The new lease accounting regulations will require strong accounting acumen. The new standards will require organizations that lease assets, or “lessees” to recognize the assets and liabilities of those leases on their balance sheets. The new guidance requires lessees to recognize assets and liabilities for leases with terms of more than 12 months.

The new regulations are consistent with Generally Accepted Accounting Principals (GAAP) in that lease reporting will depend on its classification as a finance or operating lease. Unlike GAAP, which requires only capital leases to be recognized, the new standards require both types of leases to be recognized on the balance sheet.

The new standards are aimed at helping investors and other financial statement users better understand the amount, timing, and uncertainty of cash flows arising from leases. Some confusion still exists around the topic. In 2005, the SEC conducted a survey that estimated the off-balance sheet obligation associated with operating leases for public companies was $1.25 trillion.

To that end, the new standards are designed to improve lease accounting in the following ways.

- Providing a more faithful representation of the rights and obligations arising from leases.

- Fewer opportunities for organizations to structure leasing transactions to achieve a particular accounting outcome on balance sheet.

- Improve the understanding and comparability of lessees’ financial commitments.

- Aligns lessor accounting and sale and leaseback transactions guidance more closely to ASC 606.

- Provides additional information about lessors’ leasing activities and lessors’ exposure to credit and asset risk as a result of leasing.

In preparing for ASC 842 and IFRS 16, there are lessons to be taken from the implementation of ASC 606. The process of adopting ASC 606 required businesses to gather all customer sales contracts and determine how to account for each component in the contract based on the standards. The process for lease accounting will be similar in approach to ensure that leases are compliant with the new lease accounting regulations.

The new lease accounting standards will be most challenging for dual reporting companies—those who are required to publish their financial information under both international standards—IFRS 16 and US GAAP - ASC 842. Dual reporting companies will need to maintain different processes, controls and accounting systems for each framework to comply with the different lessee reporting requirements.

For companies facing this hurdle, NetSuite’s Multi-Book functionality will ease this pain point.

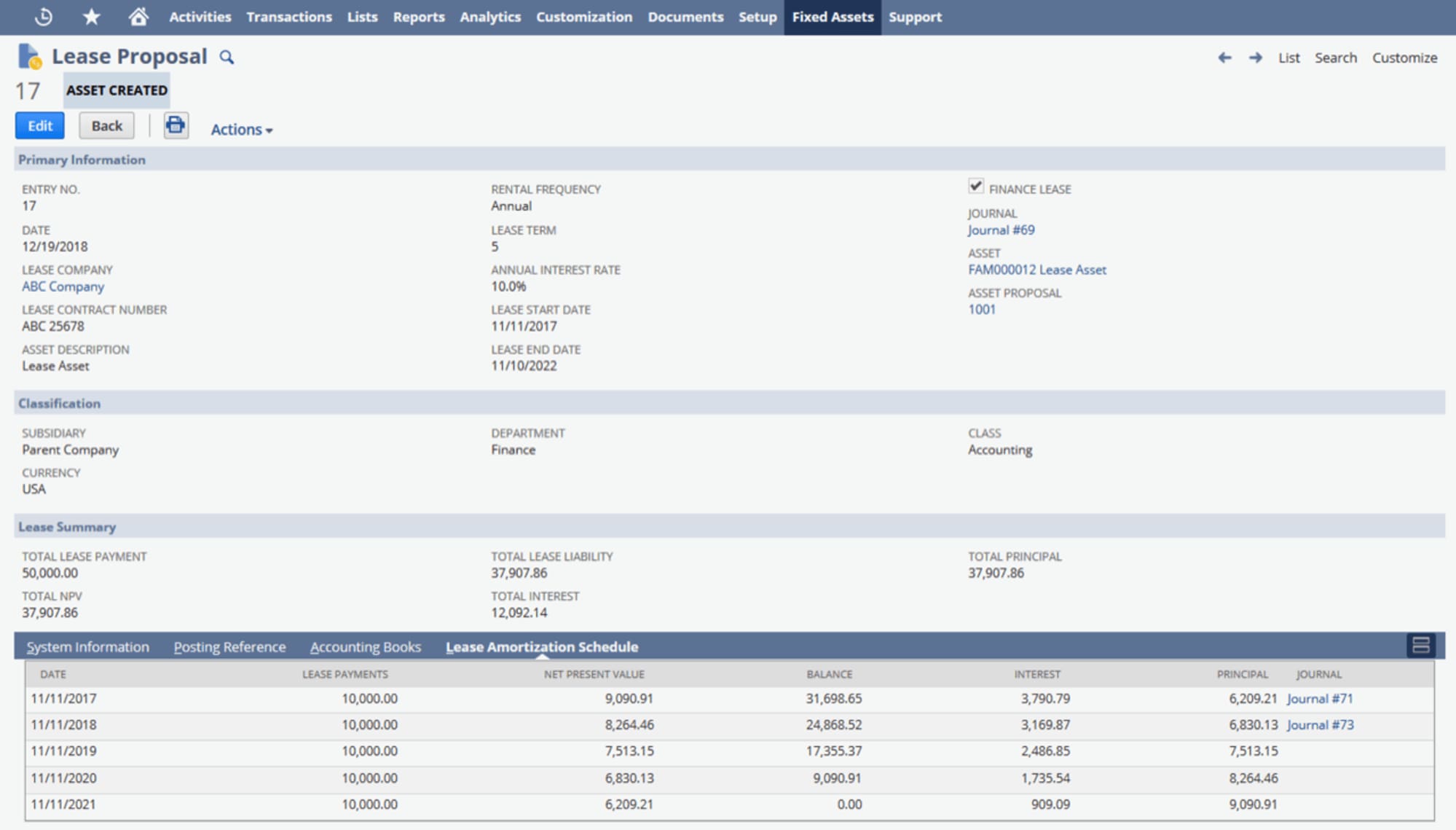

Once companies have determined how leases should be accounted for, NetSuite’s Fixed Asset and Lease Accounting Management module can help automate the entire lease accounting process. NetSuite Fixed Assets Management simplifies lease payment, amortization and reporting, helping companies comply with the latest tax rules and accounting standards. With NetSuite Fixed Assets Management, you can easily create, update and track finance and operational leases. NetSuite Fixed Assets Management separates lease and interest expenses and updates lease values automatically, ensuring compliance and streamlining the monthly close process.

#1 Cloud

Accounting

Software

- Standardize lease accounting processes across your business.

- Ensure compliance with ASC 842, IFRS 16 and GASB 87 standards.

- Import existing amortization schedules or create custom schedules as new leases are added. Automatically post journal entries with separate lease and interest expense.

- Improve financial statement accuracy and transparency.

- Automatically create reports for lease payments including net present value, interest, and principal.

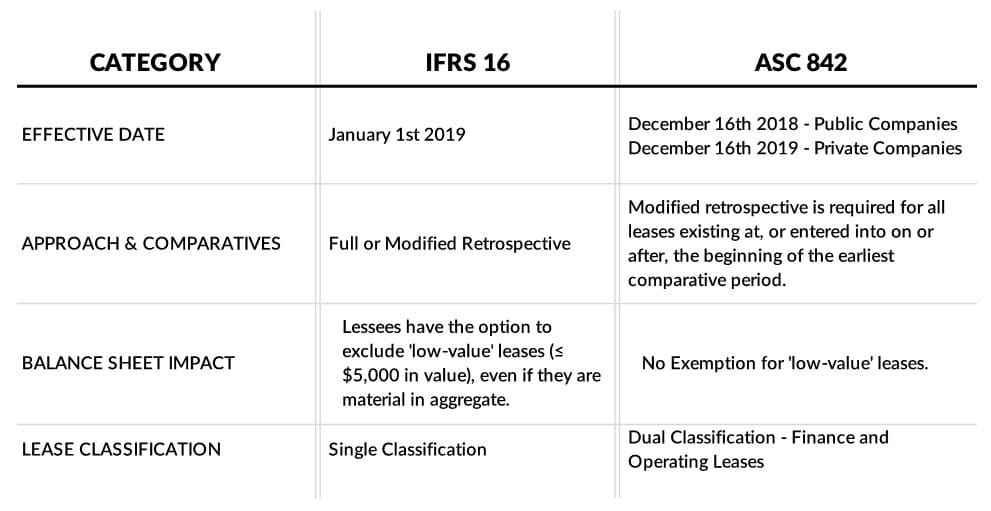

Effective January 1, 2019 for public companies and January 1, 2020 for privately held companies, the IASB’s and the FASB’s new lease standards will require that almost all leases be reported on lessees’ balance sheets as assets and liabilities. At a high level some of the key aspects of IFRS 16 and ASC 842 include but are not limited to: