and the next two elements won’t save you.

Strategy

Making our way down the inverted pyramid, we land on strategy as the second most important factor in an M&A transaction, not far behind culture. Before acquiring, or being acquired, leadership must drill down on the existing business strategy and where the company wants to go.

For example, many financially accretive companies take a step back on strategy. They dig themselves into the “we buy this asset, we become this much more valuable” mindset. That generally does not end well, and we have history to prove it.

Consider Office Depot’s failed acquisition of CompuCom, for one. Office Depot was primarily centered around providing low-cost products for SMBs and very large enterprise accounts — a riff on the “barbell” approach. It then acquired CompuCom, an enterprise services business. If you sell enterprise accounts low-value products, why are they going to trust your company to provide high-value services? And by definition, SMBs are not candidates for your services. The strategy angle was not thought through. CompuCom, valuable in and of itself, has failed to thrive within its strategic acquirer.

Another obvious strategy fail was Microsoft’s purchase of Nokia. At the time (meaning, before Azure existed), Microsoft was largely a desktop business just crawling into services; it had no presence in the mobility space.

The phone business snuck up on Redmond, so it bought a company that knew hardware but had lagged on smartphones. Making the strategy work required software that Microsoft did not have. It also needed to be seen as a manufacturer of high-value devices. Microsoft failed on both counts, to the tune of about $8 billion.

Financially the Nokia acquisition might have made sense, if leadership had drilled down into specifics: business model, service offerings, customer base, how to break the iOS and Android duopoly. But they didn’t, and strategic differences meant the transaction was bound to fail.

And Finally, Price

CFOs — and the entire executive team — usually focus 90% of their time and attention on price, the least important aspect of a transaction.

The reality: There is no “fair” value. It’s always subjective — though you should always have a ballpark idea of your company’s market value, as I explain here. And, no transaction comes in down to the exact dollar estimated. We’ve worked with multibillion-dollar global entities that paid more at the end of the process than the initial expectation, but the transaction worked. And that cost everyone less, in the end, than a failed deal.

For example, we advised Bain Capital, a large, global private equity firm, in its minority investment in VXI Global Solutions. While terms of the deal were not disclosed, Bain sold its stake for $1 billion, significantly more than it bought into VXI for. An extra 10% or $10 million on the front end wouldn’t have made a difference.

That’s not to say you should overpay. What I am saying is that a good transaction with a nominal price premium works. What fails every time is to get an asset on the cheap that does not have the proper cultural fit or alignment with your strategy.

A note on principal-to-principal interactions: In a typical transaction, sellers are focused on price, while buyers should be more concerned with culture and strategy. This all becomes complicated if you need the seller to operate the business post-acquisition.

Depending on the role of the seller, particularly if there is an earn-out or expectation that the principal will stay on, it’s very difficult to negotiate price and maintain a working relationship. In these cases, find an outside adviser that can evaluate the culture and strategy fit before anyone even starts to negotiate on price. That makes it more likely the deal closes, with the most value possible for both buyer and seller.

Knowing where you are now, where you want to go in terms of strategy and culture, and how to marry those two is the key to successful M&A. Don’t sweat too much on the price and let it ruin an ideal fit.

Need advice on how to set yourself up for success before you get to the transaction phase? Check out my advice on how to prepare your company for sale when you’re not for sale.

Marty Wolf has been involved in more than 150 IT M&A transactions during the last 20 years, creating over $5 billion in value. In addition to his responsibilities as president of global M&A advisory firm martinwolf M&A Advisors, which he founded in 1997, he actively manages transactions, has been directly involved in the divestiture of seven Fortune 500 divisions, and closed transactions in over 22 countries in segments including IT services, supply chain, and SaaS. Marty also acts as counselor and trusted adviser to CEOs of select IT firms. He has advised on take-private strategies and corporate carve-outs, as well as defended firms in hostile tender offers. He is a columnist and frequent speaker at IT and M&A conferences. Contact Marty via email.