It’s critical that small-business leaders understand the financial health of their organizations, and financial metrics and key performance indicators (KPIs) inform that understanding. Small-business financial metrics shed light on the company’s current financial state and its short- and long-term outlook.

Financial metrics and KPIs help small businesses understand if they have the cash on hand to fund big capital investments—or are on the fast track to insolvency. These numbers are obviously important to business owners, but lenders and investors will also want to review them before they sign any contract with a company.

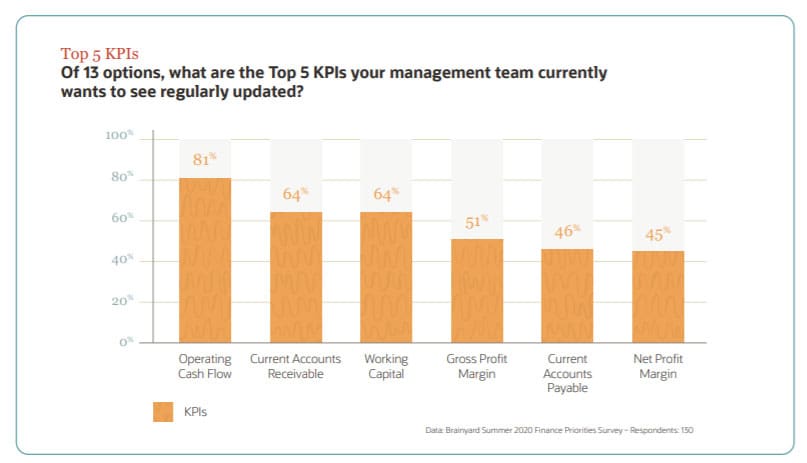

There are certain metrics that are vital to the success of a small business.

What Are Metrics?

Metrics are any quantifiable data a company may monitor to track performance and improvements across the business. While financial metrics are among the most important and widely used, businesses can use metrics to monitor the success of any aspect of their operations, like monthly website visitors or average order fulfillment times.

Once an organization starts tracking an important metric, it has a baseline against which it can compare future numbers to see how the performance of various processes or teams has changed over time. As a business grows, it often starts tracking more metrics, including ones specific to certain initiatives or departments.

What Are KPIs?

Key performance indicators, or KPIs, are metrics that are particularly important to your business. These numbers have the biggest impact on whether your company thrives and grows or struggles and shuts down. A distinguishing feature of KPIs is they usually have predetermined goals, which is not true of all metrics—a company might monitor certain metrics for years without specific targets in mind. Certain financial metrics are also KPIs since profitability and cash flow play major roles in the immediate and future viability of a business.

Small-business executives should choose their critical KPIs early on and establish a clear understanding of what numbers will indicate success, or raise warning flags. KPIs should be closely tied to key business objectives. For example, average customer account size could be a manufacturing KPI to watch if a company wants to increase revenue by 10% this year. If that manufacturer is looking to increase productivity at its plant, another KPI could be the number of products produced per day.

Defining and Choosing the Right KPIs and Metrics for Small Businesses

The metrics small-business leaders need to pay attention to vary from one company to the next, and KPIs are even more specific and depend on industry, business and financial model and goals. The leadership team should first establish business objectives for the quarter or year and work backward from there, identifying the KPIs and metrics that will help it stay on target. These discussions should include employees from all key departments to ensure goals are relevant to the entire company.

However, there are a few common financial metrics that all companies need to keep an eye on. They need to have a firm grasp of total revenue, expenses, assets and liabilities and how each shifts over time. The cost of customer acquisition and how long those customers stick around, a.k.a. churn rate, are other metrics important to many young companies. For products-based companies, tracking the efficiency of various processes and employee productivity at manufacturing plants or warehouses is often important.

15 Key Financial Metrics & KPIs for Small Businesses

While organizations need a firm grasp of what will make them successful and which industry-specific KPIs matter to them, there are metrics relevant to most businesses. Here are our Top 15 most commonly applicable metrics and KPIs:

-

Revenue

Revenue is the amount of money a business takes in for sales of its products or services before any expenses are taken out. Revenue, also called sales or top-line income, is part of the calculation for most financial metrics. There are multiple ways to measure revenue. In accrual accounting, customer purchases made on credit count toward revenue before the business has actually received payment. In cash accounting, only money already in the company’s bank account counts toward revenue.

Revenue = Sales Price x Units Sold

-

Expenses

Expenses are all the costs a business must cover to operate and earn revenue. With some exceptions, such as VC-backed startups, a business needs more revenue than expenses to survive. Examples of expenses are labor, equipment, and supplies. Just like with revenue, accrual accounting factors in expenses as they are incurred, even if they haven’t been paid yet, while cash accounting includes these expenses only once they’re paid.

Expenses can be grouped into two broad categories: operating expenses and nonoperating expenses. Operating expenses are a direct result of doing business, like mortgages, production costs and administrative costs. Nonoperating expenses are more indirect and include interest and other lending fees.

Expenses = Cost of Goods Sold + Salaries + Sales Commissions + Marketing Costs + Real Estate Expenses + Utilities

-

Net Income

Net income or net profit is the money left over after subtracting all expenses and taxes from revenue. Although there are investor-backed startups that lose money, most small businesses need to bring in enough revenue to cover their expenses. If they don’t, they risk falling into debt and eventually going out of business.

Net income is also referred to as the “bottom line” because it shows up below revenue (the “top line”) on profit and loss (P&L) statements.

Net Profit = Revenue – Total Expenses

-

Cash Flow/Operating Cash Flow

Cash is the lifeblood of small businesses—they rely on the money coming in to pay expenses. Cash flow is the amount of money moving in and out of a business over a certain timeframe. If more money is coming in than going out, a business has positive cash flow, and if it’s paying out more money than it’s receiving, it has negative cash flow.

Operating cash flow (OCF) is the amount of cash a company generates through typical operations. This metric can give a business a sense of how much cash it can spend in the immediate future and whether it should reduce spending. OCF can also reveal issues like customers taking too long to pay their bills or not paying them at all.

Operating Cash Flow = Net Income + Non-Cash Expenses – Increase in Working Capital

-

Working Capital

Working capital is the difference between current assets (cash, accounts receivable and short-term investments) and liabilities (accounts payable, payroll, taxes and debt payments). This metric helps paint a picture of a business’s financial state for the near term by looking at is available liquidity to cover immediate expenses.

Working Capital = Current Assets - Current Liabilities

-

Budget vs. Actual

Just as it sounds, budget vs. actual compares a company’s actual spend or sales in a certain area against the budgeted amounts. Although budgets and expense are related, budget vs. actual can be used to compare both revenue and expenses.

This “budget variance analysis” helps small business leaders identify areas of the business where they’re overspending that may need further attention. It also reveals areas of the business that outperformed expectations.

Budget Variance Percentage = Actual/Forecast – 1 x 100

-

Accounts Receivable Aging

Accounts receivable aging is a report that measures how many days it takes your customers to pay their bills. Companies often include credit terms on an invoice that say how many days the customer has to submit payment; 30 days is common.

On an accounts receivable aging report, a business typically organizes clients by due date—immediately, 1–30 days late, 31–60 days late—to see how much money is collectable from different companies and timeframes.

When accounts receivable consistently runs behind, it hurts cash flow and working capital. As more time passes, the chances of ever collecting that revenue decrease. Businesses may need to cut ties with customers that are consistently late, as these delays can cause a cash flow crunch. Companies should consider offering customers a small discount for early payment to prevent delays.

-

Accounts Payable Aging

Accounts payable aging is a report similar to accounts receivable aging, except it looks at how many days it takes your business to pay its bills. Like with accounts receivable aging, a company lists its upcoming bills based on when they’re due to ensure it can meet all obligations and resolve any problems ahead of time. Revenue, cash flow and accounts receivable aging can all affect your ability to keep up with invoices from suppliers, technology vendors and other business partners.

How quickly a company pays its bills affects its creditworthiness and ability to get a loan. Companies that are able to stay on top of their financial obligations can reinvest the savings from early payments back into the business.

-

Break-even Point

The break-even point(opens in new tab) is when revenue is equal to costs, meaning there is no profit or loss. Also known as margin of safety, break-even point helps a business know when it will earn more than it spends and start earning a profit. By calculating the break-even point, a software provider knows how many licenses it needs to sell, or a manufacturer understands how many products it must move to cover monthly costs.

Break-even Point = Fixed Costs/(Sales Price Per Unit – Variable Cost Per Unit)

-

Gross Profit Margin Ratio

Gross profit margin ratio shows revenue after deducting the cost of goods sold (COGS)—that is, the direct costs of making a product. This ratio, written as a percentage, reveals the gross profit for every dollar of revenue a business earns. A ratio of 60%, for instance, means the company receives 60 cents of profit for each dollar of revenue.

Gross Profit Margin Ratio = (Revenue – COGS)/Revenue x 100

-

Profit Margin Ratio

Profit margin ratio is similar to the gross profit margin ratio but accounts for all expenses, like payroll and other operating costs, rather than just COGS. Although standard profit margins differ between industries, many companies target a profit margin ratio of at least 25%.

Profit Margin Ratio = (Revenue – Expenses)/Revenue

-

Quick Ratio (Acid Test Ratio)

Quick ratio(opens in new tab), also called the acid test ratio, measures whether a business can fulfill its short-term financial obligations by evaluating whether it has enough assets to pay off its current liabilities. Quick ratio is written as a decimal, with a ratio of 1.0 meaning a company has just enough assets to cover its liabilities.

Quick Ratio = (Cash + Marketable Securities + Accounts Receivable)/Current Liabilities

-

Average Customer Acquisition Cost

Average customer acquisition cost uncovers how much a company spends, on average, to add new customers during a certain period of time. This metric factors in expenses for marketing, technology, payroll and more. Customer acquisition cost is typically proportional to the price of a product or service, so it varies widely by industry—the average retailer spends $10 to acquire a customer, while the typical technology provider shells out $395.

An organization can compare customer acquisition cost to customer lifetime value to make sure its business model is sustainable. If necessary, a company can lower its customer acquisition costs by reducing marketing spend and focusing on customer retention and upsells.

Cost of Customer Acquisition = (Cost of Sales + Cost of Marketing)/New Customers Acquired

-

Churn Rate

Churn rate calculates how frequently customers stop using your product or service over a given timeframe. Are a quarter of customers abandoning your service after a year or do most use it for five years? Does that churn rate make sense for your industry or business model? A high churn rate suggests a company needs to change something about its offering, better nurture its customers and/or lower its customer acquisition cost.

Churn Rate = Lost Customers/Starting Number of Customers x 100

-

Cash Runway/Burn Rate

Cash runway calculates how long a company has before it runs out of cash based on the money it currently has available and how much it spends per month. This metric helps businesses understand when they need to cut back spending or get additional funding. If your cash runway shortens over time, it’s a sign your company is spending more money than it can afford to.

Cash runway is closely tied to burn rate, which measures how much money a company spends over a certain period (usually monthly). Burn rate is frequently used by investor-backed startups that lose money in their early days.

Cash Runway = Cash Balance/Monthly Burn Rate

How Can Financial Software Help With Setting and Tracking Financial Metrics and KPIs?

Tracking even basic metrics like revenue, expenses and income can become cumbersome with spreadsheets or other manual methods. It's difficult to keep all this information up-to-date, especially as a small company grows and its transaction volume increases, and that can lead to inaccurate information.

Manually calculating more advanced metrics, like break-even point, quick ratio and average customer acquisition cost, is even more challenging.

Financial or accounting software makes it far easier and less time-consuming to find the numbers needed for these metrics. Leading solutions can make these calculations with just a few clicks, and business stakeholders can automatically and regularly receive reports showing select metrics and KPIs.

These solutions open up countless possibilities to view and compare numbers that illuminate your business’s performance and help identify issues holding it back—all without consuming a lot of employee time or effort. There is tremendous value in real-time data, and that alone often justifies the cost of the solution.

Small businesses must set clear KPIs and track a wide variety of metrics to excel in today’s turbulent environment. Without insights, these companies have no true sense of how they’re progressing toward goals and whether they're financially healthy or digging themselves into deep holes. Corporate leaders must make it a priority to pinpoint the KPIs and metrics that matter most to their businesses, monitor them and continually adjust based on what the data tells them.

Technology, even a basic financial system, can go a long way toward helping companies track these numbers and spot changes that will have a positive or negative impact on their financial health. Small firms need metrics because they can be a deciding factor in whether or not a business makes it.