Account reconciliation is a key step in the financial close process. The practice of comparing a balance in a company's general ledger (GL) to the balance on an independent statement and investigating any differences helps reassure accountants and business executives that their companies' books are up to date, accurate and complete. It's also an important outcome, since GL balances flow into a company's financial statements, which are used for internal and external decision-making. Bank reconciliations tend to be the first kind of account reconciliation that comes to mind given the implications for cash flow, but account reconciliation applies to other accounts as well, such as inventory, accounts receivable and intercompany accounts, to name a few. Account reconciliation of all GL accounts is a best practice that businesses should have in place — and it's even better when the process is automated.

What Is Account Reconciliation?

A company's books are comprised of seven types of GL accounts that track its financial activity: assets, liabilities, equity, revenue, expenses, gains and losses. As part of the bookkeeping process, every business transaction is posted to two or more GL accounts using corresponding debits and credits that indicate value coming into or going out of the business. Account reconciliation confirms the accuracy of each GL account — not just cash accounts, as commonly thought of — by comparing the details to data from another source, such as a bank statement. The process may uncover errors, omissions or duplications in the GL, any of which would have to be investigated and corrected before reconciliation can occur.

Key Takeaways

- Account reconciliation is a primary internal control that maintains the accuracy of a company's general ledger (GL) and detects fraud.

- Bank reconciliation is the most common type of account reconciliation, but all GL accounts can benefit, especially assets, liabilities and equity accounts.

- The documentation approach to account reconciliation is the most helpful for identifying and evaluating specific reconciling items. A second approach is called the analytic method.

- Account reconciliation is ideal for automation, freeing staff to focus on exception resolution and account analysis.

Account Reconciliation Explained

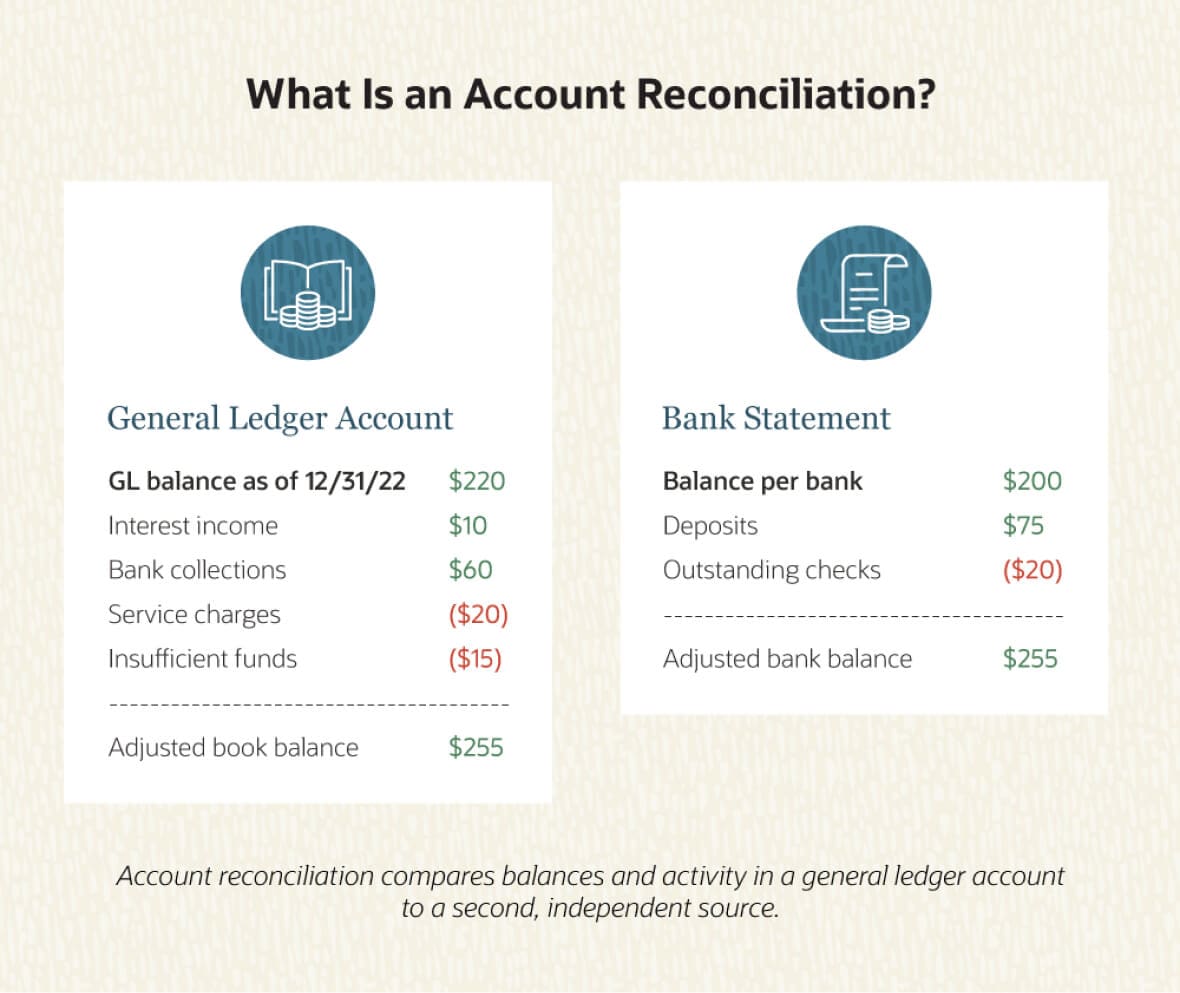

Account reconciliation in business is similar to the familiar process of balancing a personal checkbook. In the latter scenario, one compares the balance on the bank statement to that in the checkbook register (which is analogous to the GL), and then compares the activity on both the bank statement and in the checkbook register, looking for items that don't match. These are called reconciling items, and they are added or subtracted to each balance to bring the bank statement and checkbook register into agreement, or balance. A bank fee is a common reconciling item that reduces a bank balance but usually isn't reflected in the person's checkbook register. By discovering the bank fee during the reconciliation process, the person can add the amount to the checkbook register and bring its balance in line with the bank's.

Why Is Account Reconciliation Important?

Account reconciliation is an effective internal control for keeping a company's GL account balances accurate. In turn, this process increases the accuracy of financial statements and analyses — which are based on the GL and are used by internal decision-makers and external stakeholders. In addition, regular reconciliations to outside information can uncover fraud and anomalies. For example, an account reconciliation for inventory compares the GL account balance of the items believed to be held in inventory to an actual physical count of warehouse stock. When large discrepancies are discovered, the company may find that they're due to theft.

It's especially important to reconcile the balance sheet accounts — assets, liabilities and equity — since these are permanent accounts in financial accounting, meaning their balances persist from one accounting period to the next. For example, the ending balance in an asset account on Dec. 31, 2022, becomes the beginning balance on Jan. 1, 2023 (unlike a revenue account that starts fresh each fiscal year). Accuracy is important, so errors should be reconciled as soon as possible.

Account reconciliation is useful to external auditors, who require the process and review records when assessing a public company's internal controls environment, as set forth by the Sarbanes-Oxley Act of 2002. For smaller companies, account reconciliation can be an important control to help mitigate risks that may be introduced if a company lacks segregation of duties, meaning there's no division of responsibility between different people to reduce the temptation and opportunities to commit fraud.

How Does Account Reconciliation Work?

Account reconciliation compares the balance in a company's GL account with another source of information that contains details about specific transactions — such as bank statements, credit card statements, loan statements or separate internal systems, such as fixed asset, accounts receivable and inventory subledgers — to make sure GL account activity is complete and accurate. Any differences are investigated, and corrective action is taken when appropriate.

At the end of the process, the GL account balance may change using an adjusting journal entry. The internal control value of an account reconciliation is considered stronger when the second source of data comes from a third party, like a bank or credit card company. However, performing account reconciliations against internal sources, like subledgers or intercompany accounts, is still useful.

Sometimes account reconciliations are done to simply understand why balances correctly differ between two sources. Investment account reconciliations are a good example, since balances may differ due to daily market fluctuations. In addition, not all reconciling items require balance adjustments. Timing differences are one example, such as when an outstanding check that has been deducted from a paying company's GL cash balance has yet to be deposited at the receiver's bank. As a result, the check funds remain in the payer's account and the bank balance will appear higher than the GL balance until the funds have been withdrawn from the payer's account.

When Does Reconciliation Happen?

In most accounting departments, account reconciliations are done before the month-end financial close. Adjusting journal entries for any reconciling items that are discovered are posted to the GL in the current period. During the year-end financial close, the books may be left open for a brief period of time so that account reconciliations for major accounts can be performed and adjustments are included in the final balances before closing.

In some cases, account reconciliation happens more frequently, such as weekly or daily. These reconciliations are usually done as part of a continuous close process, or they may involve accounts with high volume or sensitive activity. Bank reconciliations, which reconcile a company's cash accounts, typically occur more often. It is generally accepted that more frequent account reconciliation helps reduce the risks of material misstatement and loss. Additionally, the account reconciliation task becomes more time-consuming and complicated when it occurs less frequently.

Benefits of Account Reconciliation

Account reconciliation is a commonly used financial-close practice and is an important part of the control environment at companies of all sizes and in most industries. The many benefits include:

- Validating account balances in the GL with outside documentation.

- Increasing the accuracy of account balances by catching errors, such as incorrect calculations, omissions, duplications and human errors, such as transposing digits during data entry.

- Revealing potential fraud and other unusual activity.

- Avoiding overdrafts in bank accounts because balanced GL accounts balances supply a more complete and accurate view of current funds or position.

- Saving money by identifying hidden fees, such as storage fees, fuel surcharges, service charges and administration charges, and determining whether these fees are valid.

- Uncovering delayed, incorrect or surprising activity. For example, when reconciling inventory, a company may learn that a shipment was delayed, physical counts used incorrect quantities or inventory in a certain warehouse had unusual levels of damage.

Reconciliation Methods

Given how critical account reconciliations are, it may be surprising to learn that there is no official regulation or standard that guides their preparation. Accountants use two methods that are significantly different from each other and serve different purposes:

-

The documentation method is the process of comparing the GL to a second source document. This is the method described in this article, since it is the most commonly used, has the most practical applications and has a higher internal control value. The documentation method is best for validating GL account balances, ensuring completeness and identifying specific reconciling items. A bank reconciliation is a good example of the documentation method.

-

The analytic method is a high-level approach that uses estimates and assumptions to check a GL balance. Unlike the documentation method that “ticks and ties” by matching individual transactions across two separate sources, the analytic method compares a GL balance to a ballpark balance that is calculated using appropriate metrics. For example, if a company maintains a consistent outstanding loan balance, it may use the analytic method to estimate its quarterly interest expense based on the contractual interest rate. If the interest expense in the GL balance is materially close to the estimate, then the account would be considered reconciled and no further action would be taken. If the GL balance is significantly different than the analytic method indicated, a second, more detailed reconciliation would be initiated using the documentation method. The analytic method is an effective way to identify which accounts might need a closer look and is used to generally test GL account balances.

How to Reconcile Accounts

To get the most internal control benefit from account reconciliations, they should be prepared by someone other than the individual responsible for that account. In cases where staffing doesn't allow for this day-to-day segregation of duties, account reconciliation can provide an opportunity to catch mistakes or fraud. “Segregation of duties” is another way of saying that it's better to divide duties between different people, so that no single employee has the opportunity to view and alter financial data. Additionally, the more independent the second source of data is, the higher the internal control value, although any comparative analysis and transactional reconciliation can be helpful.

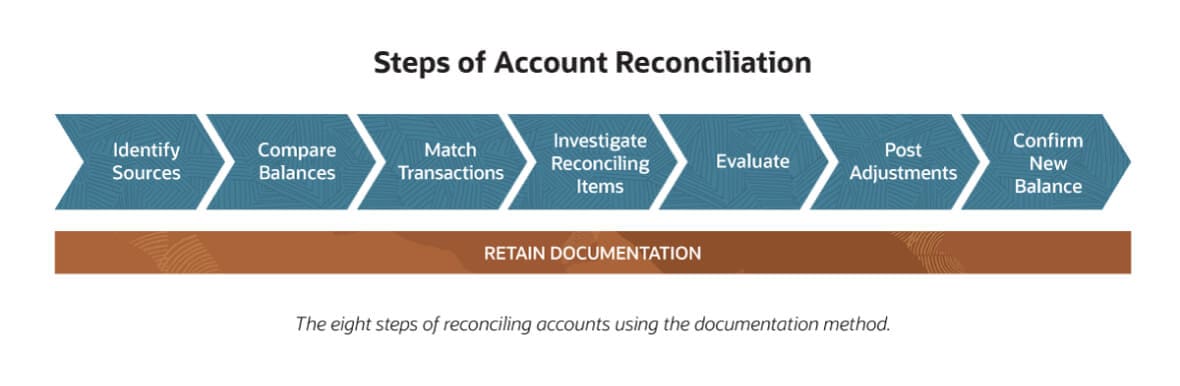

Steps of Account Reconciliation

When using the documentation method for reconciling accounts, the following steps are performed in this sequence:

- Identify the GL account to be reconciled and determine the best source to compare it against. Ideally, all accounts are reconciled on a regular basis. Various sources can be used for different accounts, but the same source should be used consistently.

- Compare the ending balances reflected on both sources, ensuring that the dates align. If the balances are the same, it's still worth completing the reconciliation to ensure there aren't offsetting errors within the transactions.

- Match each transaction in the GL to each transaction in the second source. Accountants call this tick and tie.

- List and investigate any items that do not match. Each reconciling item may require analyzing the internal GL data and/or the data from the second source.

- Determine whether corrective action is required for each reconciling item. Not all will.

- Post adjusting journal entries, if necessary.

- Confirm the new GL balance.

- Retain all reconciliation documentation to help with account reconciliation during the following month and for audit purposes.

6 Causes of Account Reconciliation Discrepancies

A primary benefit of the documentation method of account reconciliation is that it isolates individual reconciling items. Each item is investigated to determine whether further action needs to be taken. Reconciling discrepancies tend to be caused by:

-

Mistakes: Human errors, such as transposing digits, data entry errors or incorrect calculations.

-

Omissions: Transactions that were not included in the GL balance due to oversight or because they were unknown. A bank charge for a returned check is a common example.

-

Duplication: Transactions that were incorrectly included more than once. This can happen due to miscommunication among staff, technology glitches or simply hitting the “submit” button too many times.

-

Timing: A transaction that is included in one balance but not the other as a result of timing differences. It's important to investigate the underlying reason for timing differences to determine whether an adjusting journal entry is required. For example, a credit card statement that cuts off on Jan. 3, 2023, compared to the GL that ends on Dec. 31, 2022, causes timing differences that will likely need to be manually adjusted.

-

Miscoding: Transactions that are miscoded and included in the wrong GL account will skew a balance.

-

Fraud: Unauthorized transactions can be uncovered by account reconciliation, especially when the second source of information comes from an external, independent third party. A classic example of fraud is an employee who embezzles funds, cashing fraudulent checks that were not recorded or approved in the GL.

Manual vs. Automated Reconciliation

As beneficial as account reconciliations are, many companies aren’t able to dedicate the resources needed to do a complete reconciliation of all accounts every month. Additionally, the documentation approach takes time and is tedious when handled manually, often conflicting with pressures to close the books as quickly as possible. According to a recent study, 43% of companies surveyed used a fully manual or low level of automation account reconciliation, and another 46% had only partially automated this accounting subprocess. So, it’s easy to see why many companies resort to doing the bare minimum beyond bank reconciliations, often leaving other accounts, like inventory, intercompany and equity (among others) to languish.

Account reconciliation is a repetitive, voluminous and time-sensitive process that is ripe for automation. Technology, like artificial intelligence (AI), can perform matching at rates much faster than even the best accountant can tick and tie, enabling staff to focus on investigating items from an automated exceptions report, rather than checking each and every entry. Further, materiality thresholds can be set to ensure that the most significant items are investigated. For example, an unmatched $10,000 transaction could have a significant impact on a subsequent financial statement and should take priority for investigation, whereas a $1 transaction will make little difference.

Automation also provides a central repository for documentation, enhancing the audit trail and management reviews while also controlling access.

Psst...There’s a Better Way to Put Money Back in Your Business!

Improve Account Reconciliation With NetSuite

The right automation can greatly improve account reconciliation by speeding the process, optimizing staff time and increasing a company's ability to reconcile more accounts. NetSuite Cloud Accounting Software includes built-in banking integration with automatic data imports from bank and credit card accounts and matching software, which does all the heavy lifting of bank reconciliation. Exceptions are flagged for investigation, allowing staff to skip to step five in the reconciliation process, which calls for determining whether corrective action is required for each reconciling item. (See Steps of Account Reconciliation, above.) Similarly, embedded AI and optical character recognition (OCR) ease the burden of reconciling GL accounts by digitally accepting transactions and automatically categorizing them into the right GL accounts, matching transactions and balancing accounts. Further, the simplified chart of accounts helps eliminate miscoding, which is one of the most common causes of reconciling errors.

Account reconciliation is an internal control process that compares a company's GL balance with a second source to determine its validity and accuracy. A bank reconciliation, which compares a GL cash balance to an external bank statement, is the most common type of account reconciliation, but it's considered best practice to reconcile all GL accounts, especially assets, liabilities and equity accounts. Because account reconciliations are tedious and time-consuming, they are often done after the financial close, or they are delayed or even overlooked. Automation can help companies avoid being in this unfortunate position and allow businesses to capture the many benefits that account reconciliation provides.

Account Reconciliation FAQs

What are 3 types of account reconciliation?

Three common reconciliations are bank reconciliations and credit card reconciliations, both of which deal with cash, and reconciliations for balance-sheet accounts — assets, liabilities and equity. However, any and all general ledger accounts can be the subject of account reconciliation.

What are the steps in account reconciliation?

There are eight steps in the documentation method for reconciling accounts.

- Identify the general ledger account to be reconciled and determine the best source to compare it against.

- Compare the ending balances reflected on both sources, ensuring that the dates align.

- Match each transaction in the general ledger to each transaction in the second source.

- List and investigate any items that do not match.

- Determine whether corrective action is required for each reconciling item.

- Post adjusting journal entries, if necessary.

- Confirm the new general ledger balance.

- Retain all reconciliation documentation to help with reconciliation the following month and for audit purposes.

Why do we do account reconciliation?

There are four primary reasons for doing account reconciliations, although there are many other benefits as well. First, they are an effective internal control that helps keep a company's general ledger account balances accurate, which also increases the accuracy of financial statements and analyses that are often relied on by internal decision-makers and external stakeholders. Second, regular comparisons to outside information can uncover fraud and anomalies. Third, the balances on balance-sheet accounts — assets, liabilities and equity — persist from one fiscal year to the next, so detecting and correcting discrepancies is critical to avoid perpetuating errors. Fourth, external auditors require and review account reconciliations when assessing a public company's internal controls environment and fraud risk under the Sarbanes-Oxley Act.