In short:

- Extending the runway is a given. But there’s more to do to keep your company financially viable until the recovery kicks in.

- Don’t count on a straight line. Plan to withstand fits and starts.

- Decisiveness is a virtue in turbulent times. He who hesitates ... well, you know the rest.

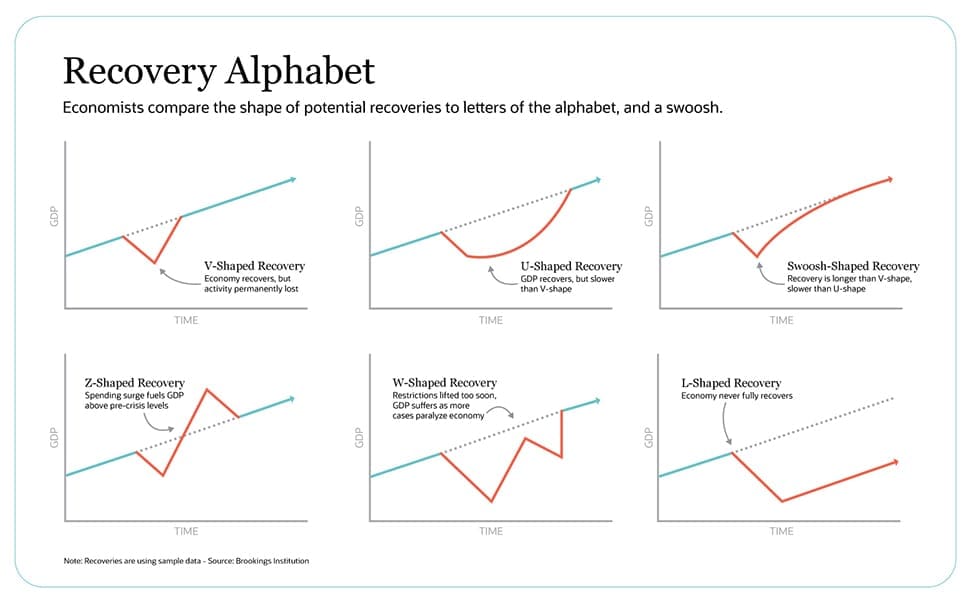

As the global economy gradually reopens, the multi-trillion-dollar question is, What shape will the bounce take? An L? A U? A V, W or Z? Maybe a square-root symbol?

I have my thoughts, but prognostication is an iffy business because the current situation is unprecedented, for two reasons. First, most major global economies ground to a halt nearly in unison. And the response by central banks and governments has been aggressive — a good thing, in my opinion, but also the reason the market is now above where COVID-19-driven financial damage froze business. That makes the Dow a poor bellwether.

For CFOs facing uncertainty (that is, all of them) my advice is to heed the words of illustrious British PM Benjamin Disraeli: “I am prepared for the worst, but hope for the best.”

Founders, who are by nature optimists and not prone to preoccupation with downside scenarios, tend to favor the second half of that concept more than the first. Finance leaders may need to inject a dose of reality, because the current situation carries so much uncertainty that if your company does not prepare for downside scenarios, you might not be around for the bounce.

Leaders including Washington governor Jay Inslee have said economic recovery will be more like turning a dial than flipping a switch. Analysts agree, so let’s consider the possible recovery scenarios laid out by The Brookings Institution .

The second quarter will be problematic across the board, with variability depending on sector. The big unknowns are the third and fourth quarters. The uncertainty is so extreme that no management team can rely on historical metrics as a predictor of future performance.

In a best-case V-shaped recovery, most companies will be able to benefit from the upswing, provided it begins early in the second half. However, any of the other five possibilities may prove disastrous unless you take decisive action.

I recommend modeling three scenarios for your business’ revenue, relative to pre-pandemic levels, along with associated operating expense and headcount plans at those respective levels.

Ideally, your company had 12 to 18 months of cash and debt capacity heading into the pandemic; however, for many, the financing window shut before they were able to access additional funding. As we explore these scenarios, how many months of runway you have will dictate your margin for error and the commensurate advisable expense and headcount reductions.

If you need advice on extending your runway, here’s my take.

Three Scenarios to Model

Scenario 1: Your company’s post-pandemic reduced revenue stays depressed through the third quarter of 2020.

In this scenario, resembling a V-shaped recovery, your business recovers to pre-pandemic levels in the fourth quarter of this year. If, come the fourth quarter, your company has less than six months of cash and debt capacity, operating expenses should be reduced on the order of 5%, with a particular focus on variable, nonessential costs such as marketing and travel.

Extend payment terms with vendors to the extent possible.

Hires not absolutely critical to the functioning of the business should be pushed out. Headcount reductions are not necessary, though salary reductions may be instituted for a temporary, pre-set period of time to extend the runway. I advise making the cuts needed to take your cash burn above six months, minimum, exiting the fourth quarter.

Fundraising conversations can start during the fourth quarter, given a firm recovery well recognized, with a Q1 closing target.

Scenario 2: Your company’s post-pandemic revenue stays depressed further into the fourth quarter of 2020.

In this scenario, resembling a swoosh-shaped recovery, business does not expand until early in the first quarter of 2021. If your cash and debt capacity does not exceed nine months exiting 2020, then beyond the moves recommended in Scenario 1, headcount reductions and steeper cuts in operating expenses, likely in the 10% to 15% range, need to be explored closely.

During the first quarter, additional equity and/or debt financing conversations should begin, with a target closing in late second quarter.

Scenario 3: Lowered revenue extends through a good part of the first half of 2021.

In this scenario, resembling at best a U- or W-shaped recovery, business flatlines through early 2021. Operating expenses must be reduced beyond the relatively modest cuts in the two scenarios above, on the magnitude of 20% to 25%. Further headcount reductions must be made to preserve a cash runway of at least nine months, and ideally 12 months, exiting 2020.

Further, in this scenario it will be difficult to raise additional capital, so it’s best to prepare a lower cost structure to be positioned to navigate a difficult 2021.

Probability Planning

The stock market is projecting a V-shaped recovery, but that’s skewed by huge stimulus spending. I think we’re due for something between a V and a W, with a square-root sign my best guess.

And of course, some industries are in significantly better shape than others. CFOs need to continually and closely monitor the dynamics for the overall economy, your industry and your business and ascribe a likelihood percentage to each of the three aforementioned scenarios. Aggregating the probability-weighted results should result in an operating expense and headcount reduction target.

The longer you wait to implement recommended cuts, the shorter your runway. As Sequoia sagaciously advised in March : “Nobody ever regrets making fast and decisive adjustments to changing circumstances. In downturns, revenue and cash levels always fall faster than expenses.”

I see minimal appetite for financing in the venture equity and debt community. New funding isn’t completely off the menu, as I’ll discuss in my next column, but you’ll need a sustainable profitability bent.

Disraeli also wrote, “Success is the child of audacity.” After a realistic self- and market-analysis, move quickly. Waiting for a clear sign that the economy has not rebounded may prove disastrous if it’s then too late to make appropriate adjustments.

Josh Burwick is an active private technology investor with a particular focus on software, Blockchain, e-commerce and sports betting technology. He has served as an interim CFO and advised on strategic fundraising for a variety of technology companies, ranging from Series A to Series D rounds.

For more helpful information from the Brainyard and our friends at Grow Wire and the NetSuite Blog , visit the Business Now Resource Guide.