The law of supply is an economic theory that predicts how the price of goods and services affects their supply. It says that as prices rise, businesses will increase the amount of goods and services that they make available. Though the law of supply can be useful when making business decisions, it doesn't take into account other factors that can affect supply, such as changes in production costs and the competitive environment. Still, understanding the law of supply, as well the exceptions to the law and other relevant factors, can help companies determine how to price their products and services and adjust their supply to maximize profits.

What Is the Law of Supply?

The law of supply is a basic economic concept. It states that an increase in the price of goods or services results in an increase in their supply. Supply is defined as the quantity of goods or services that suppliers are willing and able to provide to customers. The law works like this: Rising prices mean that products become more profitable, assuming other factors such as production costs remain constant. The prospect of higher profits therefore motivates businesses to supply more of these products. Existing suppliers may increase the supply of more profitable products at the expense of less profitable ones. In addition, new suppliers may enter the market, further increasing the overall supply.

Key Takeaways

- The law of supply states that an increase in the price of goods or services results in an increase in the quantity that suppliers make available to the market.

- Existing suppliers increase production of higher-priced goods to maximize profits, while new suppliers may also enter the market.

- The law of supply assumes that all other factors remain constant. In practice, many other factors can play into supply decisions, including rising production costs and market competition.

Law of Supply Explained

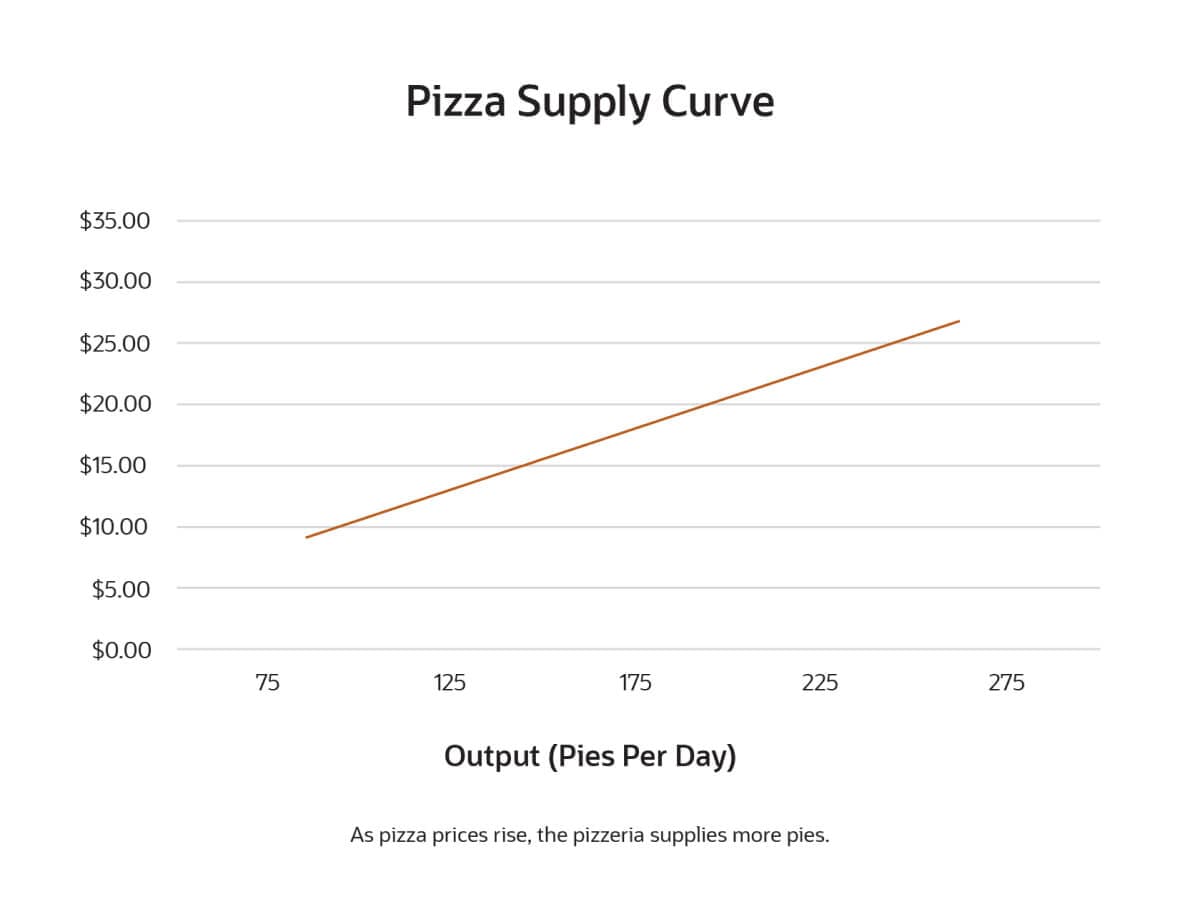

Consider the example of a pizzeria that sells pasta dishes as well as pizzas. If the price of pizza rises, and with it the profit per pie, the business may focus its resources on increasing the production of pizza — while decreasing the production of pasta offerings. As the price keeps rising, the pizzeria continues to increase the pizza supply because it can increase its profits by doing so. This relationship can be represented graphically as a supply curve, which shows the number of pizzas produced at different prices.

As prices and output continue to increase, the supplier eventually reaches the maximum quantity that it can provide with its existing equipment — it can't make any more pizzas because its ovens are already full at all times. The pizzeria may then decide to invest in an additional pizza oven to increase its supply. Meanwhile, other entrepreneurs establish new pizzerias because the higher prices justify the startup costs. This further increases the market supply.

How Does the Law of Supply Work?

The law of supply applies to services and labor as well as goods — a higher price can increase the supply. For example, employees may be more likely to work overtime if they're paid at a higher hourly rate. Professions that offer relatively high salaries, such as software engineering, may attract more people to educational programs that ultimately increase the supply of qualified job applicants.

In practice, prices are often determined by the relationship between supply and demand. A related economic theory, the law of supply and demand, describes how this works. Rising demand for products and services tends to drive up prices. This provides an incentive for providers to increase the supply. However, as the price of those products and services continues to rise, fewer customers will buy them. The law of supply and demand predicts that as a result, free markets move toward an equilibrium point where the price and quantity of the supply exactly matches customer demand.

Factors That Affect Supply

The law of supply predicts that rising prices result in increases in the supply of goods or services — but that's assuming all other factors remain constant. In reality, many other factors can affect supply, and those factors can change frequently. Here are 10 of the most common.

-

Price and demand forecasts.

Many businesses base their production plans on forecasts of future demand and pricing, not just on what customers are currently buying. Enterprise resource planning software can help businesses improve demand forecasts by considering factors such as economic growth and seasonality. Furthermore, if a product's price is expected to increase, businesses may hold back stock so they can make a larger profit in the future.

-

Production costs.

The law of supply assumes that companies can increase profits by selling more goods or services when prices rise, which provides them with an incentive to increase the supply. But if the price rises reflect increased production costs, that may not be true. If a pizzeria raises the price of a slice by 50 cents because the cost of the tomatoes used in the sauce went up by 50 cents, its profit is unchanged — so the price increase doesn't represent an incentive to make more pizzas. On the other hand, if production costs fall and prices remain stable, profits increase and so does the incentive to supply more pizzas.

-

Competition.

New suppliers may enter the market even if prices are not increasing and demand is stable. Often, these new suppliers aim to offer products at lower prices than existing providers.

-

Technology.

Technology can enable companies to make and sell more products at a lower cost, thus increasing the available supply.

-

Transportation.

Transportation delays or rising shipping costs can affect a company's ability to increase its supply of goods. If goods can't move from warehouses to retail shelves, they can't be purchased by customers and don't count toward the market supply.

-

Availability of raw materials and labor.

A business may want to increase the supply of a product but unable to do so because it can't purchase the raw materials or hire the people required to produce it.

-

Government regulations and subsidies influence supply in some industries.

Companies must meet strict regulatory requirements when introducing certain healthcare products, for example, which can limit the supply of these products regardless of the demand. On the other hand, government subsidies support the supply of some local transportation services.

-

Weather and natural disasters.

For many agricultural goods, the weather has a major impact on supply. A dry season or flooding can greatly reduce crop yields.

-

Comparable goods.

A change in the supply of one good can affect the supply of other goods. For example, if the market price of corn increases, farmers may dedicate more land to growing corn. As a result, they use less land for growing squash, so the supply of squash decreases.

-

Business objectives.

Companies may adjust the supply of products to achieve specific objectives. For example, some businesses introduce limited-edition collectibles in small quantities to increase their desirability and value. At the other extreme, companies sometimes supply products in large quantities to build market presence and brand awareness, even if increasing the supply doesn't generate higher profits.

Types of Law of Supply

There are five types of supply — market supply, joint supply, composite supply, short-run supply and long-run supply. Here's how to distinguish them.

-

Market supply.

The market supply is the total supply from all producers. If a town has three pizzerias that produce 30, 40, and 25 pies a day, respectively, at $20 apiece, the market supply at the $20 price level is 95 pies a day.

-

Joint supply.

Joint supply occurs when multiple goods are produced from a single source. For example, cows can be used to produce milk as well as leather.

-

Composite supply.

Composite supply occurs when goods are intrinsically linked and sold only as a bundle. For example, a car manufacturer typically offers air conditioning and audio systems only as part of a bundled package with the purchase of a new vehicle.

-

Short-run supply.

Short-run supply is the total supply that companies can provide without additional investment in business expansion. It's also known as short-term supply.

-

Long-run supply.

Long-run supply, also known as long-term supply, includes factors such as suppliers' investment in new production capacity. It also considers that new suppliers may enter the market while older firms exit.

Exceptions to Law of Supply

Not every business scenario is determined by the law of supply. There are many exceptions — situations where the supply of goods and services isn't determined by the pricing. Here are some of the most common.

-

Economies of scale.

When a producer becomes large enough, it may be able to apply economies of scale to reduce the cost of producing goods and services. As a result, it may be able to increase its supply while keeping prices stable or even reducing them.

-

Shift in business plan.

If a business is shifting its market focus and plans to cease production of some products, it may temporarily increase the supply of those products at a low price to eliminate any remaining stock and raw materials. A business may also use this approach as an emergency measure if it needs cash in a hurry.

-

Monopoly.

When there's only a single supplier of a good or service, the company may be able to increase or decrease its supply or pricing irrespective of external factors.

-

Competitive pricing.

In a highly competitive market, businesses may increase the supply of their products while reducing the price to capture market share.

-

Expiring or dated goods.

If perishable goods near their expiration date, a business may increase their supply early to try to recoup some of the production costs before the goods become unsellable.

-

One-of-a-kind goods.

Handmade art or other rare goods cannot be easily reproduced, so the supply cannot expand even if the price rises.

-

Inelastic supply.

For many goods, including agricultural products, it is difficult to quickly adjust the supply even if the price rises. It can take months or even years for crops to reach maturity and become available to customers. For example, an apple farmer who adds trees to their orchard won't be able to harvest the fruit for several years.

Law of Supply Examples

The law of supply operates across almost every industry. Here are some common examples.

- The owner of a coffee shop notices that sandwich prices are rising. To boost profits, the owner starts making more sandwiches for sale.

- A movie studio sees that major theaters are charging higher prices for blockbuster films, so it begins greenlighting more projects to develop star-studded action movies.

- Noticing that the price of organic vegetables is increasing faster than the price of conventionally produced crops, a farmer starts the process of gaining organic certification.

Conclusion

The law of supply describes a simple relationship between pricing and supply — the higher the price of an item, the more suppliers will make. In practice, many other factors can affect both supply and pricing, including production costs, the availability of raw materials and the competitive environment. So while it's useful to consider the law of supply when making business decisions, it's equally important to take into account other factors that may apply to your situation.

Law of Supply FAQs

What is the basic law of supply?

The law of supply states that as prices increase, overall supply will increase. Existing suppliers increase their production to maximize profits. New sellers may also enter the market.

What is law of supply and law of demand?

The law of supply and the law of demand are two sides of the supply equation. The law of supply states that as prices increase, so does the amount produced by sellers. The law of demand states that as prices increase, customer demand declines. Theoretically, a free market will move toward an equilibrium point where the price and quantity of the supply exactly matches the demand.