Efficient, low-cost production is fundamental to business success. Maximizing production is often a key business goal, but sometimes increasing production can result in lower profits. Using marginal cost, businesses can optimize production volumes, set prices advantageously and deploy resources efficiently. This article explains how to calculate marginal cost and use it to help reduce costs and increase profits.

What Is Marginal Cost?

Marginal cost is the additional cost incurred by a business when it increases production by one unit. Increasing production can reduce marginal cost through efficiency gains known as “economies of scale.” However, once maximum efficiency is achieved, marginal cost can start to increase. Keeping track of marginal cost requires good cost accounting that clearly separates fixed and variable costs. When it is used routinely as part of management accounting, marginal cost can help businesses optimize production volumes and set prices so as to maximize revenues. Reducing marginal cost can increase a company’s ability to grow the business and improve its bottom line.

Key Takeaways

- Marginal cost is the additional cost that a business incurs when it produces one more unit of a product.

- Increasing production can reduce marginal cost through efficiency improvements known as economies of scale.

- However, once production has reached maximum efficiency, further increases in output tend to increase marginal cost.

- Businesses can maximize profits by increasing production to the point where marginal cost equals marginal revenue.

Marginal Cost Explained

Marginal cost — the incremental cost of producing one extra unit of a product — goes hand-in-glove with marginal revenue, which is the incremental revenue earned from producing that one additional unit. The value difference between marginal cost and marginal revenue is the incremental profit gained from producing the extra unit. But if marginal cost exceeds marginal revenue, increasing production means lower profits.

Marginal cost takes into account the variable costs associated with the added production, such as the need for additional labor and materials. Fixed costs remain the same no matter the level of production, so they are not a factor.

Marginal cost is related to another manufacturing concept, average cost, but is not quite the same. To illustrate this, imagine that a business produces 100 notebooks at a total cost of $1,000. The average cost of production is $10 ($1,000/100). Now suppose the business produces one more notebook. The total number of notebooks produced is now 101, and the total cost has risen to $1,010. The cost of producing that one extra notebook is $10. That’s the marginal cost of production.

In this example, the marginal cost is the same as the average cost, which means the company is operating at optimal production efficiency. But this isn’t always the case. Typically, companies that are scaling up from low levels of production find their marginal cost falls below their average cost as production increases because they are increasing their production efficiency and thus spreading both fixed and variable production costs over a larger quantity of output. However, companies that are already running at high output levels can find that increasing production raises their marginal cost above their average cost because production errors increase due to the faster pace of production and more human time is needed to maintain quality.

Often, the solution to rising marginal cost is to invest in fixed assets, such as plant and machinery, to increase production capacity. But this raises fixed costs. The marginal cost calculation, however, is a measure of the efficiency of production using existing fixed assets. As such, fixed costs are assumed not to change.

If an increase in production arises from new investments in fixed assets, then the marginal cost can be calculated only for any subsequent increase in production since that investment. Including changes in fixed costs in the marginal cost calculation can give a false impression of the company’s production efficiency.

Marginal Cost Formula

To understand why marginal cost might fall and then rise, it’s crucial to know that the marginal cost formula includes only changes in production cost and changes in production output. To calculate the marginal cost of a production increase, a business needs to know its total cost of production before and after the additional production and the number of additional units produced. The formula for marginal cost is:

Marginal cost (MC) = Change in total cost / Change in quantity of output

This table demonstrates how marginal cost might fall, then rise, as the notebook business described above expands its output:

How Changes in Output Can Affect Marginal Cost

| Output | Fixed Cost ($) | Variable Cost ($) | Marginal Cost ($) |

|---|---|---|---|

| 0 | 500 | 0 | |

| 50 | 500 | 500 | 10 |

| 100 | 500 | 850 | 7 |

| 200 | 500 | 1150 | 3 |

| 300 | 500 | 1300 | 1.5 |

| 400 | 500 | 1400 | 1 |

| 500 | 500 | 2100 | 2 |

| 600 | 500 | 3100 | 5 |

| 700 | 500 | 4700 | 10 |

The initial reduction in marginal cost is caused, first, by spreading fixed costs over a greater quantity of output, and second, by production efficiencies that reduce the variable cost of producing each item to achieve economies of scale. Applying the marginal cost formula, we see that when production increased by 50 to 100 units, the total costs of production (fixed + variable) increased by $350 ($1,350 – $1,000). Therefore, the marginal cost to produce each of those 50 units was $7 ($350 / 50).

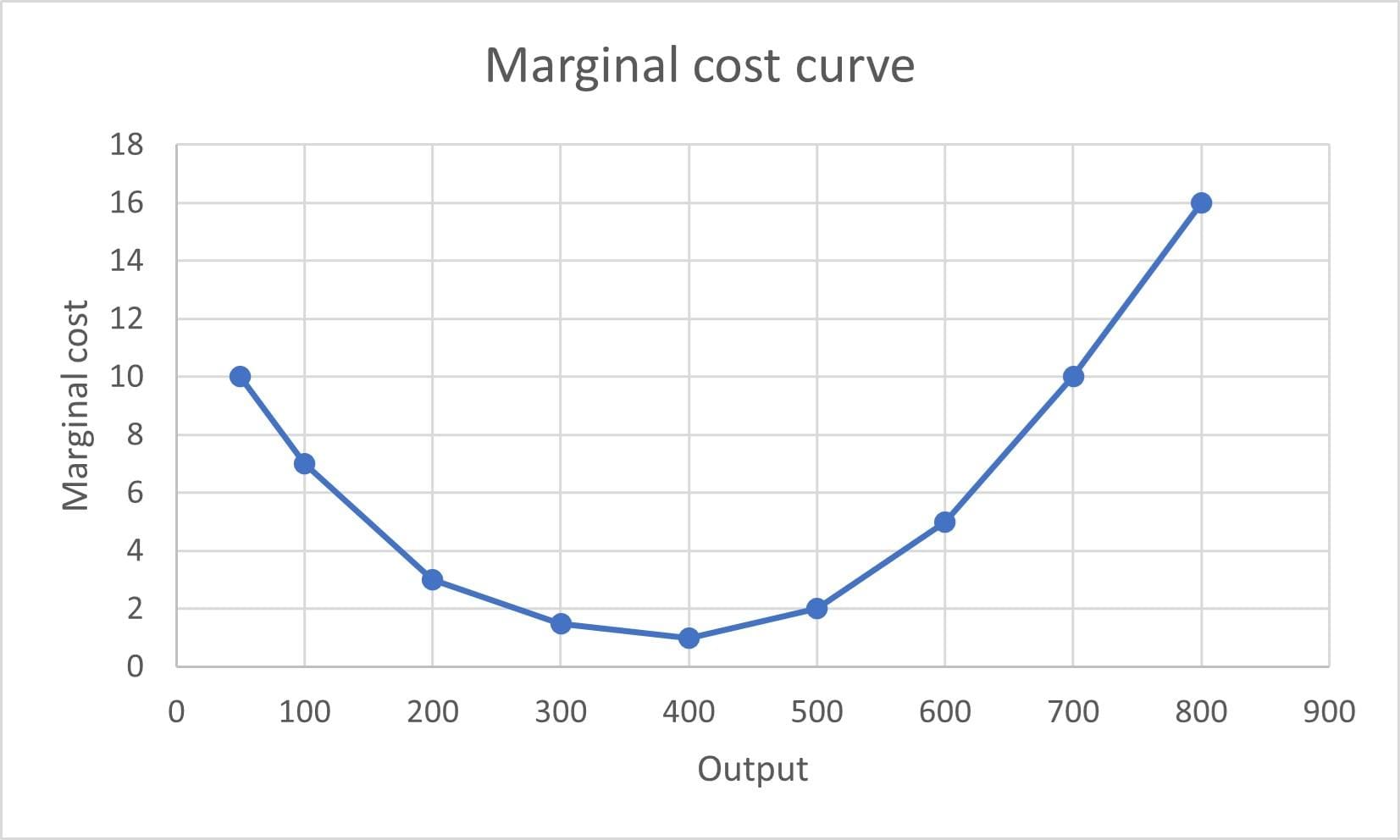

The table shows that the optimal output for this firm is 400 notebooks. At that point, the firm’s marginal cost of $1 is equal to its average cost. Beyond this, production efficiency declines and costs rise. This is known as diminishing marginal productivity.

How to Calculate Marginal Cost

Before calculating marginal cost, a business must first calculate its change in total production cost and change in quantity of output. Here’s how that’s accomplished.

1. Figure out the change in product quantity.

Although marginal cost is the additional cost of producing a single item, in practice businesses typically increase production by much more than one. The change in the quantity of product is the quantity currently produced minus the quantity previously produced.

Suppose the notebook manufacturer from above doubles its production, from 100 notebooks to 200. The change in the quantity of notebooks is 100 (200 – 100).

2. Determine the change in total cost when output changes.

It’s tempting to assume that production costs will increase in line with the increase in production. But this isn’t necessarily the case: When production efficiency is improving, output increases more than production costs. But, once maximum efficiency has been achieved, increasing production can disproportionately increase costs. Therefore, calculating marginal cost needs to use actual production costs as identified in cost accounting. The total cost of production is the total cost after the increase minus the total cost before the increase.

Suppose the notebook manufacturer’s total cost before the production increase was $1,350 and afterward was $1,650. The change in the total cost is $300 ($1,650 – $1,350).

3. Run the marginal cost calculation.

With the change in output and change in total cost calculated, a business is ready to calculate its marginal cost. For the notebook manufacturer, here is the math:

Marginal cost = Change in total cost / Change in output

= 300/100

= $3

The original unit production cost for each notebook was $10 (at 50 units). So in this case, the marginal cost of $3 is much lower than the initial unit cost. This means that doubling the quantity of output is efficient for this company.

Limitations of the Marginal Cost Calculation

Marginal cost is a powerful metric, but it has some limitations. These limitations arise from the subjective nature of many costs and the imperfect link to prices and revenues.

Assumptions and Conditions

The marginal cost formula assumes that fixed costs are clearly defined and can be easily separated from variable costs. In practice, this is not so simple. For example, highly skilled members of staff may be salaried (a fixed cost), but if they are asked to work a weekend, the company might also have to pay them overtime (a variable cost). Replacing an administrator’s laptop is a fixed cost, but repairing it if something goes wrong could be considered a variable cost. Also, the marginal cost calculation assumes that fixed and variable costs can be accurately allocated to individual product lines. However, the allocation of overhead is up to the discretion of management.

In addition, because the marginal cost calculation doesn’t take into account changes in fixed costs, marginal cost analysis can result in a business failing to cover its fixed costs fully. Conversely, including changes to fixed costs in marginal cost analysis can disguise changes in variable costs arising from production increases, giving a misleading impression of production efficiency.

Real-World Variances

Marginal cost implicitly assumes that consumer demand doesn’t change, so any increase in production can always be absorbed by the market without a change in prices. However, consumer demand is variable and dependent on market and economic conditions that are typically beyond the company’s control. Marginal cost calculations don’t take into account economic indicators or consumer surveys. That means a marginal cost calculation that indicated increasing production would improve the company’s bottom line could therefore be wrong. Business managers are wise to look at market and economic indicators before moving ahead with a production increase.

Visualizing the Marginal Cost Curve

Marginal cost curves are typically U-shaped. As a company scales up from low levels of production, marginal cost falls until production reaches maximum efficiency. After that point, marginal cost rises. The point on the curve at which marginal cost is lowest is known as the “turning point.”

The exact shape of a marginal cost curve varies from business to business. Here’s what the marginal cost curve for the notebook manufacturer looks like.

10 Key Benefits of Marginal Cost

Using marginal cost analysis can help managers optimize business performance across a number of areas. But marginal cost isn’t limited to businesses. It also helps in environmental and sustainability analyses, government policy, and financial and investment analyses.

1. Optimizing Production Levels

The most cost effective production level for a company is the turning point on the marginal cost curve. Modeling marginal cost changes using different assumptions of output can thus help companies identify the production level that minimizes their costs. Combining the marginal cost curve with a marginal revenue curve can further help managers identify the optimal production level to maximize profits.

2. Pricing Strategy

Calculating the marginal cost of a product can help a business determine its pricing strategy, particularly during periods of poor sales. If the price that the market will bear falls below the marginal cost of the product, the business may decide to cut production rather than accept losses.

Under conditions of perfect competition — for example, if 10 businesses are all selling an undifferentiated product in a restricted market — the price of a product is its marginal cost. However, perfect competition is rare. In most markets, businesses sell differentiated products, and price is a factor of demand as well as marginal cost. Businesses can use marginal cost to set a minimum price for a particular product and add a markup based on market information.

3. Resource Allocation

Businesses can use marginal cost analysis to allocate resources in order to optimize output across all business lines.

4. Informed Decision-Making

Marginal cost analysis can help business managers decide which product lines have potential for expansion, which ones would benefit from further investment and/or greater resources, which ones need pruning for optimal performance and which ones should be considered for sale or phasing out.

5. Supply Chain Management

Production costs are heavily influenced by companies’ relationships with suppliers. Marginal cost analysis can help companies identify where costs are rising, such as for raw materials, leading them to consider whether changing suppliers or negotiating better deals could reduce their costs. Marginal cost analysis can also help identify where suppliers’ pricing strategies make upscaling production advantageous, such as if a supplier charges lower unit prices for larger orders.

6. Consumer Benefit

Marginal benefit is the maximum amount of money a consumer will pay to acquire one additional good or service. When production is sufficient to meet demand, marginal consumer benefit will equal the marginal cost of production. But often marginal benefit is higher or lower than marginal cost. If marginal benefit is higher than marginal cost, then companies can raise their prices. But if marginal benefit is lower than marginal cost, companies may choose to reduce or cease production of that good or service.

For business managers, keeping an eye on both marginal costs and marginal revenue allows them to identify when marginal consumer demand is falling below marginal cost.

7. Technological Implementation

A major benefit of technology is increased productivity and efficiency across the entire business. For example, investing in cloud computing can streamline administration, improve communication and eliminate resource-hungry paper-based processes. These improvements will be reflected in lower marginal costs. The cost of investments in technology can be allocated as fixed costs across all product lines, and the benefits can be monitored using marginal cost analysis.

8. Market Structure Analysis

Economic theory says that in perfectly competitive markets, the price of a good will be the marginal cost of production. But not all markets are perfectly competitive. Identifying where market prices differ from marginal cost can help financial analysts, investors and economists understand the structure of a market and the competitive pressures companies face in that market. For example, in an oligopolistic market, which is dominated by a few large players, the dominant players may benefit from economies of scale, enabling them to keep prices below smaller companies’ marginal cost of production.

9. Economic Policy and Welfare

Minimizing production costs can help keep prices low for consumers. This can be particularly important for essential goods and services, such as food, energy and healthcare, since high prices for these goods and services can be unaffordable for low-income consumers.

According to economic theory, when production is sufficient to meet demand, the price paid by consumers will be the marginal cost of production. Marginal cost analysis can help governments set economic policy to optimize production of essential goods and services and minimize the cost to consumers. For example, by taking on the cost of building and maintaining a national grid, governments might subsidize fixed (infrastructure) costs for providers of energy, thus reducing their marginal cost of production and helping to keep prices low for households and small businesses. However, taxpayers would bear the cost of this subsidy. Welfare policy would have to consider whether the welfare benefit of the subsidy outweighs the welfare cost of higher taxation.

10. Environmental and Sustainability Impact

In environmental economics, the marginal cost of pollution is the cost to the environment arising from the production of one additional good or service. For example, in agriculture, producing more crops can increase nitrate run-off into watercourses; in manufacturing, increasing steel production using traditional blast furnaces can increase carbon emissions. The marginal cost to the environment can be weighed against the welfare benefit to people.

Marginal Cost Examples

In addition to the notebook manufacturer, let’s take a look at two more hypothetical examples that bring to life the concept of marginal cost.

Example 1: A manufacturer of beauty products has introduced a new product line. The new line is selling well, and now the manufacturer is considering whether to discontinue its old line and redeploy resources to the new line. Marginal cost calculations reveal that the marginal cost of the old line is $10, while the marginal cost of the new line is $15. The marginal revenue of the old line is $8, while the marginal revenue of the new line is $10. However, the new product line is not yet at full production capacity, while the old line is already close to capacity and production errors are high. Management models forward-looking marginal cost curves for both lines, which indicate that increasing production on the new line would reduce marginal cost below marginal revenue, but increasing production on the old line would mean further deterioration in the contribution of that line to the company’s bottom line unless the firm invested in new production equipment. Based on this analysis and consumer surveys indicating good demand for the new product line, the company decides to discontinue the old line and increase production on the new line.

Example 2: A manufacturer of luxury bespoke automobiles has a long waiting list for its products. It wants to increase production, but the size of its facility means it can produce only an additional five vehicles per year. A forward-looking marginal cost analysis incorporating the cost of moving to bigger premises reveals that after the move, the company would have to produce another 20 vehicles per year to generate sufficient profits to cover its premises costs. The company believes there is sufficient consumer demand, but it doesn’t think it can find the skilled staff needed to ramp up production to such an extent. So it decides to stay in its existing facility and limit production to five vehicles per year.

Reduce Costs and Improve Efficiency With NetSuite Accounting Software

The ability to properly calculate marginal cost rests on a company’s record-keeping accuracy regarding its production and inventory costs. NetSuite’s cloud accounting software increases accounting accuracy by automating error-prone manual accounting processes that could impact results and lead to faulty decision-making about whether boosting production is in the company’s best financial interest. Through seamless integration with NetSuite Enterprise Resource Planning (ERP), the software can easily access and analyze necessary manufacturing, procurement, inventory and supply-chain data. The end result? Business managers are best-positioned to manage costs and improve efficiency, potentially leading to better customer and supplier relationships, clearer opportunities for long-term expansion and, most important, higher profits.

Marginal cost is an indispensable metric for identifying production efficiencies, deploying resources effectively and creating opportunities for business expansion. When used in conjunction with marginal revenue, marginal cost can help businesses maximize their profits.

Marginal Cost FAQs

What is “marginal” in marginal cost?

In economics, “marginal” relates to one unit. So “marginal cost” means the cost incurred by producing one additional unit of a product. Marginal is also sometimes expressed as “at the margin.”

What assumptions does the marginal cost formula have?

The marginal cost formula assumes that fixed and variable costs are clearly defined and easily separable and that only variable costs can change. It also assumes that consumer demand will always be sufficient to absorb increases in production, which isn’t necessarily the case. This is why businesses may find it helpful to analyze their marginal revenues as well.

How does marginal cost affect consumer decision-making?

Consumers aren’t usually aware of a company’s marginal cost. However, they will notice if a company increases prices because its marginal cost is rising. If the price rises above a consumer’s marginal benefit, they won’t buy the product. So rising marginal cost for a company can result in lower consumer demand for the company’s goods and services.

What industries benefit from knowing marginal cost?

Marginal cost is helpful to all goods producers and many service industries. It is particularly important for large-scale manufacturing companies that can benefit from economies of scale.

What’s the difference between marginal cost and marginal revenue?

Marginal cost is the additional cost of producing one more unit of a product. Marginal revenue is the additional revenue earned from producing and selling one more unit of a product. The maximum economic production level for a company is the point where marginal cost equals marginal revenue. If marginal cost exceeds marginal revenue, increasing production will mean the company loses money.

How do you calculate marginal cost?

To calculate marginal cost, a business must first calculate the formula’s two variables: change in total production cost (before and after the production increase) and change in quantity of output (before and after the production increase). Change in total cost is then divided by change in quantity of output, resulting in marginal cost.

What is the full formula of marginal costing?

The formula to calculate marginal cost is: Change in total cost / Change in quantity of output.